25.8 Case study—applying ASC 280 (after ASU 2023-07)

Publication date: 31 Mar 2024

us Financial statement presentation guide

Example FSP 25-15 is a case study in how to apply the provisions of ASC 280. It also provides example disclosures based on the outcome of the case study. Example FSP 25-15 applies ASC 280 as updated for ASU 2023-07.

EXAMPLE FSP 25-15 Illustrative application of ASC 280 and related disclosures

The following example provides general background information relating to FSP Corp, a fictitious consumer products company. The general background is followed by an analysis regarding the determination of FSP Corp’s CODM, its operating segments, the operating segments that qualify for aggregation, and which operating segments or aggregated operating segments are reportable segments. An example footnote is also provided.

General background

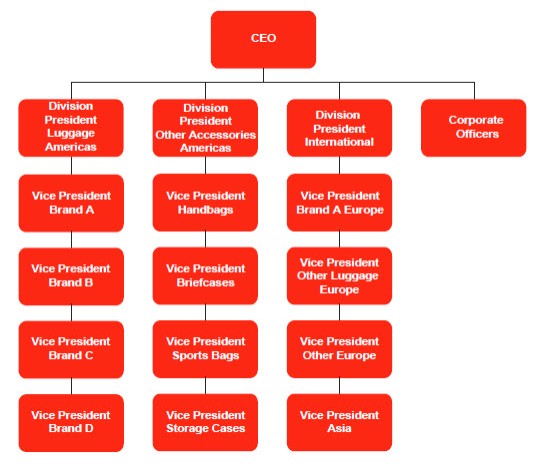

FSP Corp’s operations include manufacturing, marketing, and distribution of luggage and related accessories. The products consist of four types of branded luggage, as well as handbags, briefcases, sports bags, and storage cases (i.e., other accessories). FSP Corp is a global organization with sales in Europe, Asia, and the Americas. FSP Corp is organized as 12 marketing units, each with its own Vice President who is accountable for unit sales and performance. These marketing units are grouped into three divisions, and the Vice Presidents of the 12 marketing units report to their respective Division President. Approximately 50% of sales are from the four marketing units that compose the “Luggage Americas Division.” Approximately 30% of sales come from the four marketing units that comprise the “International Division.” The remaining 20% of sales are from the four marketing units that compose the “Other Accessories Americas Division.”

FSP Corp produces its luggage products through a network of six owned manufacturing facilities. The other accessories are produced by various independent suppliers. Other Accessories Americas Division is primarily a domestic operation, although the accessories are also sold internationally through the International Division’s marketing units. FSP Corp’s product lines are sold primarily to retailers who, in turn, sell the items to individual customers. FSP Corp also owns eight handbag retail locations in the US that sell handbag products directly to customers (handbags are also sold through third-party retailers). The results of these locations are included in the handbag marketing unit.

FSP Corp does not have any investments accounted for under the equity method and has a December 31 year-end.

The following is an organization chart for FSP Corp:

The CEO allocates resources and assesses the performance of FSP Corp primarily based on the results of each marketing unit. The CEO regularly receives information from the three Division Presidents, as well as the Corporate Officers (Chief Financial Officer, General Counsel, and Vice President of Human Resources) who report directly to the CEO.

Information reported to the CODM

Each marketing unit prepares a monthly “Operating Report,” which is sent to the applicable Division President. It reflects the marketing unit’s current-month and year-to-date sales; gross margin; operating income; and working capital. Gross margin and operating income are the most important measurements used by the marketing unit Vice Presidents, Divisional Presidents, and CEO to assess performance of the marketing units, divisions, and FSP Corp as a whole. Most incentive compensation is based on gross margin and operating income at the marketing unit level.

The monthly Operating Reports are regularly reviewed by the Division Presidents. Divisional results are prepared for each division and sent to the Division Presidents and CEO. The Operating Reports are also made available to the CEO, who may not review these reports in as much detail as the Division Presidents but finds it useful to have the disaggregated information available to analyze specific performance questions.

Additionally, the CEO is apprised of each marketing unit’s performance by:

A monthly all-day meeting with the Division Presidents and marketing unit Vice Presidents that is devoted to a discussion of recent operating results. The marketing unit Operating Reports and the consolidated division level reports are typically used as information sources during these meetings.

Frequent phone calls with the Division Presidents

Quarterly strategy meetings with marketing unit Vice Presidents, at which forecasts, business issues, opportunities, and competitors are discussed.

Each quarter, the board of directors is provided with a report that summarizes sales, operating income, gross margin, and working capital for each of the Divisions.

The following tables represent information reported in the Operating Reports.

LUGGAGE AMERICAS DIVISION Information reported as of and for the year ended December 31, 20X2 ($ in thousands)

Brand A

Brand B

Brand C

Brand D

Division total

Sales

$420

$220

$180

$100

$920

Gross margin

$126

$69

$57

$32

$284

Percentage of sales

30%

31%

32%

32%

Operating income

$80

$40

$32

$18

$170

Working capital

$200

$200

$150

$60

$610

OTHER ACCESSORIES AMERICAS DIVISION Information reported as of and for the year ended December 31, 20X2 ($ in thousands)

The CODM of FSP Corp is the CEO. Although the Division Presidents and Corporate Officers assist in the decision-making process, the CEO has historically made and is expected to continue to make the overall decisions about FSP Corp’s resource allocation. The CEO also assesses the performance of FSP Corp’s segments.

Determination and identification of operating segments

FSP Corp’s operating segments are its 12 marketing units. Based on the preceding tables that reflect FSP Corp’s internal reporting, each marketing unit recognizes revenue, incurs expenses, and has discrete financial information readily available. In addition, the monthly Operating Reports are regularly provided to and regularly reviewed by the CODM, and the CODM regularly meets with both the division presidents and the marketing unit vice presidents to discuss operating results, forecasts, business issues, etc. The CEO uses the information related to all 12 marketing units as the basis for assessing the marketing units’ performance and deciding what resources are to be allocated to them.

Determination of reportable segments

Assessing which operating segments meet all of the aggregation criteria

Since FSP Corp aligns its business by division, management first considers whether the marketing units within each division met all of the required aggregation criteria. Management prepares a long-term economic analysis for each marketing unit using gross margin, operating income, sales growth, and operating cash flows for the last three years plus forecasted results for the next three years. The impacts of foreign currency are also considered for the international operating segments.

Based on the analysis of past, current, and future expected results considering the guidance outlined in FSP 25.5.1, management concludes the operating segments representing the marketing units (Brands A, B, C, and D) of the Luggage Americas Division are quantitatively similar. Management assesses the similarity of the qualitative characteristics as follows:

The nature of the products and services All of these operating segments market luggage and, in many cases, the same types of soft shell luggage (the points of difference tend to be the price of the products, style, and external material).

The nature of the production processes The nature of the production processes is similar across all four operating segments. The production of the different brands uses common machinery and equipment in FSP Corp’s owned US facilities. In many cases, raw materials are sourced from the same suppliers and used across brands, and some piece parts are produced centrally for different operating segments in the same manufacturing facility. There are no significant technology differences in the production processes across brands.

The type or class of customer for their products and services Each brand shares similar classes of customers, which are primarily US retail department stores. US retail department stores usually carry many of FSP Corp’s brands.

The methods used to distribute their products or provide their services Each brand shares similar distribution methods, which primarily involve shipments to retail department stores by common carriers directly from FSP Corp’s manufacturing facilities.

The nature of the regulatory environment There are no specific differences in the regulatory environment for any of the four operating segments.

Management determines the operating segments meet all of the qualitative aggregation criteria. FSP Corp will aggregate the four operating segments in the Luggage Americas Division to produce a reportable segment called “Luggage Americas.”

Based on the analysis of past, current, and future expected results, considering the guidance outlined in FSP 25.5.1, management concludes the Brand A Europe and the Other Luggage Europe marketing units of the International Division are quantitatively similar. Management assesses the similarity of the qualitative characteristics as follows.

The nature of the products and services These operating segments market luggage and, in many cases, the same types of soft shell luggage (the points of difference tend to be the price of the products, style, and external material).

The nature of the production processes The nature of the production processes is similar for both segments. The luggage is manufactured in the same US plants as those described in the “Luggage Americas” reportable segment.

The type or class of customer for their products and services Each brand shares similar classes of customers, which are primarily European retail department stores.

The methods used to distribute their products or provide their services Each brand shares similar distribution methods, which primarily involve shipments to retail department stores by common carriers directly from FSP Corp’s manufacturing facilities.

The nature of the regulatory environment Although the marketing units operate in different countries, there are no significant differences in the regulatory environment.

Management determines these operating segments meet all of the qualitative aggregation criteria. FSP Corp will aggregate the Brand A Europe and the Other Luggage Europe operating segments to produce a reportable segment called “Luggage Europe.”

Although some of the other marketing units share similar economic characteristics with each other, none of the other marketing units meet all of the aggregation criteria listed in ASC 280-10-50-11. Therefore, no other operating segments are aggregated with each other.

Quantitative thresholds

FSP Corp next performs the quantitative assessments necessary to determine which of its operating segments or aggregated operating segments are required to be presented separately as reportable segments in its segment disclosures. The quantitative threshold tests should be based on the combined total of FSP Corp’s operating segments. In this example, the total is not adjusted for intersegment items that are otherwise eliminated in consolidation, since the operating segments’ results are reported to the CODM inclusive of such items (i.e., segment performance measures used to assess marketing unit performance include intercompany transactions).

Only the Luggage Americas and Luggage Europe reportable segments meet the 10% revenue test that requires separate presentation in FSP Corp’s segment disclosures.

As previously mentioned, FSP Corp uses both gross margin and operating income as its measures of segment profit or loss. However, for the 10% test, FSP Corp chose operating income as this metric applies to all segments and most closely aligns with the overall profit measure reported in the consolidated financial statements.

The Luggage Americas and the Luggage Europe reportable segments are the only segments that meet the 10% segment profit test requiring separate presentation in FSP Corp’s segment disclosures. In this example, all of the segments had a profit, making the calculations easier. As noted in FSP 25.6.1, if some segments report a profit and others report a loss, the calculations must be done separately for all those with a profit and all those with a loss.

C. 10% test – assets

Because a measure of operating segment assets is not reported to FSP Corp’s CODM, the 10% asset test is not applicable.

Immaterial operating segments which meet the majority of the aggregation criteria

Following aggregation of operating segments that meet all of the aggregation criteria in ASC 280-10-50-11 and the application of the 10% tests, only the Luggage Americas and the Luggage Europe segments meet any of the 10% tests requiring separate presentation as a reportable segment. FSP Corp then determines which remaining immaterial operating segments share similar long-term economic characteristics and meet the majority of the qualitative criteria in ASC 280-10-50-11.

Based on the analysis of past, current, and future expected results considering the guidance outlined in FSP 25.5.1, management concludes the Handbags, Briefcases, and Sports Bags marketing units have similar long-term economic characteristics and assesses the similarly of the qualitative characteristics as follows:

The nature of the products and services The Handbags, Briefcases, and Sports Bags operating segments all represent a similar type of product (personal accessories) and the points of difference tend to be the type and style of accessory.

The nature of the production processes The nature of the production processes across the operating segments is dissimilar. Handbags are sourced from several independent suppliers. The majority of the Handbags are produced in factories; however, several lines of handbags are entirely handmade. The production process for Sports Bags is primarily through an external supplier factory. The raw materials for Sports Bags primarily consist of synthetic fabrics and zippers. Briefcases are entirely handmade by a number of different independent family businesses. The raw materials for handbags primarily consist of leather, silver, and brass, all of which have had significant price fluctuations in recent years.

The type or class of customer for their products and services Each of the operating segments shares similar classes of customers, which are primarily retail department stores. The Handbags segment, however, does operate some retail locations which sell products directly to the end customers.

The methods used to distribute their products or provide their services Each brand shares similar distribution methods, which primarily involve shipments to retail department stores by common carriers.

The nature of the regulatory environment There are no significant differences in the regulatory environment for any of these operating segments.

Management determines the operating segments meet a majority of the aggregation criteria. Based on this analysis, FSP Corp will aggregate the Handbags, Briefcases, and Sport Bags segments to produce a reportable segment “Other Accessories.”

D. The 75% revenue test

Because the Luggage Americas reportable segment represents 48% of consolidated sales, the Luggage Europe reportable segment represents 26% of consolidated sales, and the Other Accessories reportable segment represents an additional 14% of external sales, total revenues of all identified reportable segments exceeds the 75% threshold. No further reportable segments are required to be disclosed. However, if the 75% threshold was not reached, FSP Corp would need to identify which of the operating segments, which otherwise would have been included in the “All Other” category, to present as a separate reportable segment until the 75% threshold was achieved.

All Other

Management analyzes the remaining operating segments (Storage Cases, Other Europe, and Asia) and concludes that none of these segments warrants separate presentation as a reportable segment as they would not provide additional useful information to the readers of the financial statements. Therefore, the remaining segments are aggregated into an “All Other” category.

Accordingly, FSP Corp has three reportable segments (Luggage Americas, Luggage Europe, and Other Accessories) and an additional All Other category, which together account for 100% of FSP Corp’s total consolidated revenues.

Measurement

FSP Corp’s measures of segment profitability that are used by management are gross margin and operating income. Management has determined that, in accordance with ASC 280-10-50-28A, it would like to report both measures of segment profit or loss. Thus, gross margin and operating income will be reported as the measures of segment profit in the segment disclosure. In accordance with ASC 280-10-50-30, it must reconcile aggregate gross margin and operating income for the reportable segments to consolidated income before income taxes.

Had management elected to only report one measure of segment profit or loss, it would have needed to evaluate which one it believed is determined in accordance with the measurement principles most consistent with those used in measuring the corresponding amounts in a public entity’s consolidated financial statements. In FSP Corp’s situation, this would be operating income as it is closest to consolidated income before income taxes.

Information about profit or loss and assets

Gross margin and operating income are the measures of segment profitability regularly reviewed by the CODM. No segment-level disclosure is required of interest expense, unusual charges, and income tax expense/benefit, since these amounts are not included in gross margin or operating income and they are not separately provided regularly to the CODM. Further, FSP Corp does not have any investments accounted for under the equity method.

Since asset information by operating or reportable segment is not reported to the CODM, the individual asset disclosures described in ASC 280-10-50-22 are not applicable to FSP Corp.

Information about significant segment expenses

FSP Corp determined that its significant segment expense categories are Cost of sales, Depreciation and amortization, and Marketing expense, as these reflect the segment-level expense information that is regularly provided to the CODM and included in the reported amounts of segment gross margin and segment operating income. FSP Corp considered relevant qualitative and quantitative factors when determining whether these segment expense categories and amounts were significant.

Entity-wide disclosures

A. Information about products and services

The CODM has access to and regularly reviews internal financial reporting by marketing unit, which are primarily organized by product. Furthermore, operating segments are aggregated into reportable segments based on similar products, and FSP Corp does not generate any service revenues. Therefore, entity-wide disclosures of information about products and services are not required.

B. Information about geographic areas

Other than the US, Germany, and Italy, no other country’s revenues from external customers are significant enough to require separate disclosure. FSP Corp will disclose revenues for these countries and remaining revenues from external customers as a single line for its other foreign operations. For this disclosure, FSP Corp determines that foreign sales will be reported by the country in which the legal subsidiary is domiciled.

As FSP Corp has no assets in an individual foreign country that are significant enough to require separate disclosure, FSP Corp will disclose long-lived assets from its United States and foreign operations.

C. Information about major customers

FSP Corp has no single customer representing greater than 10% of its consolidated revenues, and therefore this disclosure is not required.

Sample footnote

Segment information

FSP Corp is organized primarily on the basis of products and operates 3 divisions which comprise 12 separate marketing units. These 12 marketing units are our operating segments, and each of these segments is led by a Vice President. Resources are allocated and performance is assessed by our CEO, whom we have determined to be our Chief Operating Decision Maker (CODM).

Certain of our operating segments have been aggregated as they contain similar products managed within the same division, are economically similar, and share similar types of customers, production, and distribution. Four of our marketing units have been aggregated to form the “Luggage Americas” reportable segment, and two of our marketing units have been aggregated to form the “Luggage Europe” reportable segment. Three of our otherwise non-reportable marketing units have been aggregated to form the “Other Accessories” reportable segment, and the remaining three marketing units have been combined and included in an “All Other” category. The following is a brief description of our reportable segments and a description of business activities conducted by All Other.

Luggage Americas — Segment operations consist of product design, manufacturing, marketing, and sales of soft shell luggage in the US

Luggage Europe — Segment operations consist of manufacturing, marketing, and sales of soft shell luggage in Europe.

Other Accessories — Segment operations consist of product design, marketing, and sales of handbags, briefcases, and sports bags, primarily in the US

All Other — Operations consist of marketing and sales of luggage and accessories in certain international markets and the design, marketing, and sales of storage cases.

The accounting policies of the segments are the same as those described in the “Summary of Significant Accounting Policies” for FSP Corp. FSP Corp evaluates the performance of its segments and allocates resources to them based on gross margin and operating income. Segment gross margin and segment operating income includes intersegment revenues, as well as a charge allocating all corporate headquarters costs.

For all of the segments, the CODM uses segment gross margin and segment operating income in the annual budgeting and forecasting process.

The CODM considers budget-to-actual variances on a monthly basis for both profit measures when making decisions about allocating capital and personnel to the segments.

The CODM also uses segment gross margin for evaluating product pricing and segment operating income to assess the performance for each segment by comparing the results and return on assets of each segment with one another.

The CODM uses segment gross margin and segment operating income in determining the compensation of certain employees.

The table below presents information about reported segments for the years ending December 31:

A reconciliation of total segment sales to total consolidated sales and of total segment gross margin and segment operating income to total consolidated income before income taxes, for the years ended December 31, 20X2 and 20X1, is as follows:

20X2

($ in thousands)

Luggage Americas

Luggage Europe

Other accessories

All other

Total

Sales from external customers

$860

$460

$255

$225

$1,800

Intersegment sales

60

-

-

-

60

Total segment sales

920

460

255

225

$1,860

Reconciliation of sales

Elimination of intersegment sales

(60)

Total consolidated sales

$1,800

Less:

Cost of sales

636

316

154

179

1,285

Segment gross margin

284

144

101

46

$575

Less:

Depreciation and amortization

20

14

12

4

50

Marketing expense

62

31

21

2

116

Other segment items (a)

32

6

3

4

45

Segment operating income

170

93

65

36

$364

Reconciliation to income before income taxes

Other income (expense), net

(50)

Intersegment profit

(15)

Interest income (expense), net

(80)

Income before income taxes

$219

20X1

($ in thousands)

Luggage Americas

Luggage Europe

Other accessories

All other

Total

Sales from external customers

$845

$425

$230

$202

$1,702

Intersegment sales

40

-

-

-

40

Total segment sales

885

425

230

202

$1,742

Reconciliation of sales

Elimination of intersegment sales

(40)

Total consolidated sales

$1,702

Less:

Cost of sales

612

292

139

161

1,204

Segment gross margin

273

133

91

41

$538

Less:

Depreciation and amortization

18

13

11

3

45

Marketing expense

61

28

19

2

110

Other segment items (a)

30

6

3

4

43

Segment operating income

164

86

58

32

$340

Reconciliation to income before income taxes

Other income (expense), net

(45)

Intersegment profit

(11)

Interest income (expense), net

(70)

Income before income taxes

$214

(a) Other segment items for each reportable segment includes:

Luggage Americas – selling and administrative expenses, research and development expenses, professional services expense and certain overhead expenses

Luggage Europe – selling and administrative expenses, professional services expense, and certain overhead expenses

Other Accessories – travel expenses, research and development expenses, and certain overhead expenses

All Other – maintenance expense, professional services expense and certain overhead expenses

The following tables present sales and long-lived asset information by geographic area for the years ended December 31, 20X2 and 20X1. Asset information by segment is not reported internally or otherwise regularly reviewed by the CODM.

Sales

($ in thousands)

20X2

20X1

United States

$1,260

$1,191

Germany

177

170

Italy

180

175

All Other Foreign

183

166

$1,800

$1,702

Long-lived Assets

($ in thousands)

20X2

20X1

United States

$1,090

$1,035

Foreign

260

245

$1,350

$1,280

Foreign revenue is based on the country in which the legal subsidiary is domiciled.

1 Note: For this illustrative example, only two years of segment results are presented. SEC registrants typically require the presentation of three years of segment results.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.