A distinct and separable operation’s functional currency is the currency of the primary economic environment in which it operates.

ASC 830-10-45-2 provides the definition of functional currency. This guidance refers to the functional currency of an entity but, as discussed in

FX 2, the better term is distinct and separable operation, since that is the primary attribute of a reporting entity’s foreign entities.

ASC 830-10-45-2

The assets, liabilities, and operations of a foreign entity shall be measured using the functional currency of that entity. An entity’s functional currency is the currency of the primary economic environment in which the entity operates; normally, that is the currency of the environment in which an entity primarily generates and expends cash.

Often, the functional currency will be the currency of the country in which the distinct and separable operation is physically located. However, some distinct and separable operations operate in an economic environment different than that of their physical location. For example, if a US-based multinational oil and gas company that uses the US dollar as its reporting currency maintains a distinct and separable operating subsidiary in Northern Africa that sells all of its oil production in transactions denominated in the US dollar, the US dollar would be the functional currency of that operation. While the Northern African oil subsidiary is located outside the United States, it would not be considered a foreign entity under

ASC 830, as its functional currency is the same as the reporting currency of the reporting entity. If the same US-based multinational used the Canadian dollar as its reporting currency, the Northern Africa subsidiary and the oil and gas operations located in the US would be considered foreign entities for purposes of applying

ASC 830 because their functional currencies would be different than the reporting currency of the reporting entity.

When a distinct and separable operation transacts in multiple currencies, it should assess all relevant facts to determine its functional currency.

For purposes of determining functional currency,

ASC 830-10-45-4 divides foreign operations into two broad classes. While this guidance uses the term foreign operations, it is equally applicable to any distinct and separable operation. As discussed in

FX 1.2,

ASC 830 was written assuming a two-tiered organization (i.e., parent and subsidiary). In most modern multinational organizations, there are often multiple layers (i.e., holding company, first-tier operating entity, second-tier operating entity). We believe the guidance in

ASC 830-10-45-4 should be applied by analyzing the relationship between a distinct and separable operation and its immediate parent.

ASC 830-10-45-4

Multinational reporting entities may consist of entities operating in a number of economic environments and dealing in a number of foreign currencies. All foreign operations are not alike. To fulfill the objectives in paragraph 830-10-10-2, it is necessary to recognize at least two broad classes of foreign operations:

- In the first class are foreign operations that are relatively self-contained and integrated within a particular country or economic environment. The day-to-day operations are not dependent on the economic environment of the parent’s functional currency; the foreign operation primarily generates and expends foreign currency. The foreign currency net cash flows that it generates may be reinvested or converted and distributed to the parent. For this class, the foreign currency is the functional currency.

- In the second class are foreign operations that are primarily a direct and integral component or extension of the parent entity’s operations. Significant assets may be acquired from the parent entity or otherwise by expending dollars and, similarly, the sale of assets may generate dollars that are available to the parent. Financing is primarily by the parent or otherwise from dollar sources. In other words, the day-to-day operations are dependent on the economic environment of the parent’s currency, and the changes in the foreign entity’s individual assets and liabilities impact directly on the cash flows of the parent entity in the parent’s currency. For this class, the dollar is the functional currency.

Sometimes an operation will clearly align with one of these two classes; however, more often an operation will have characteristics of both classes. When an operation is clearly an extension of its parent, the operation’s functional currency is that of its parent. There may also be situations in which an operation is not considered distinct and separable and is also not clearly an extension of its immediate (legal) parent. In these situations, the operation may be considered an extension of another separate and distinct operation. For example, a sales entity located in Germany with an immediate US (legal) parent that services a distinct and separable operation in the United Kingdom (UK) may be considered an extension of the UK entity for purposes of determining its functional currency.

When an operation is not clearly an extension of its parent, management will need to consider the factors discussed in

ASC 830-10-55-5 to determine the operation’s functional currency. This guidance provides a list of economic indicators that should be considered individually and collectively when determining a distinct and separable operation’s functional currency.

ASC 830 does not weight or rank these indicators; however, in our experience, the sales price, sales market, and expense indicators are the most important factors in determining the primary economic environment in which a distinct and separable operation operates. Cash flows can also be an important indicator provided the cash flows are not merely an invoicing or settlement currency, but reflect the underlying transactions’ economics. Management should evaluate its specific facts and circumstances to determine which indicators are the most relevant to the distinct and separable operation and the economic environment in which it operates.

ASC 830-10-55-5

The following salient economic factors, and possibly others, should be considered both individually and collectively when determining the functional currency:

- Cash flow indicators, for example:

- Foreign currency. Cash flows related to the foreign entity’s individual assets and liabilities are primarily in the foreign currency and do not directly affect the parent entity’s cash flows.

- Parent’s currency. Cash flows related to the foreign entity’s individual assets and liabilities directly affect the parent’s cash flows currently and are readily available for remittance to the parent entity.

- Sales price indicators, for example:

- Foreign currency. Sales prices for the foreign entity’s products are not primarily responsive on a short-term basis to changes in exchange rates but are determined more by local competition or local government regulation.

- Parent’s currency. Sales prices for the foreign entity’s products are primarily responsive on a short-term basis to changes in exchange rates; for example, sales prices are determined more by worldwide competition or by international prices.

- Sales market indicators, for example:

- Foreign currency. There is an active local sales market for the foreign entity’s products, although there also might be significant amounts of exports.

- Parent’s currency. The sales market is mostly in the parent’s country or sales contracts are denominated in the parent’s currency.

- Expense indicators, for example:

- Foreign currency. Labor, materials, and other costs for the foreign entity’s products or services are primarily local costs, even though there also might be imports from other countries.

- Parent’s currency. Labor, materials, and other costs for the foreign entity’s products or services continually are primarily costs for components obtained from the country in which the parent entity is located.

- Financing indicators, for example:

- Foreign currency. Financing is primarily denominated in foreign currency, and funds generated by the foreign entity’s operations are sufficient to service existing and normally expected debt obligations.

- Parent’s Currency—Financing is primarily from the parent or other dollar-denominated obligations, or funds generated by the foreign entity’s operations are not sufficient to service existing and normally expected debt obligations without the infusion of additional funds from the parent entity. Infusion of additional funds from the parent entity for expansion is not a factor, provided funds generated by the foreign entity’s expanded operations are expected to be sufficient to service that additional financing.

- Intra-entity transactions and arrangements indicators, for example:

- Foreign currency. There is a low volume of intra-entity transactions and there is not an extensive interrelationship between the operations of the foreign entity and the parent entity. However, the foreign entity’s operations may rely on the parent’s or affiliates’ competitive advantages, such as patents and trademarks.

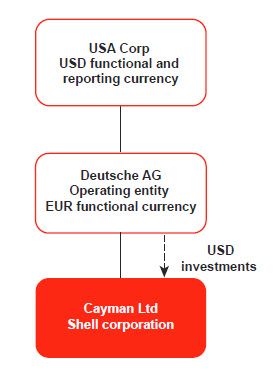

- Parent’s currency. There is a high volume of intra-entity transactions and there is an extensive interrelationship between the operations of the foreign entity and the parent entity. Additionally, the parent’s currency generally would be the functional currency if the foreign entity is a device or shell corporation for holding investments, obligations, intangible assets, and so forth, that could readily be carried on the parent’s or an affiliate’s books.

Given that an operation’s functional currency should not change frequently, the indicators in

ASC 830-10-55-5 should be considered from the perspective of a distinct and separable operation’s long-term operations.

Question FX 3-1

How should the functional currency of a start-up operation be determined?

PwC response

The functional currency of a start-up operation should be a function of the economic environment the entity expects to operate in over the long-term. The currency of that long-term economic environment is the functional currency of a start-up operation, not the currency that is used to fund initial operations or the currency of its initial cash flows.

Example FX 3-1, Example FX 3-2, and Example FX 3-3 illustrate how to determine the functional currency of a foreign operation, sales office, and foreign manufacturing facility, respectively.

EXAMPLE FX 3-1

Determining the functional currency of a foreign operation

USA Corp is a US registrant that uses the US dollar (USD) as its reporting currency.

Britannia PLC is a consolidated subsidiary of USA Corp located in the United Kingdom. Consider the following facts regarding Britannia PLC:

- Britannia PLC is a distinct and separable operation of USA Corp.

- The local currency of Britannia PLC is the British pound sterling (GBP).

- Britannia PLC manages USA Corp’s operations within the European market, including strategy, manufacturing, sales, logistics, billing and collections.

- Customers of Britannia PLC are located across Europe, with the majority of its customers located in the United Kingdom, Germany, France, and Italy.

- Sales are denominated in GBP and euros (EUR); sales prices are primarily driven by local competition.

- Britannia PLC was originally funded by USA Corp with a capital contribution and a USD 100 million intercompany loan. It also has a third-party line of credit of GBP 20 million, which can be drawn in either GBP or EUR.

- Cost of goods sold comprises 75% of Britannia PLC’s expenses. It purchases 50% of its raw materials from a USA Corp subsidiary in the United States in USD (at market prices) and 50% of its raw materials from third parties in EUR. Selling, general and administrative expenses comprise 25% of the subsidiary’s expenses and are denominated 50% in GBP and 50% in EUR.

Britannia PLC’s income statement is shown below. During the period presented, the average exchange rates are EUR 1 = USD 1.4, and GBP 1 = USD 1.7.

Income/ expense |

Amount in currency in which income or expense is denominated |

Exchange rate |

Amount in USD |

|

|

|

|

|

|

Selling, general and administrative expenses

|

|

|

|

|

|

|

|

|

|

View table

What is the functional currency of Britannia PLC?

Analysis

Since Britannia PLC transacts in multiple currencies, management will need to assess the factors outlined in

ASC 830-10-55-5 to determine the appropriate functional currency.

Indicator |

Currency |

Analysis |

|

|

Operating cash flows are predominantly denominated in EUR (75% of sales and 50% of expenses)

|

|

|

Local competition in the European sales market dictates the sales price; sales prices are negotiated in both EUR and GBP

|

|

|

The predominant sales market is EUR denominated

|

|

|

Raw material purchases are denominated in USD and EUR; selling, general and administrative expenses are denominated in EUR and GBP

|

|

|

A large intercompany loan is denominated in USD

|

Management considers the sales market, sales price, and related cash flows of the Britannia PLC to be the most significant economic indicators. They believe operating cash flows are a significant indicator in this case. Since operating cash flows are predominantly EUR denominated, the cash flow indicator strongly suggests the EUR is Britannia PLC’s functional currency. The sales market and sales price indicators also signal EUR as the functional currency. Expenses are split between USD and EUR.

The financing indicator points to USD. Management does not place significant weight on the financing indicator because the denomination of an intercompany loan can be easily changed. If significant weight were placed on the financing indicator, Britannia PLC’s functional currency could be easily influenced by USA Corp.

Based on this analysis, Britannia PLC’s functional currency is the EUR.

EXAMPLE FX 3-2

Determining the functional currency of a sales office

USA Corp is a US registrant that uses the US dollar as its reporting currency. Deutsche AG is a wholly-owned subsidiary of USA Corp located in Germany, which functions as the European sales office of USA Corp. Consider the following facts regarding Deutsche AG:

- The local currency is EUR.

- Deutsche AG manages USA Corp sales within the European market, including negotiating sales contracts with its European customers, coordinating delivery of products, as well as performing billing and collections. Products are produced in the US and shipped directly to customers in Europe.

- Customers of the European sales office are located across Europe, with the majority of the customers located in Germany, France, and Italy.

- Sales are in EUR; the sales price is primarily driven by local competition.

- USA Corp finances Deutsche AG by reimbursing its expenses (which are mostly payroll and administration related) plus an additional 3% each month; the incremental 3% is used to pay the local taxing authority.

- Deutsche AG’s assets consist mainly of office equipment, and the hardware and software necessary to execute the sales duties of the organization.

What is the functional currency of Deutsche AG?

Analysis

Deutsche AG is a direct and integral extension of USA Corp’s operations (i.e., it is not distinct and separable). Deutsche AG performs a European sales function that could just as easily be performed by USA Corp directly, and Deutsche AG cannot operate without financing from USA Corp. As a result, management concludes that the functional currency of Deutsche AG is USD, the functional currency of its immediate parent, USA Corp.

EXAMPLE FX 3-3

Determining the functional currency of a foreign manufacturing facility

USA Corp is a US registrant that uses the US dollar as its reporting currency. Mexico SA is a wholly-owned subsidiary of USA Corp located in Mexico, which functions as a manufacturing facility of USA Corp. Consider the following facts regarding Mexico SA:

- USA Corp manufactures parts for one of its products at a facility in the United States. USA Corp packages the parts and ships them to Mexico SA for assembly.

- Mexico SA has a manufacturing facility in Chihuahua, Mexico. This facility receives the parts from USA Corp. Employees of Mexico SA assemble the parts into the final product and test them to ensure that the quality of the product is up to USA Corp’s standards.

- Mexico SA then ships the completed product back to USA Corp for sale to customers.

- The local currency of Mexico SA is the Mexican Peso (MXN).

- USA Corp funds the expenses of Mexico SA each month, plus a small margin.

What is the functional currency of Mexico SA?

Analysis

Mexico SA is a direct and integral extension of USA Corp’s operations; Mexico SA performs assembly that could just as easily be performed by USA Corp directly, and Mexico SA cannot operate without financing from USA Corp. Furthermore, Mexico SA’s expenses have a direct impact on USA Corp’s cash flows through the cost-plus reimbursement arrangement. As a result, the functional currency of Mexico SA is USD, the functional currency of its parent, USA Corp.

Question FX 3-2

Can a distinct and separable operation have more than one functional currency?

PwC response

No. A distinct and separable operation cannot have more than one functional currency. However, a single legal entity could comprise more than one distinct and separable operation, in which each has its own functional currency. See

FX 2 for information on identifying distinct and separable operations.