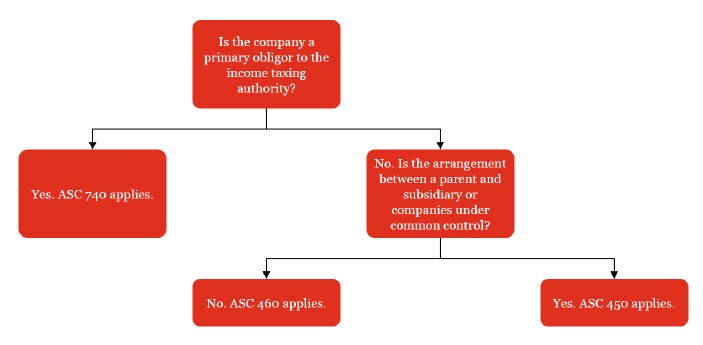

The indemnified party must also determine if they are a primary obligor to the taxing authority and, if so, recognize and measure a liability in accordance with

ASC 740. If the indemnifying and indemnified parties are both liable for the exposure, both parties should apply the guidance in

ASC 740. The indemnified party must then determine the amount to recognize for the indemnification receivable.

The relevant accounting guidance for the indemnified party may differ depending on whether the transaction is accounted for as a business combination (see

TX 10.7 for discussion of indemnification uncertainties in a business combination). Regardless of the recognition and measurement model followed for the indemnified asset, the indemnified party should not offset the indemnification receivable against the tax liability because those amounts are receivable from and payable to two different parties and so do not qualify for off-set.

The guidance in

ASC 805 is limited to business combinations and, therefore, does not apply to transactions such as spin-offs or asset acquisitions. Accordingly, the question arises whether "mirror image" accounting should be applied to transactions other than business combinations. In “mirror image” accounting, the indemnified party recognizes an indemnification asset (as it relates to the uncertain tax position) at the same time that it recognizes the indemnified item and measures the asset on the same basis as the indemnified item.

Question TX 15-3 addresses the tax accounting related to indemnification receivables.

Question TX 15-3

Company B used to be the parent of Company A. However, the two companies are no longer related. Company B has indemnified Company A for any uncertain tax position liabilities ultimately payable by Company A related to periods when Company B was Company A’s parent. Therefore, Company A has recorded an indemnification receivable equivalent to its uncertain tax position liabilities from that time period. Should deferred income taxes be recorded related to the indemnification receivable?

PwC response

No. From a US tax perspective, there are typically no consequences from indemnification payments. The amount paid to the taxing authority and the amount collected from the seller would generally offset, with no net impact on taxable earnings. As a result, in most cases the indemnification receivable recorded would not be expected to have a deferred tax effect.

Question TX 15-4 addresses intraperiod considerations related to tax consequences of an indemnification.

Question TX 15-4

Company A spins off Company B but retains a partial interest. The spinnor (Company A) may indemnify the spinnee (Company B) for a legal claim. When the legal claim is settled, any necessary indemnification payments from the spinnor to the spinnee would constitute taxable income to the spinnee. How should the tax consequences of the indemnification payment be recorded?

PwC response

In this case, the tax consequences of the indemnification payment should generally be recorded in the same manner as the indemnification payment. For example, if the indemnification payment is recorded as a capital contribution due to an ownership relationship between the two parties, the tax consequences should also be recorded in accumulated paid-in-capital.

In certain situations, in an effort to neutralize the impact of a tax exposure to a fund’s net asset value (NAV), a fund manager is willing to indemnify the fund for its tax exposure. In connection with the implementation of

ASC 740’s guidance related to uncertain tax positions, certain investment funds approached the SEC staff for guidance on how to measure an indemnification receivable. In a letter to the funds, the SEC staff noted that “an advisor’s (or other relevant party’s) contractual obligation to indemnify uncertain tax positions generally would be sufficient in demonstrating that the likelihood of recovery is probable. The process of obtaining a contractual obligation to indemnify uncertain tax positions may occur simultaneously while the fund is gathering the relevant information to assess whether a liability should be recorded to NAV. In these circumstances, recognition of an indemnification receivable, to the extent of recovery of the tax accrual, generally would be acceptable practice.” The SEC’s letter provides support for recognizing the indemnification receivable at the same amount as the recorded liability absent any collectability or contractual limitations on the indemnified amount.

A more common indemnification scenario, outside of a business combination, is when a parent spins off a subsidiary. Following the spin-off, the parent may indemnify the new entity for income tax exposures related to the spun-off entity’s prior operations. Assuming that the indemnification fully covers the exposure, we believe that it would be reasonable for the spun-off entity to record an indemnification receivable at the same amount as the tax liability. This view is consistent with the SEC’s letter to the funds.

When a parent retains a controlling interest after a transaction like an IPO or spin-off, the parent-subsidiary relationship survives the transaction. If the parent indemnifies the subsidiary, consideration should be given to whether the indemnification asset and subsequent changes should be recorded in equity.