Search within this section

Select a section below and enter your search term, or to search all click Loans and investments

Favorited Content

Step 1

|

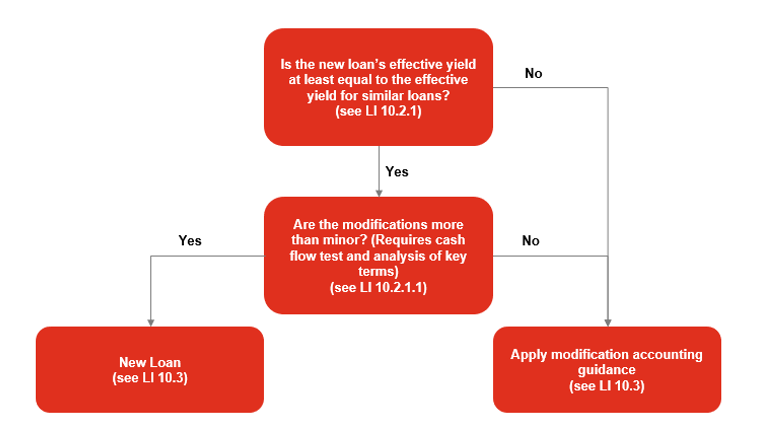

In accordance with ASC 310-20-35-11, compare the present value of the cash flows of the new debt with the present value of the remaining cash flows of the original debt utilizing the guidance in ASC 470. See FG 3 for an illustration of this assessment.

If the present value of cash flows differs by at least 10%, the modification is considered more than minor.

If the present value of cash flows differs by less than 10%, further analysis should be performed under Step 2.

ASC 470-50-40-12 provides specific guidance on performing the 10% test. Key takeaways from this guidance include:

|

|

Step 2

|

The creditor should evaluate whether the modification is more than minor based on the specific facts and circumstances surrounding the modification and other relevant considerations. The accounting literature does not provide specific guidance on what factors a reporting entity should consider.

Relevant facts may include considering the impact of the modification on the following:

|

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Loans and investments