Some conduit bond obligors (particularly in the health care sector) coordinate multiple borrowings using a master trust indenture (MTI) structure. This indenture is separate from, and serves a different purpose than, the indenture discussed in

NP 11.3.1. In these arrangements, a conduit obligor selects a bank to serve as “master trustee” for a credit group (often referred to as an “obligated group”) whose aggregated revenue, cash, and assets are used as collateral for various financings. Normally, the obligated group is comprised of specifically identified entities within the consolidated financial reporting entity. In most cases, the entities within an obligated group have joint and several liability for the payment of any debt secured by the MTI, which means that in theory, any one of the parties to the arrangement could be liable for the entire amount of the bonds.

Continuing disclosure agreements for obligated group financings will usually require the issuer to provide financial information on the assets, liabilities, revenues, and expenses of the obligated group. Typically, the consolidated external financial statements of the consolidated reporting entity are used, with balance sheet and income statement information of the obligated group provided in combining or consolidating schedules that are presented as supplemental information. For example, a supplemental schedule might include individual columns for each entity in the obligated group, an obligated group subtotal column, an aggregate column for all other entities, and the consolidated total column that corresponds to the consolidated financial statements.

When separately issued statements are required for an individual entity within the obligated group, that entity’s obligation and its joint-and-several liability must be appropriately presented and described.

ASC 405-40,

Obligations Resulting from Joint and Several Liability Arrangements, provides accounting and financial statement presentation guidance on these matters.

Based on the requirements of

ASC 405-40-30-1, an obligated group member’s individual financial statements would reflect a liability for the portion of the obligation that has been allocated to it for repayment, plus any amount that it expects to pay on behalf of its co-obligors.

ASC 405-40-30-1

Obligations resulting from joint and several liability arrangements included in the scope of this Subtopic initially shall be measured as the sum of the following:

- The amount the reporting entity agreed to pay on the basis of its arrangement among its co-obligors.

- Any additional amount the reporting entity expects to pay on behalf of its co-obligors. If some amount within a range of the additional amount the reporting entity expects to pay is a better estimate than any other amount within the range, that amount shall be the additional amount included in the measurement of the obligation. If no amount within the range is a better estimate than any other amount, then the minimum amount in the range shall be the additional amount included in the measurement of the obligation.

The amount that an individual group member expects to pay on behalf of its co-obligors is measured based on principles that are similar to those in

ASC 450-20,

Loss Contingencies. The amount recorded should be the best estimate of the expenditure required to settle the obligation. If the best estimate is a range, and if one amount in that range represents a better estimate than any other amount within the range, that amount should be accrued. If no amount in the range is a better estimate than any other, the minimum amount in the range is included (which could be zero).

Disclosure should be made regarding the joint-and-several nature and amount of the overall obligation as well as information about the risks that the obligation poses to the entity’s future cash flows.

Example NP 11-1 illustrates the application of this guidance.

EXAMPLE NP 11-1

Joint and several liability – obligated group

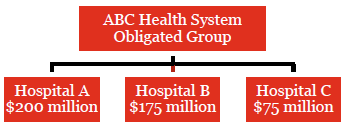

ABC Health System has an obligated group consisting of three hospitals. In 20X1, the obligated group issues $450 million of bonds, with the proceeds allocated among the hospitals as shown. The hospitals are jointly and severally liable for repayment of the bonds. Each individual hospital is expected to repay the portion of the proceeds that were allocated to it.

Hospital A prepares and issues standalone financial statements. How should Hospital A reflect the bond liability?

Analysis

Under

ASC 405-40, Hospital A’s statements should reflect a liability for the amount that has been allocated to it for repayment ($200 million), plus an additional amount reflecting the amount it expects to pay on behalf of another member (if any). If each member of the group is solvent and expected to pay its allocated share of the obligation, Hospital A’s balance sheet would reflect a $200 million liability at the outset, and the notes would disclose the $250 million contingent obligation. The disclosures should include the nature and amount of the obligation as well as information about risks such obligations pose to Hospital A’s future cash flows.

If in 20X3 it appears that Hospital C might become unable to repay some or all of its $75 million allocation, Hospital A’s estimate of the additional amount it expects to pay on behalf of others may increase above zero. Hospital A would develop a range of exposure (for example, $15-50 million). If no amount is better than any other in that range, Hospital A would increase the liability by $15 million.

For more information on accounting for joint and several obligations, see

FG 2.9.