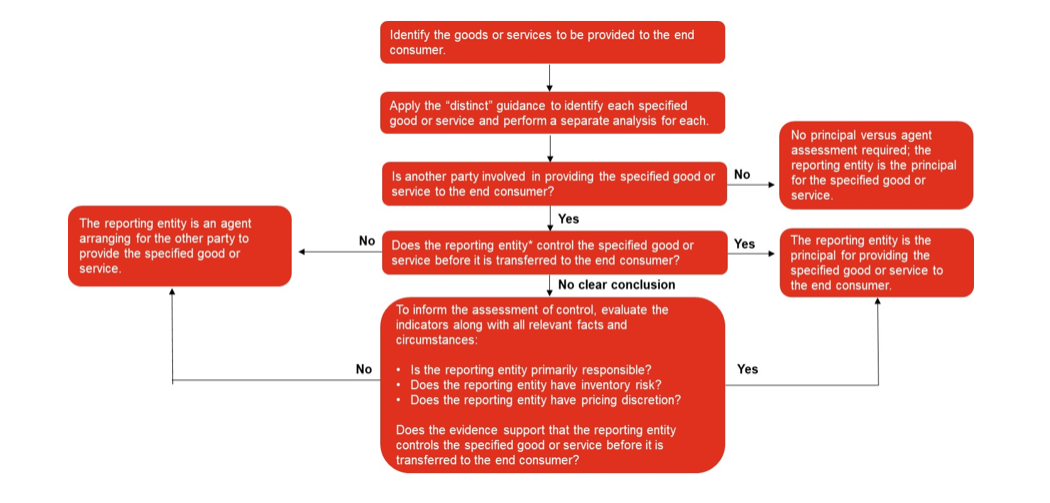

Example RR 10-1, Example RR 10-2, and Example RR 10-3 illustrate the analysis of whether a reporting entity is the principal or an agent in various arrangements. These concepts are also illustrated in Examples 45-48A of the revenue standard (

ASC 606-10-55-317 through

ASC 606-10-55-334F).

EXAMPLE RR 10-1

Principal versus agent – reporting entity is an agent

WebCo operates a website that sells books. WebCo enters into a contract with Bookstore to sell Bookstore’s books online. WebCo’s website clearly identifies Bookstore as the seller of the books and facilitates payments between Bookstore and the end consumer. The sales price is established by Bookstore, and WebCo earns a fee equal to 5% of the sales price. Bookstore ships the books directly to the end consumer, and WebCo cannot redirect ordered books to other customers. The end consumer returns the books to WebCo if they are dissatisfied; however, WebCo has the right to return books to Bookstore for a full refund if they are returned by the end consumer.

Is WebCo the principal or an agent for the sale of books to the end consumer?

Analysis

WebCo is acting as a sales agent for Bookstore and should recognize revenue equal to the fee it charges Bookstore for facilitating sales to end consumers; that is, it should recognize revenue on a net basis.

The specified good or service is a book purchased by the end consumer. WebCo does not control the book before it is transferred to the end consumer because it does obtain control of the book from Bookstore, does not direct Bookstore to perform on its behalf, and does not combine the book with other goods or services into a combined output. This conclusion is supported by the indicators of control:

- WebCo is not primarily responsible for fulfilling the promise to deliver a book.

- WebCo does not have inventory risk because it has the right to return books to Bookstore that are returned by end consumers.

- WebCo does not have discretion in establishing the selling price of the book.

WebCo should recognize revenue equal to its 5% fee when it satisfies its promise to facilitate the sale of a book (that is, when a confirmed order is placed on its website).

EXAMPLE RR 10-2

Principal versus agent – reporting entity is the principal

TravelCo negotiates with major airlines to obtain access to airline tickets at reduced rates and sells the tickets to end consumers through its website. TravelCo contracts with airlines to buy a specific number of tickets at agreed-upon rates and must pay for those tickets regardless of whether it is able to resell them. End consumers visiting TravelCo’s website search TravelCo’s available tickets. TravelCo has discretion in establishing the prices for the tickets it sells to the end consumers.

TravelCo is responsible for delivering the ticket to the end consumer. TravelCo will also assist the end consumer in resolving complaints with the service provided by the airlines. The airline is responsible for fulfilling all other obligations associated with the ticket, including the air travel and related services (that is, the flight), and remedies for service dissatisfaction.

Is TravelCo the principal or an agent for the sale of an airline ticket to an end consumer?

Analysis

TravelCo is the principal for the sale of the ticket to the end consumer and should recognize revenue for the price paid by the end consumer; that is, it should recognize revenue on a gross basis.

The specified good or service is a right to fly on the selected flight (represented by a ticket) along with the other rights provided by the airline for the holder of that ticket. TravelCo obtains control of the right to the airline’s services (which it could resell or use itself) and transfers that right (represented by the ticket) to the end consumer. This conclusion is supported by the indicators of control:

- Although the airline is responsible for providing the air travel services, TravelCo is primarily responsible for fulfilling the promise to transfer a right to future services (the ticket) to the end consumer.

- TravelCo has inventory risk as a result of purchasing the ticket from the airline in advance and will be subject to the risks and rewards of ownership, including loss if it is unable to sell the ticket.

- TravelCo has discretion in establishing the selling price of the ticket.

TravelCo should recognize revenue equal to the price paid by the end consumer for the ticket when it transfers control of the ticket to the end consumer. It will recognize the cost of the ticket (the purchase price from the airline) as cost of sales.

EXAMPLE RR 10-3

Principal versus agent – multiple specified goods or services

PayrollCo provides payroll processing services to end consumers under a service arrangement. PayrollCo also offers consulting services to an end consumer related to the end consumer’s payroll and compensation processes. PayrollCo has concluded that the payroll processing services and consulting services are distinct in the arrangement with the end consumer.

The consulting services are performed by a third party, ConsultCo. ConsultCo determines the pricing of the consulting services and coordinates directly with the end consumer to determine the timing and scope of work. PayrollCo occasionally assists the end consumer in resolving complaints about the consulting services; however, ConsultCo is responsible for meeting the end consumer’s specifications, including providing any refunds or reperforming work, as needed.

PayrollCo bills and collects the fee for the consulting services, of which 90% is remitted to ConsultCo. Any losses resulting from cost overruns in the consulting services are fully absorbed by ConsultCo. On a monthly basis, PayrollCo bills and collects a service fee from the end consumer for the payroll processing services. No discounts are provided to the end consumer for purchasing the services as a bundle.

Is PayrollCo the principal or an agent for the payroll processing services and consulting services?

Analysis

There are two distinct specified services in the arrangement: payroll processing services and consulting services. PayrollCo is the principal for the payroll processing services provided to the end consumer because no other parties are involved in providing these services. Therefore, PayrollCo will recognize revenue for the payroll processing services on a gross basis. PayrollCo is an agent arranging for ConsultCo to provide the consulting services to the end consumer; therefore, it will recognize revenue net of the amount remitted to ConsultCo.

PayrollCo does not control the consulting services because it does not obtain a right to the consulting services, does not direct ConsultCo to perform on its behalf, and does not combine the consulting services with other goods or services into a combined output. This conclusion is supported by the indicators of control:

- PayrollCo is not primarily responsible for fulfilling the promise to provide consulting services.

- PayrollCo does not have inventory risk as it does not pay for the consulting services in advance.

- PayrollCo does not have discretion in establishing the selling price of the consulting services.

PayrollCo should recognize revenue equal to the price it charges end consumers for payroll processing services as it provides the services. PayrollCo should recognize the commission it receives from ConsultCo when it satisfies its promise to arrange for the consulting services.