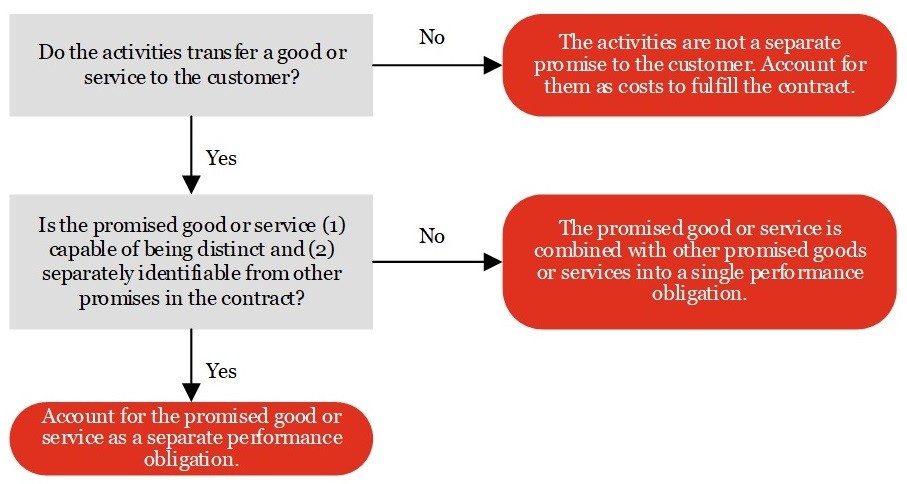

Arrangements that involve shipment of goods to a customer might include promises related to the shipping service that give rise to a performance obligation. Management should assess the explicit shipping terms to determine when control of the goods transfers to the customer and whether the shipping services are a separate performance obligation.

Shipping and handling services may be considered a separate performance obligation if control of the goods transfers to the customer before shipment, but the reporting entity has promised to ship the goods (or arrange for the goods to be shipped). In contrast, if control of a good does not transfer to the customer before shipment, shipping is not a promised service to the customer. This is because shipping is a fulfillment activity as the costs are incurred as part of transferring the goods to the customer.

Management should assess whether the reporting entity is the principal or an agent for the shipping service if it is a separate performance obligation. This will determine whether the reporting entity should record the gross amount of revenue allocated to the shipping service or the net amount, after paying the shipper. Refer to

RR 10.4 for further consideration related to the presentation of shipping and handling costs within the income statement.

The revenue standard includes an accounting policy election that permits reporting entities to account for shipping and handling activities that occur after the customer has obtained control of a good as a fulfillment cost rather than as an additional promised service. Reporting entities that make this election will recognize revenue when control of the good transfers to the customer. A portion of the transaction price would not be allocated to the shipping service; however, the costs of shipping and handling should be accrued when the related revenue is recognized. Management should apply this election consistently to similar transactions and disclose the use of the election, if material, in accordance with

ASC 235,

Notes to Financial Statements. The policy election should not be applied by analogy to other services.

Example RR 3-9 and Example RR 3-10 illustrate the potential accounting outcomes for sale of a product and a promise to ship the product.

EXAMPLE RR 3-9Identifying performance obligations — shipping and handling services

Manufacturer enters into a contract with a customer to sell five flat screen televisions. The customer requests that Manufacturer arrange for delivery of the televisions. The delivery terms state that legal title and risk of loss pass to the customer when the televisions are given to the carrier.

The customer obtains control of the televisions at the time they are shipped and can sell them to another party. Manufacturer is precluded from selling the televisions to another customer (for example, redirecting the shipment) once the televisions are picked up by the carrier at Manufacturer’s shipping dock. Manufacturer does not elect to treat shipping and handling activities as a fulfillment cost.

How many performance obligations are in the arrangement?

Analysis

There are two performance obligations: (1) sale of the televisions and (2) shipping service. The shipping service does not affect when the customer obtains control of the televisions, assuming the shipping service is distinct. Manufacturer will recognize revenue allocated to the sale of the televisions when control transfers to the customer (that is, upon shipment) and recognize revenue allocated to the shipping service when performance occurs.

Since Manufacturer is arranging for the shipment to be performed by another party (that is, a third-party carrier), it must also evaluate whether to record the revenue allocated to the shipping services on a gross basis as principal or on a net basis as agent. Refer to

RR 10 for further discussion of the principal versus agent assessment.

EXAMPLE RR 3-10Identifying performance obligations — shipping and handling accounting election

Manufacturer enters into a contract with a customer to sell five flat screen televisions. The customer requests that Manufacturer arrange for delivery of the televisions. The delivery terms state that legal title and risk of loss pass to the customer when the televisions are given to the carrier.

The customer obtains control of the televisions at the time they are shipped and can sell them to another party. Manufacturer is precluded from selling the televisions to another customer (for example, redirecting the shipment) once the televisions are picked up by the carrier at Manufacturer’s shipping dock. Manufacturer elects to account for shipping and handling activities as a fulfillment cost.

How many performance obligations are in the arrangement?

Analysis

There is one performance obligation in the arrangement because Manufacturer has elected to account for shipping and handling activities as a fulfillment cost. Manufacturer will recognize revenue and accrue the shipping and handling costs when control of the televisions transfers to the customer upon shipment. Manufacturer does not need to assess whether it is the principal or agent for the shipping service since the shipping service is not accounted for as a promise in the contract. Manufacturer should disclose its election with its accounting policy disclosures.

View image

View image