6.7 Classification of awards issued by "pass-through" entities

Publication date: 30 Apr 2024

us Stock-based compensation guide

It is often difficult to determine the appropriate classification (liability or equity) of awards granted to employees of partnerships, limited liability companies (LLCs) and similar pass-through entities. Awards granted by pass-through entities may be akin to equity interests or profit sharing/bonus arrangements. This is because the underlying equity on which these awards are granted may contain rights that differ from other equity instruments of the entity (e.g., a capital interest).

There is no authoritative guidance specific to this determination and, therefore, no "bright lines" between an equity interest versus a "profit sharing" arrangement that is more akin to a bonus (i.e., liability). Thus, judgment is required in making that assessment.

In March 2024, the FASB issued ASU 2024-01, Scope Application of Profits Interests and Similar Awards, which reformats some of the scope guidance in ASC 718-10-15-3 and adds an illustrative example (Example 10) in ASC 718-10-55-138 through 55-148. The ASU is intended to help entities determine whether profits interest and similar awards are in the scope of ASC 718, Stock Compensation.

The ASU solely focuses on scope and does not address guidance on recognition, classification, attribution, or measurement. For PBEs, it is effective for annual periods beginning after December 15, 2024 and interim periods within those annual periods. For all other entities, it is effective for annual periods beginning after December 15, 2025. Early adoption is permitted for both interim and annual financial statements. The amendments would be applied either (1) retrospectively to all prior periods presented in the financial statements or (2) prospectively to profits interest and similar awards granted or modified on or after the date at which the entity first applies the amendments.

The terms of a "profits interest award" in a pass-through entity vary from plan to plan. Depending on the terms of the award, the interest may be similar to the grant of an equity interest, a stock option, a stock appreciation right, or a profit-sharing arrangement. A profits interest award should be accounted for based on its substance.

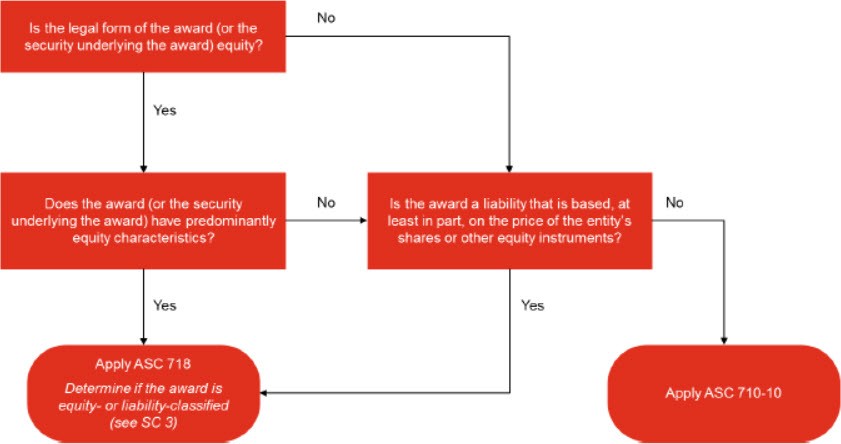

A profits interest award that is, in substance, a profit-sharing arrangement or performance bonus would generally not be within the scope of the stock-based compensation guidance (ASC 718) and would be accounted for under the guidance for deferred compensation plans (ASC 710-10), similar to a cash bonus. However, if the award is akin to a performance bonus settled in cash but the amount payable under the award is based, at least in part, on the price of the company's shares or other equity instruments, the arrangement would be accounted for as a liability award in the scope of ASC 718.

While the illustrative example in ASC 718-10-55-138 through 55-148 provides scoping considerations based on the terms of certain plan designs, judgment will still be required for arrangements whose terms differ from the example.

If it is determined that an award (or the underlying security) has predominantly equity characteristics (even if junior to other classes of equity interests), it is subject to the scope of the ASC 718. An assessment should then be performed to determine whether features of the award result in liability classification under ASC 718. For example, an award that is equity both in legal form and in substance might still be liability-classified under ASC 718 due to a repurchase feature based on a formula. Refer to SC 3.

In many cases, these arrangements will have features that are both similar to equity and liabilities. Some characteristics should be considered to bear more weight than others, depending on the specific facts and circumstances of the entity and the arrangement. A key consideration is often understanding an employee's rights upon a voluntary termination. If an employee is only entitled to share in profits while providing employee service and forfeits those rights upon termination of employment, the arrangement would generally be considered akin to a profit-sharing arrangement or performance bonus, not an equity award.

Figure SC 6-3 provides a flowchart to determine the appropriate accounting model for awards granted to employees of pass-through entities.

Figure SC 6-3 Scoping of awards granted to employees of pass-through entities

The following provides a list of the general characteristics to consider when determining whether an award (or the underlying security) has predominantly equity or liability characteristics. This list is not all inclusive.

The following are equity characteristics

of awards to employees of "pass-through" entities:

Legal form of the security is equity

Voting rights commensurate with ownership interest

Liquidation rights (Rights to net assets of entity on liquidation. Liquidation rights that are proportionate to other equity holders of a similar class is an equity-like characteristic)

Pre-emptive rights (The right of current shareholders to maintain their fractional ownership of a company by buying a proportional number of shares of any future issue of common stock). This may be in the form of drag-along or tag-along rights where employees have the option or obligation to sell their shares in situations in which the controlling shareholder(s) transfers control of the company, generally under the same terms and in the same proportion.

Distributions proportionate to ownership interest. (Instrument participates in the residual returns of the entity's net assets in a manner consistent with equity ownership, even if junior to other classes of equity interests)

Rights upon sale of the company commensurate with equity ownership. (Instrument participates in the same form of consideration, such as stock or debt, received from a buyer as do other equity holders, rather than receiving cash.)

Initial investment required

Risk of loss of initial capital (Some arrangements require the employee to "purchase" the equity interest, subject to certain vesting provisions or repurchase features. If the employee has risk of loss of this initial investment, it is an equity-like characteristic.)

Claims to net assets subordinate to debt holders

Interest is transferable after vesting

Employee can retain vested interests on termination of service

Employee is subject to risks and rewards of equity ownership

Management's intent is to provide the employee an equity ownership interest in the entity

The following are liability characteristics

of awards to employees of "pass-through" entities:

Little or no investment required (It is common that no investment is required in stock compensation arrangements. Thus, it is reasonable that this factor could be outweighed by other equity characteristics.)

Repurchase features (puts/calls) based on a formula (e.g., a fixed multiple of EBITDA)

Off-market employer call feature linked to employment (e.g., if an employer can terminate the employee and call the award at lower than fair value, this is not an equity-like characteristic.)

Rights to share in distributions tied to employment (e.g., if employees forfeit their award for no consideration upon termination, their rights are tied to employment.)

Holder entitled to cash upon sale of the company, regardless of the form of consideration paid by the buyer. (Instrument does not participate in the same form of consideration from the buyer as do equity holders.)

Other cash settlement provisions

Creditor-like features (e.g., fixed redemption date)

Management's intent is to provide a performance bonus by allowing employee to share in profits and distributions of the entity only during employment

Profits interest is used in lieu of cash performance bonuses

Profits interest used instead of cash bonuses for preferential tax treatment (If cash bonuses were paid, these would be immediately taxable to the employee as ordinary income. Under profits interest structure, tax is deferred until realization and taxed at capital gains rates.)

Example SC 6-1 and Example SC 6-2 illustrates the accounting for the grants of profits interest awards.

EXAMPLE SC 6-1 Grant of profits interest award that is forfeited upon termination

SC LLC grants a profits interest award to its employee. The award vests ratably over a four-year period. Once vested, the holder is entitled to receive distributions proportionate to their ownership interest. However, if the employee voluntarily leaves employment or is terminated, the interest is forfeited for no consideration.

How should SC LLC account for this profits interest award?

Analysis

In this fact pattern, the profits interest award is akin to a profit-sharing arrangement or performance bonus, not an equity award. SC LLC should account for the award similar to a cash bonus plan under ASC 710, accruing cost over the relevant service period when distributions that the holder is entitled to receive are probable and reasonably estimable. See PEB 6.3. Upon termination, the employee forfeits all rights to future distributions and receives no consideration for their interest. The holder never bears the risks and rewards of equity ownership and the amount payable under the award is not based, even in part, on the price of the entity’s shares or other equity instruments. Therefore, this award is not a share-based payment in the scope of ASC 718.

The award in this example is different than the award in ASC 718-10-55-142 through 55-144, Case B, as that award vests upon an exit event and can be retained by the grantee after termination of employment. Further, the award in this example is different than the award in ASC 718-10-55-145 through 55-146, Case C, as that award vests and is settled in cash upon an exit event (including an IPO). In this example, even upon an IPO there is no settlement of the award. The grantee simply continues to be entitled to any future distributions until termination of employment.

EXAMPLE SC 6-2 Grant of profits interest award that can be held beyond termination

SC LLC grants a profits interest award to its employee. The award vests ratably over a four-year period. Once vested, the holder is entitled to distributions and liquidation and pre-emptive rights proportionate to their ownership interest and participates in the same form of consideration as other equity holders in the event of a sale of the entity. If the employee voluntarily leaves employment or is terminated without cause, SC LLC has a call option to repurchase the vested interests at fair value on the repurchase date. SC LLC has the ability to delay the repurchase of the vested interests for at least six months to allow the employee to bear the risks and rewards of ownership. Unvested interests are forfeited for no consideration upon termination.

How should SC LLC account for this profits interest award?

Analysis

While all facts and circumstances should be considered, SC LLC would likely conclude that the profits interest award is a form of share-based compensation under ASC 718. The employee will participate in future operating and capital transactions of the entity in the same fashion as other equity holders, proportionate to their interest. Upon termination, the employee can either retain their interest or it may be repurchased at fair value which, again, is consistent with bearing the risks and rewards of equity ownership. Therefore, this award is likely a share-based payment in the scope of ASC 718.

The remaining provisions of ASC 718-10-25-6 to ASC 718-10-25-18 should be evaluated to determine the appropriate classification of the award as equity or liability. If it is determined to be an equity-classified award, SC LLC should determine the grant date fair value of the profits interest and recognize it over the requisite service period as described in SC 2.8. If it is determined to be a liability-classified award, SC LLC should remeasure the award each reporting period at either its fair value or intrinsic value, depending on its accounting policy for liability-classified awards (as described in SC 6.2.2). In this example, SC LLC would likely determine that the profits interest award is equity-classified.

When determining the fair value of a profits interest that may be junior to other classes of equity interests (and might not participate in any distributions or proceeds until the more senior classes have received specified amounts or specified returns), the potential upside appreciation of the interest must be considered, similar to an at-the-money stock option. It would generally not be appropriate, for example, to value the profits interest based on a hypothetical liquidation of the entity and application of the distribution “waterfall” as of the grant date.

1 If an award (or the underlying security) has predominant characteristics of equity, it is subject to the guidance in ASC 718. However, the award might require liability classification based on the provisions in ASC 718. For example, certain repurchase features could require liability classification despite the fact that the instrument underlying the award has the equity characteristics in this list.

2 If an award (or the underlying security) is determined to predominately have characteristics of a liability, generally it is subject to the guidance in ASC 710-10. However, liabilities for which the amount payable is based, at least in part, on the price of the company's shares or other equity instruments are liability awards in the scope of ASC 718.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.