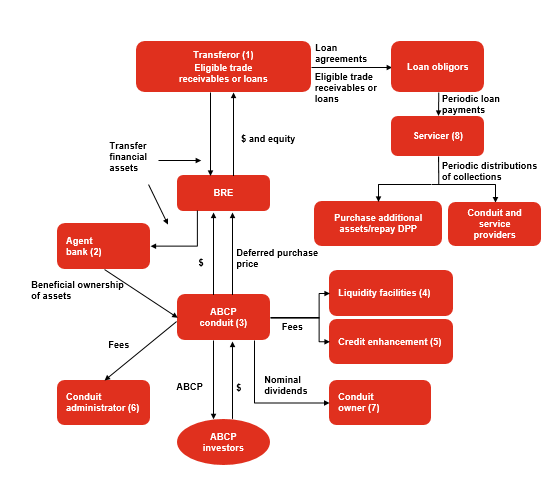

To accelerate receipt of operating cash flows, companies sometimes transfer (sell) trade receivables or short-term consumer loans to a multi-seller asset-backed commercial paper conduit ("conduit"), a limited-purpose securitization entity sponsored and administered by a bank. As the name implies, these entities are structured to acquire receivables from numerous originators (sellers), financed by issuing commercial paper. Although cash collections on the acquired receivables are intended to fully repay the commercial paper, the sponsor bank (sometimes in tandem with other banks) provides liquidity support and credit enhancement to the vehicle. These facilities provide additional assurance to investors that the conduit will have the ability to redeem its commercial paper when due, even in the event of major market disruption or if the conduit’s assets experience significant unanticipated credit issues. Each seller of receivables also provides credit support to the conduit through the deferred purchase price construct, discussed below.

For various reasons, a conduit typically does not directly purchase the receivables sold by each originator. Rather, as Figure TS 1-5 illustrates, the sponsoring bank of the conduit (or, if multiple conduits are providing financing, one of the conduits’ sponsoring banks), in its capacity as agent for the conduit, will acquire legal title to the receivables transferred by each seller. The agent bank holds the receivables for the benefit of the participating conduits, each of which in turn acquires a beneficial interest in the transferred receivables corresponding to its financing commitment.

In exchange for selling the receivables to the agent bank, the seller receives cash from the conduits for a portion of the purchase price, and a beneficial interest (an obligation of the conduits) for the remainder. This beneficial interest, which is subordinated to the conduits’ investment in the receivables pool, is commonly referred to as the deferred purchase price (DPP) in the industry. The DPP will absorb first any credit losses incurred on the receivables sold, as well as collection timing risk. The DPP is sized to ensure that, under virtually all scenarios, the conduit will not incur a loss on its investment in the receivables pool.

Most financing arrangements with conduits are "revolving;" the seller continues to periodically transfer receivables to the agent bank in exchange for cash and DPP until the arrangement terminates at a prescribed date. Assuming the conduit has fully funded its contractual financing commitment, the cash component of the purchase price for these subsequent transfers can be funded solely from collections from receivables previously sold to the agent bank. The difference between the cash paid and the all-in purchase price of the transferred receivables is "funded" by a corresponding increase in the seller’s DPP.

At the termination date prescribed, the seller may no longer sell additional receivables to the agent bank, and the arrangement enters "amortization" status. Subsequent collections on the receivables previously transferred are used first to repay the conduit’s investment in the pool. Any remaining collections inure to the seller (return of its DPP). In certain cases, the seller may wind up the arrangement by exercising a servicer clean up call after the principal amount of the receivables pool has declined to a prescribed level.

The banking entity that sponsors a conduit is frequently its consolidator (primary beneficiary) under

ASC 810,

Consolidation, stemming from the bank’s involvement in the conduit’s design, bank-provided credit enhancements and liquidity facilities, and the bank’s role as the conduit’s administrator. Assuming that a conduit owns financial assets sourced from multiple sellers at any point in time, it would be rare for a seller to consolidate the conduit.

Figure TS 1-5 illustrates the typical conduit financing arrangement and the principal parties involved.

Figure TS 1-5

Multi-seller asset-backed commercial paper conduit

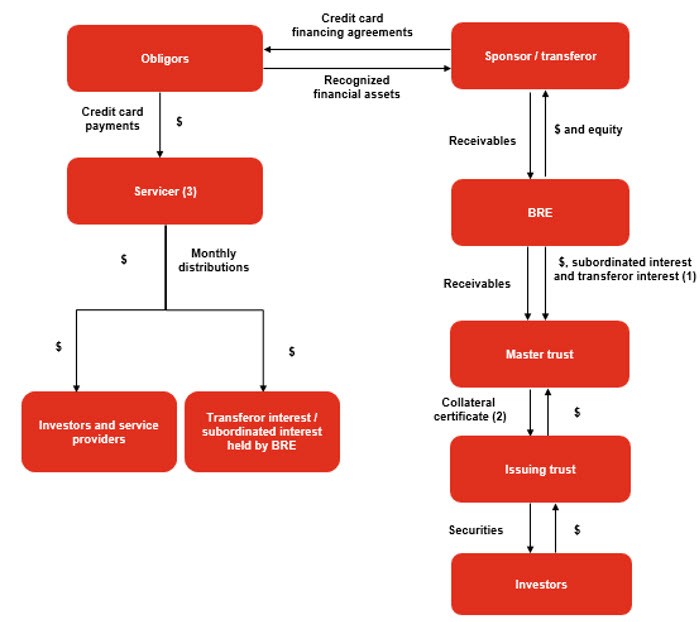

View image

View image

(1) Multiple sellers will transfer eligible financial assets to the typical asset-backed commercial paper conduit; only one transferor is shown here for convenience.

(2) An agent bank (usually the sponsor of the conduit) acquires legal title to the financial assets sold by the BRE, and holds them for the benefit of the conduit, which funds the purchase price. If multiple conduits are involved, each will provide funding in proportion to its financing commitment.

(3) Typically, a limited-liability corporation established in Delaware.

(4) One or more banks will provide liquidity backup facilities intended to fund any cash flow shortfalls between maturing commercial paper and cash inflows from assets or newly-issued commercial paper.

(5) Program-wide credit enhancement, typically written by one or more banks, serves as a backup facility to fund any shortfalls remaining after liquidity facilities have been drawn.

(6) The conduit administrator (usually the sponsoring bank) directs the significant operations of the conduit, including negotiating with sellers, maintaining support arrangements, and managing the commercial paper program.

(7) Typically, a service company that provides officers and ensures that the conduit observes all corporate formalities. The owner receives dividends in exchange for its nominal equity investment.

(8) Each seller services the financial assets sold to the agent bank, and reinvests collections received on those assets to fund periodic sales of additional assets to the agent bank.

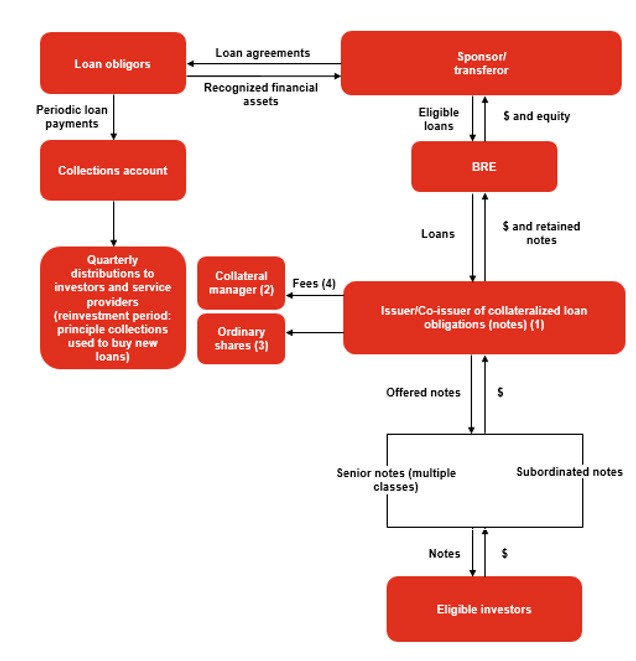

View image

View image

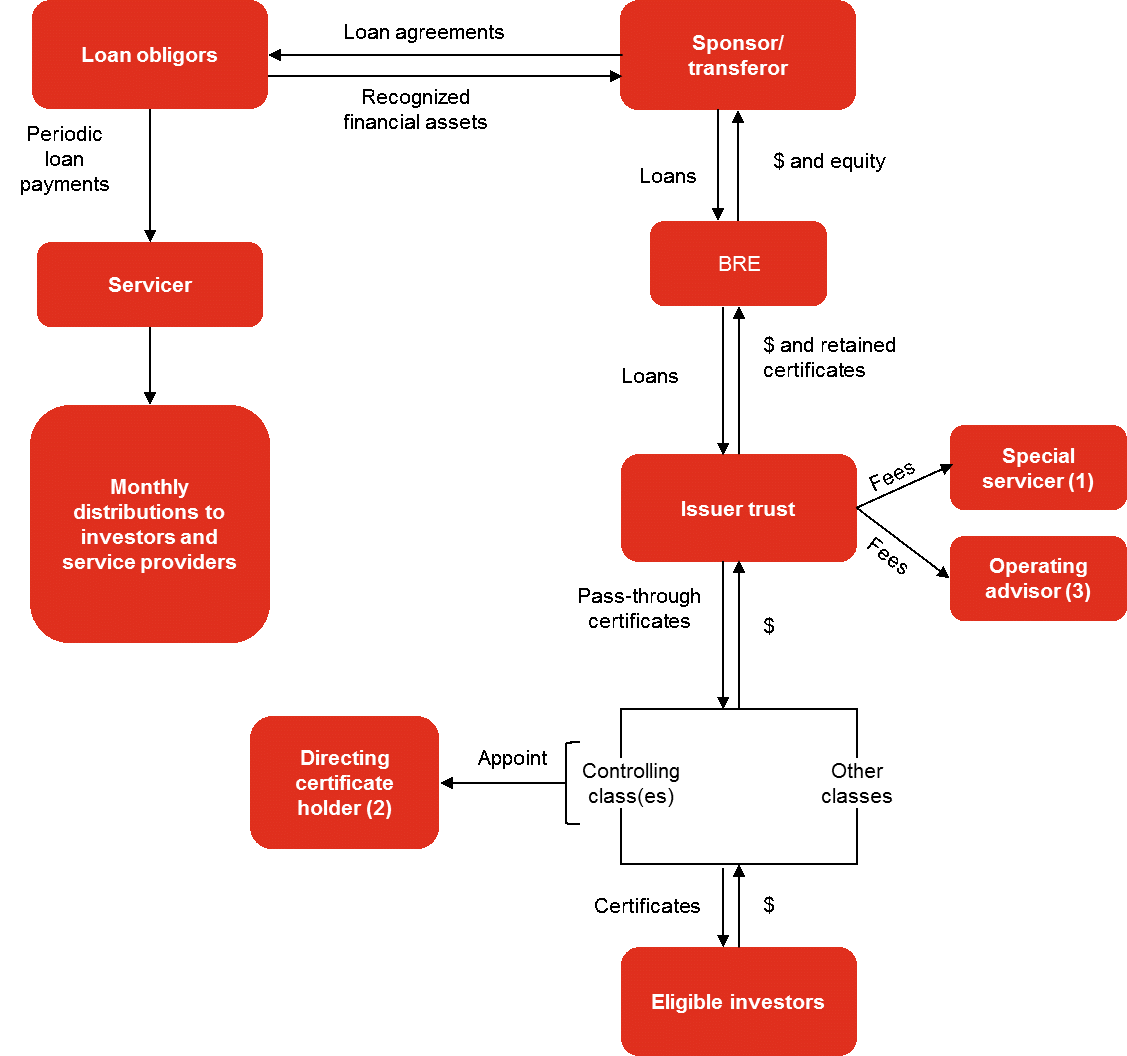

View image

View image