Search within this section

Select a section below and enter your search term, or to search all click Transfers and servicing of financial assets

Favorited Content

Transferor Corp |

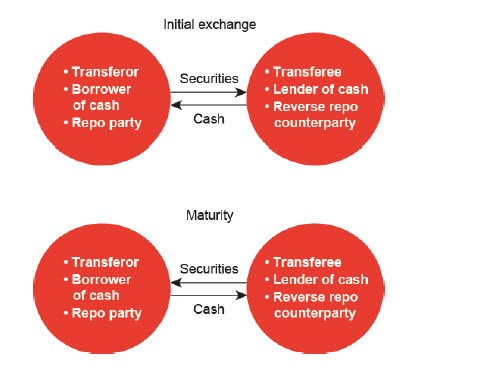

Transferee Corp |

|||||||

|---|---|---|---|---|---|---|---|---|

At inception:

|

At inception:

|

|||||||

Dr. Cash

|

$980

|

Dr. Reverse repo agreements

|

$980

|

|||||

Cr. Obligation under repo agreements

|

$980

|

Cr. Cash

|

$980

|

|||||

To record the receipt of cash and obligation under repo agreement

|

To record transfer of cash to Transferor Corp in exchange for security (noncash collateral)

|

|||||||

Dr. Securities pledged to Transferee Corp

|

$1,000

|

|||||||

Cr. Securities

|

$1,000

|

|||||||

To reclassify pledged security that Transferee Corp has the right to sell or repledge

|

Transferee Corp does not recognize the security (noncash collateral) on its balance sheet. An obligation to return the security is recorded only if Transferee Corp on-sells it.

|

|||||||

Dr. Money market instrument

|

$980

|

|||||||

Cr. Cash

|

$980

|

|||||||

To record investment of cash collateral

|

||||||||

At conclusion:

|

At conclusion:

|

|||||||

Dr. Cash

|

$985

|

Dr. Cash

|

$984

|

|||||

Cr. Interest income

|

$5

|

Cr. Reverse repo agreements

|

$980

|

|||||

Cr. Money market instrument

|

$980

|

Cr. Interest income

|

$4

|

|||||

To record results of short-term cash investment

|

To record receipt of cash upon maturity of reverse repo agreement and related interest income

|

|||||||

Dr. Obligation under repo agreements

|

$980

|

|||||||

Dr. Interest expense

|

$4

|

|||||||

Cr. Cash

|

$984

|

|||||||

To record repayment of repo obligation and related interest (security’s repurchase price) |

||||||||

Dr. Securities

|

$1,000

|

|||||||

Cr. Securities pledged to Transferee Corp

|

$1,000

|

|||||||

To reclassify security no longer pledged |

||||||||

Transferor Corp |

Transferee Corp |

||||||||

|---|---|---|---|---|---|---|---|---|---|

At inception:

|

At inception:

|

||||||||

Dr. Cash

|

$980

|

Dr. Reverse repo agreements

|

$980

|

||||||

Cr. Obligation under repo agreements

|

$980

|

Cr. Cash

|

$980

|

||||||

To record the receipt of cash and obligation under repo agreement

|

To record transfer of cash to Transferor Corp in exchange for security (noncash collateral)

|

||||||||

Dr. Securities pledged to Transferee Corp

|

$1,000

|

||||||||

Cr. Securities

|

$1,000

|

||||||||

To reclassify pledged security that Transferee Corp has the right to sell or repledge

|

Transferee Corp does not recognize the security (noncash collateral) on its balance sheet. An obligation to return the security is only recorded when Transferee Corp sells the security.

|

||||||||

Dr. Money market instrument

|

$980

|

||||||||

Cr. Cash

|

$980

|

||||||||

To record investment of cash collateral

|

|||||||||

When collateral is pledged:

|

When collateral is pledged:

|

||||||||

Dr. Cash

|

$980

|

||||||||

Transferor Corp does not record an entry when Transferee Corp repledges the collateral.

|

Cr. Obligations under repo agreements

|

$980

|

|||||||

To record the sale of the security (noncash collateral)

|

|||||||||

Dr. Money market investment

|

$980

|

||||||||

Cr. Cash

|

$980

|

||||||||

To record investment of cash received from on-selling the security

|

|||||||||

At conclusion:

|

At conclusion:

|

||||||||

Dr. Cash

|

$985

|

Dr. Cash

|

$982

|

||||||

Cr. Interest income

|

$5

|

Cr. Interest Income

|

$2

|

||||||

Cr. Money market instrument

|

$980

|

Cr. Money market instrument

|

$980

|

||||||

To record results of short-term cash investment

|

To record results of short-term cash investment

|

||||||||

Dr. Securities

|

$1,000

|

Dr. Obligations under repo agreements

|

$980

|

||||||

Cr. Securities pledged to Transferee Corp

|

$1,000

|

Cr. Cash

|

$980

|

||||||

To reclassify security no longer pledged

|

To record return of on sold security and cash collateral [note: interest expense omitted for sake of simplicity]

|

||||||||

Dr. Obligation under repo agreements

|

$980

|

Dr. Cash

|

$984

|

||||||

Dr. Interest expense

|

$4

|

Cr. Reverse repo agreements

|

$980

|

||||||

Cr. Cash

|

$984

|

Cr. Interest income

|

$4

|

||||||

To record repayment of repo principal and interest (security’s repurchase price)

|

To record the receipt of cash upon maturity (unwind) of reverse repo agreement

|

||||||||

Transferor Corp |

Transferee Corp |

|||||

|---|---|---|---|---|---|---|

At inception:

|

At inception:

|

|||||

Dr. Cash

|

$980

|

Dr. Reverse repo agreements

|

$980

|

|||

Cr. Obligation under repo agreements

|

$980

|

Cr. Cash

|

$980

|

|||

To record the receipt of cash and obligation under the repo agreement

|

To record transfer of cash to the repo counterparty in exchange for pledged security

|

|||||

Transferor Corp does not reclassify the pledged security because Transferee Corp does not have the right to sell or repledge it.

|

||||||

Dr. Money market instrument

|

$980

|

|||||

Cr. Cash

|

$980

|

|||||

To record investment of cash collateral

|

||||||

At conclusion:

|

At conclusion:

|

|||||

Dr. Cash

|

$985

|

|||||

Cr. Interest income

|

$5

|

|||||

Cr. Money market instrument

|

$980

|

|||||

To record results of short-term cash investment

|

||||||

Dr. Obligation under repo agreements

|

$980

|

Dr. Cash

|

$984

|

|||

Cr. Interest expense

|

$4

|

Cr. Reverse repo agreements

|

$980

|

|||

Cr. Cash

|

$984

|

Cr. Interest income

|

$4

|

|||

To record the repayment of repo principal and interest

|

To record the receipt of cash upon maturity (unwind) of reverse repo agreement

|

|||||

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Transfers and servicing of financial assets