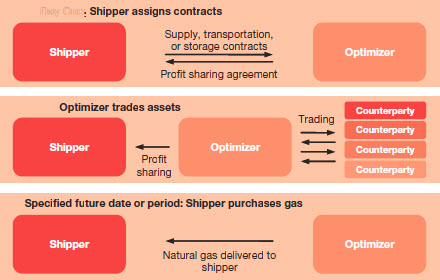

Figure UP 5-9 depicts a typical natural gas optimization agreement.

Figure UP 5-9

Typical natural gas optimization agreements

Reporting entities may enter into arrangements with third parties to manage their natural gas supply, transportation, storage, or any combination thereof. These arrangements are generally referred to as asset optimization agreements or natural gas optimization agreements. The terms of the agreements vary and each arrangement should be considered based on the specific facts and circumstances. In a typical natural gas optimization arrangement, the reporting entity (the shipper) transfers title to any combination of some or all of its natural gas supply, transportation, and storage contracts to a financial intermediary (the asset optimizer or optimizer). In some cases, the shipper retains full title to its underlying contracts. The optimizer is usually required to sell a specified supply of natural gas to the shipper in accordance with a predetermined schedule, although some agreements permit the natural gas to be called by the shipper when needed. During the contract period, the asset optimizer will trade the assets to maximize its return based on market price fluctuations.

In many respects, natural gas optimization agreements are similar to physical or virtual storage and park and loan transactions. Key characteristics of a natural gas optimization arrangement include:

- It is predetermined that the asset optimizer will trade the assets.

- The profits generated from the trading activity are shared with the shipper in the form of a monthly fee, a percentage of profits, or some combination thereof.

In this type of arrangement, the shipper benefits from a reduced cost of its natural gas supply and storage. It may retain these benefits, or in the case of a regulated utility, it may share them with its customers in the form of reduced rates.

In considering the accounting for a natural gas optimization agreement, the reporting entity needs to assess the overall natural gas optimization agreement (which provides the overall rights and obligations of the shipper and the optimizer), as well as any embedded forward or option agreements (e.g., the forward sale of natural gas supply from the optimizer to the shipper).

In evaluating this type of arrangement, the reporting entity should follow the commodity contract accounting framework discussed in

UP 1. In some cases, one arrangement may include various components that are subject to different accounting models. Although the accounting will vary depending on facts and circumstances, lease accounting is usually not applicable unless the arrangement involves the right to use identified property, plant, or equipment (e.g., a storage facility). In addition, the contracts are usually not derivatives in their entirety. Because the natural gas optimization agreement contains multiple elements, including the trading of transportation and storage and the delivery of natural gas, these agreements typically do not meet the net settlement criterion.

However, an asset optimization contract may contain one or more embedded derivatives requiring separation. As described above, asset optimization agreements typically include forward and, at times, option contracts for the purchase of natural gas from the financial intermediary. These types of contracts would be derivatives on a stand-alone basis; therefore, further analysis is required to determine if they should be separated from the host contract. In accordance with

ASC 815-15-25-1, an embedded derivative should be separated from its host contract and accounted for as a derivative if three criteria are met.

As summarized in Figure UP 5-10, asset optimization agreements typically include an embedded derivative instrument that should be recognized at fair value in the financial statements of the shipper; however, the terms and conditions of each arrangement should be evaluated. See

UP 3.4 for further information on the evaluation of embedded derivatives.

Figure UP 5-10

Does an asset optimization agreement contain an embedded derivative that requires separation from the host?

Guidance | Evaluation | Comments |

Economic characteristics of the embedded are not clearly and closely related to the host

| |

- The host contract is determined based on the nonderivative elements; typically natural gas storage or capacity.

- The embedded elements (e.g., natural gas supply) are separate deliverables; they are generally not clearly and closely related to the host contract.

- See UP 3.4.3 for information on evaluating the clearly and closely related criterion.

|

Hybrid instrument is not remeasured at fair value under otherwise applicable US GAAP

| |

- The asset optimization agreement is not remeasured at fair value.

|

A separate instrument with the same terms as the embedded derivative would be a derivative instrument subject to ASC 815 | |

- A firm commitment to receive natural gas in the future would generally meet the definition of derivative.

- The separated embedded derivative may be eligible for hedge accounting in some circumstances (see the response to Question UP 5-4).

|

The following example illustrates the journal entries for an asset optimization agreement.

EXAMPLE UP 5-6

Natural gas optimization of supply and transportation

On May 1, 20X1, Rosemary Electric & Gas Company enters into a natural gas optimization agreement for its natural gas supply and capacity with Big Bank. As a result, it transfers title to a natural gas supply arrangement for 10,000 MMBtus of natural gas and also assigns a related capacity agreement. Big Bank receives the initial delivery of natural gas directly from REG’s supplier and is required to sell 10,000 MMBtus of natural gas to REG on December 1, 20X1 for $5/MMBtu. In the interim, Big Bank can trade both the natural gas supply and natural gas capacity. REG receives an optimization fee of $1,000 per month from Big Bank, regardless of the optimization activities. On December 1, 20X1, REG receives the natural gas from Big Bank.

For purposes of this example, the spot and forward prices of natural gas (forward price for delivery in December 20X1) are as follows ($/MMBtu):

How should REG account for the natural gas optimization agreement?

Analysis

The agreement does not contain a lease because there is no identified asset. Further, the arrangement does not meet the definition of a derivative in its entirety because of the lack of net settlement related to the pipeline capacity component of the agreement. However, the natural gas optimization agreement is a hybrid instrument comprising the host contract (the capacity agreement, which is a nonderivative component) and an embedded forward natural gas purchase agreement. The forward natural gas purchase agreement is not clearly and closely related to the host, so it should be separated and accounted for as a derivative at fair value on a recurring basis. See the response to Question UP 5-6 for information on evaluating whether the forward agreement can be accounted for as a normal purchases and normal sales contract.

REG would record the following journal entries to account for this agreement (amounts in $000s).

| Date | Journal entries | Cash | Fuel inventory | Derivative | Income statement |

| |

No accounting by REG for

initial delivery of contracts to

Big Bank (see note 1)

| | | | |

| |

Record change in value of

forward natural gas purchase

(10,000 × ($5.00 – $4.50))

| | | ($5) | $5 |

| |

Record optimization fee

($1,000 × 2 months)

(see note 2)

| $2 | | | (2) |

| |

Record change in value

(10,000 × ($4.50 – $5.50))

| | | 10 | (10) |

| |

Record optimization fee

($1,000 × 3 months)

(see note 2)

| 3 | | | (3) |

| |

Record change in value

(10,000 × ($5.50 – $6.00))

| | | 5 | (5) |

| |

Record delivery of natural gas

from Big Bank and effective

“settlement” of embedded

derivative

| (50) | 50 | (10) | 10 |

| |

Record optimization fee

($1,000 × 2 months)

(see note 2)

| 2 | | | (2) |

|

Note 1: This example assumes that the contracts were at the money at the time of transfer to Big Bank. The contract terms may be modified to include an initial receipt or payment of cash or other compensation if the contracts were in or out of the money at the time of transfer. In such case, additional journal entries would be required. See the response to Question UP 5-6 for information on the potential implications if the initial supply agreements were previously designated as normal purchases or normal sales.

Note 2: The optimization fee journal entry would be recorded on a monthly basis. To simplify this example, a cumulative entry is recorded on a quarterly basis.

The example has been simplified to include only one receipt of natural gas from Big Bank on December 1, 20X1 and a simple profit-sharing fee in the form of a monthly payment from Big Bank to REG. In practice, there may be different variations of the profit sharing (e.g., a split percentage of the profits once trading revenues reach a certain level). Further, the shipper may receive natural gas supply, capacity, as well as storage rights at varying times over the arrangement.

Question UP 5-6

Can a reporting entity apply the normal purchases and normal sales scope exception to natural gas supply agreements that have been transferred into an asset optimization arrangement?

PwC response

No. As discussed in

ASC 815-10-15-36, gross physical delivery is required for a contract to qualify for the normal purchases and normal sales scope exception. Once a reporting entity transfers supply contracts to an asset optimizer, it no longer receives gross physical delivery of the natural gas under the original purchase agreement. Ultimately, the reporting entity will receive deliveries of natural gas from the asset optimizer, but it has suspended deliveries from its original supplier due to the optimization contract. In addition, because it will be sharing in profits through optimization fees for the trading activities associated with those supply contracts, the reporting entity has effectively net settled the contracts.

Further, a transfer of natural gas supply arrangements that were previously designated under the normal purchases and normal sales scope exception into an asset optimization agreement will taint the contracts. This requires de-designation of the transferred contracts (as they were effectively net settled) and may also impact current and future similar contracts. See

UP 3.3.1 for further information about tainting and the normal purchases and normal sales scope exception.