Single power plant entities are commonly set up as limited liability companies; however, they may also take the form of corporations, general partnerships, or limited partnerships. These structures are designed as follows:

- Corporation — a legal entity that is separate and distinct from its owners that offers limited liability for shareholders.

- General partnership — an association in which each partner has unlimited liability.

- Limited partnership — an association in which one or more general partners have unlimited liability and one or more partners have limited liability. A limited partnership is usually managed by the general partner or partners, subject to limitations, if any, imposed by the partnership agreement.

- Limited liability company — companies with characteristics of both corporations and partnerships; however, they are dissimilar from both in certain respects. Examples of these characteristics are discussed in Figure 9-4 in the context of evaluating the appropriate accounting model for the investor. They include considerations such as which parties have limited and unlimited or personal liability, tax liability, and control and/or management ability.

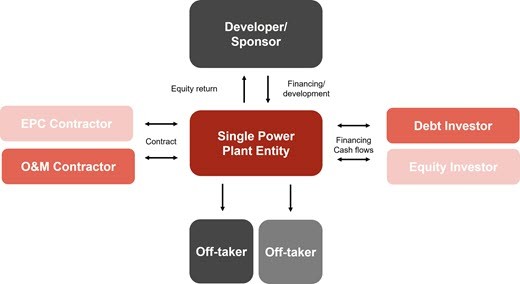

Regardless of the legal structure, single power plant entities generally involve a number of parties, including a variety of investors and off-takers from the power plant. Figure UP 9-1 illustrates the potential parties involved in a typical structure.

Figure UP 9-1

Sample structure for a single power plant entity

The relationships of the various parties to the single power plant entity typically include:

The developer generally has equity ownership in the project and responsibility for the formation, construction, and operation of the plant. The developer may contribute cash, contractual rights, expertise, and/or physical assets to the single power plant entity in exchange for its equity interest. Physical assets and contractual rights contributed may include land, property, or equipment, offtake agreements, permits, and emission credits (credits required to build the power plant or credits needed for commercial operation).

- Financial investors — equity

A single power plant entity may involve one or more equity investors who contribute cash or other assets in exchange for their interest in the entity. Equity investments can be in the form of traditional voting equity, passive participation (such as tax equity), or another form of equity ownership such as preference shares. Tax equity owners invest to benefit from a return generated at least partially by government incentives such as grants, investment tax credits, or production tax credits along with other tax attributes that come with tax ownership (e.g., tax depreciation). See

UP 16 for information on accounting for government incentives.

- Financial investors — debt

A power plant project may have one or more debt investors. Debt interests are typically collateralized by the assets of the project and in most cases, debt holders have no recourse to other assets of the investors or developer in the event of default. In some cases, however, the debt interests may be guaranteed by the developer or other party. Debt holders are usually passive participants, although debt agreements generally include standard creditor rights.

Unless the developer is also a builder, the single power plant entity will typically enter into an engineering, procurement, and construction (EPC) contract. Once the plant becomes operational, a third-party contractor or the EPC contractor may provide ongoing operations and maintenance (O&M) services. These contracts are generally executed between the single power plant entity and the related contractors, although the owners of the entity may provide a guarantee of payments.

One or more parties may agree to purchase the power, capacity, and/or other attributes of the facility (e.g., renewable energy credits) through contractual arrangements. These agreements are often required as a condition of financing. In other cases, the power plant may operate as a merchant facility, whereby all output is sold on the open market.

One common type of structure that is used for renewable energy projects is referred to as a “flip structure.” In a flip structure, the developer partners with one or more third-party investors to monetize the tax benefits associated with owning a renewable energy facility. The tax investors are willing to invest in the entity to receive returns primarily through tax credits and other tax benefits, which may or may not be supplemented by a project’s underlying cash flows.

Although single power plant entity structures may vary and all facts and circumstances should be individually analyzed, a typical partnership flip structure is configured as follows:

- A developer establishes a project company (often a limited partnership or limited liability company).

- The project company invests in a renewable energy project that is eligible to receive certain tax attributes, such as tax credits and tax depreciation benefits.

- A tax investor commits to contribute the majority of equity via a cash investment in return for a majority (possibly up to 99%) of income and losses and all tax attributes (e.g., tax credits and tax depreciation) until it has recovered its initial investment plus a predetermined yield or internal rate of return.

- When the target return is reached by the tax investor, the majority of the allocation of income and losses will “flip” to the developer, along with the ownership rights in the residual value of the project.

Cash distributions to the various partners will also follow an agreed allocation percentage, which may or may not follow the same allocation used for income and losses.

Although the structures often vary, many single power plant entities incorporate differing allocations of income, losses, and cash distributions to provide targeted benefits to the various classes of owners. As a result, the accounting for these types of structures can be challenging. Management of the single power plant entity needs to assess the accounting implications related to plant construction, operations, supply agreements, and power purchase agreements.

The hypothetical liquidation at book value (HLBV) method of allocating income is often appropriate for these types of structures, for both the allocation of income to the non-controlling interests of the project, as well as for investors applying the equity method of accounting under

ASC 323. See

UP 9.6 for further discussion on the use of HLBV to allocate income.