Key points

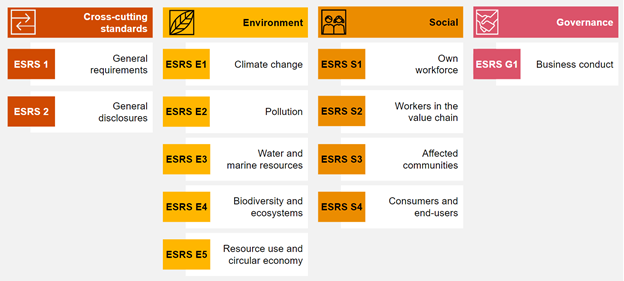

On 31 July 2023, the European Commission (EC) adopted the final delegated act of the European Sustainability Reporting Standards (ESRS). The delegated act includes the 12 finalised ESRS, made up of two cross-cutting standards, which apply to all sustainability matters, and ten topical standards covering a wide range of environmental, social and governance matters.

The delegated act includes the 12 finalised ESRS, made up of two cross-cutting standards, which apply to all sustainability matters, and ten topical standards covering a wide range of environmental, social and governance matters.

What is the issue?

The ESRS are the sustainability reporting standards that underpin the

Corporate Sustainability Reporting Directive (CSRD). The aim of the CSRD, which has been in force since January 2023, is to bring sustainability reporting on par with financial reporting. To achieve this objective, companies must provide relevant, comparable and reliable information on their sustainability-related impacts, risks and opportunities. The ESRS include detailed and standardised disclosure requirements for companies to report on environmental, social and governance matters.

The

delegated act, including its appendices, is available in all EU Member States’ languages. As noted above, the ESRS include two cross-cutting standards that define the general reporting principles and the CSRD fundamental concepts, including double materiality and reporting boundaries, as well as the overarching disclosures that are to be made by all companies in scope of the CSRD. The ten topical standards include the specific reporting requirements for environmental, social and governance matters:

The final ESRS reflect updates to the 12 previous

draft ESRS that were issued by the EC for public feedback on 9 June 2023. Responses were due by 7 July 2023. The EC received over

600 comments, including

feedback from PwC.

What are the main changes compared to the June 2023 version issued by the EC for public feedback?

The EC included an overview of significant changes compared to the draft ESRS which were handed over to the EC by EFRAG (European Financial Reporting Advisory Group) in November 2022. Based on our preliminary assessment, the changes made after the feedback period in June 2023 include:

- The terminology around financial materiality to align further with the definition of financial materiality in the IFRS sustainability disclosure standards.

- A provision within the materiality section which requires a detailed explanation when a reporting entity concludes that climate change is not a material topic.

- An additional provision to facilitate the compliance of financial markets participants, benchmarks administrators and financial institutions with their own disclosure obligations from other EU law: If the reporting entity concludes that a data point derived from such EU law is not material, it shall explicitly state that the data point in question is “not material”.

- A requirement to disclose a table with all data points derived from other EU law, indicating where they are to be found in its sustainability statement or stating “not material” as appropriate.

International interoperability

The EC has stressed the importance of the alignment of the ESRS with global standards such as the IFRS sustainability disclosure standards and the Global Reporting Initiative (GRI). In its

press release about the adoption of the ESRS, the ISSB (International Sustainability Standards Board) confirmed the high degree of alignment between its and the ESRS climate disclosures. Furthermore, interoperability guidance material from the EC, EFRAG and ISSB, which is due out shortly, should assist entities in navigating between the standards and understand where there are incremental or different disclosures required by one of the two sets of standards.

In this respect, EFRAG has recently made available

papers on the interoperability of ESRS with the GRI-standards and the IFRS sustainability disclosure-standards. These papers will be discussed during the 23 August 2023 EFRAG SRB (Sustainability Reporting Board) public session.

Phasing-in and voluntary disclosures

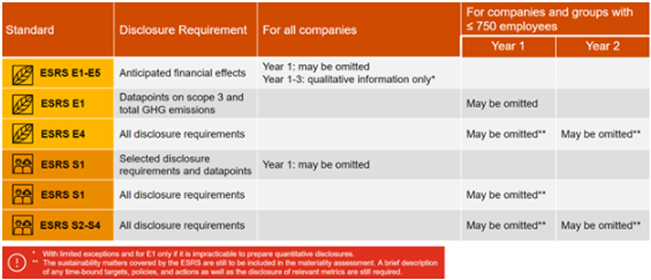

Additional phase-in reliefs and voluntary disclosures introduced in the June 2023 draft ESRS remain substantially unchanged. These are summarised below and described in more detail in our In brief 2023-13. The additional reliefs are intended to reduce the reporting burden of companies and to facilitate the first-time application of the standards.

Examples of voluntary disclosures include the transition plan for biodiversity and ecosystems (ESRS E4) and information on non-employee workers in ESRS S1 (for example, with respect to adequate wages, social protection, and health and safety). An explanation of why certain sustainability topics have been classified as not material is also a voluntary disclosure (with the exception of the climate change topic).

What are the next steps?

After the adoption of the delegated act, a two-month scrutiny period (with a possible two months’ extension) by the European Parliament and the Council of the European Union will begin. Once the scrutiny period is over and assuming neither of the co-legislators objects, the delegated act will apply from 1 January 2024.

Parallel to the legislative process, EFRAG is working on developing further guidance to support the application of the ESRS. This guidance is expected to cover the materiality assessment and the inclusion of value chain information. In addition, EFRAG has announced that it will put in place an access point for ESRS stakeholders to provide application questions on the ESRS.

Where do I get more details?

You can find more information on the recent sustainability reporting initiatives in the EU: