This In the loop was updated on April 12, 2024 to reference the issuance of the SEC’s climate-related disclosure rules.

For investors, despite an abundance of ESG data, there is often a lack of consistent, comparable, and reliable ESG information available upon which to make informed investment and voting decisions.

John Coates, Acting Director, Division of Corporation Finance,

March 11, 2021

Voices from an increasing number of constituents extoll the merits of a new age of environmental consciousness. Vocal in the crowd, investors and other stakeholders across the business spectrum see environmental, social, and governance (ESG) disclosures as a window into a company’s future. Shareholder proposals related to environmental impact are on the rise in number and level of support. And if companies weren’t already acutely aware of the need to moderate their impact on the environment, many are voluntarily responding to stakeholder demand and increasingly making climate-related commitments—net zero, carbon neutral, carbon negative. Some of these commitments and other climate-related impacts are disclosed on websites or in speeches, sustainability reports, or survey responses, which may stand in stark contrast to what is (or isn’t) said in a company’s SEC filings.

The SEC is responding to the increased disparity between public statements and what’s included in regulatory filings with increased attention to the quality and adequacy of disclosure. Issuers of securities are required to make material disclosures to facilitate investors’ informed decision making. Of course, what constitutes a material disclosure that informs decision making is subject to significant management judgment. And while management is responsible for determining what is material and ultimately disclosed in its filings, the SEC staff is charged with assessing those disclosures for compliance with the federal securities laws.

In March 2024, the SEC adopted

new rules for climate-related disclosures (see our

In depth for further details). The new rules are applicable beginning in 2026 (on 2025 information). In the meantime, it’s important for companies to continue to focus on compliance with the current requirements. This document highlights the requirements and provides insight into recent SEC comments on registrant disclosures.

| |

An old story with a renewed focus and an eye toward change

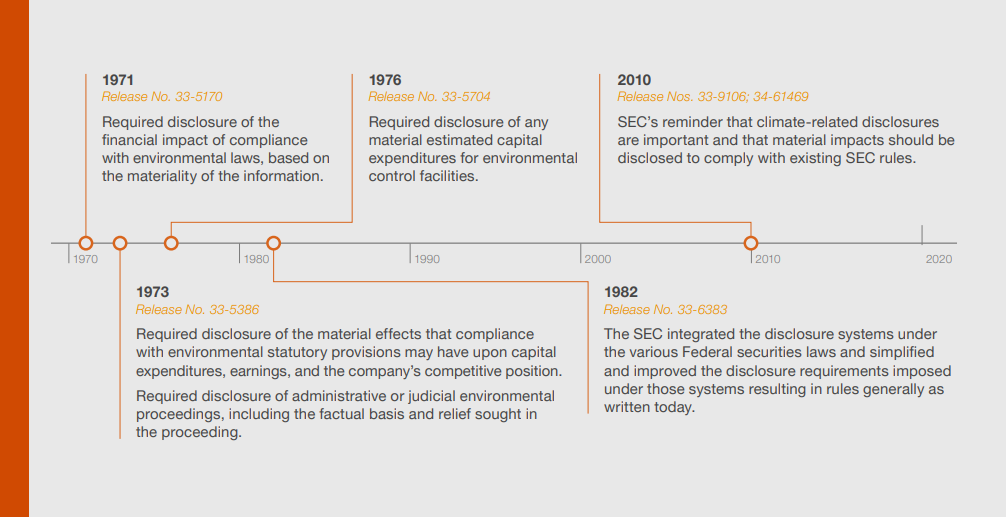

In its 2010 interpretive release outlining how existing disclosure requirements apply to climate change matters, the SEC noted that “climate change has become a topic of intense public discussion in recent years,” which is a sentiment equally, if not more, appropriate today. But even the 2010 guidance was nothing new. Since the 1970s, the SEC has asked for climate-related disclosures. After 40 years of developments, the SEC provided a roadmap in 2010 that summarized how existing requirements apply to climate-related risk. |

Today’s focus

Climate change creates direct and indirect risks for companies in nearly all industries. Investors want to know about risk because it informs their decision making.

We are long past the point at which it can be credibly asserted that climate risk is not material.

Commissioner Allison Herren Lee, Regulation S-K and ESG Disclosures: An Unsustainable Silence, August 26, 2020

| |

The following table summarizes the Regulation S-K requirements highlighted by the SEC in 2010. Companies have a responsibility to assess whether a material exposure in the following areas merits disclosure, and audit committees should understand management’s assessment.

|

Regulation S-K Item | Disclosures applicable to climate-related matters |

Description of business

Item 101 requires a registrant to describe its business and that of its subsidiaries.

|

- The material effects that compliance with government regulations, including environmental regulations, may have upon the capital expenditures, earnings, and competitive position of the registrant and its subsidiaries, including the estimated capital expenditures for environmental control facilities

- Resources material to a registrant’s business, such as sources and availability of raw materials

|

Legal proceedings

Item 103 requires a registrant to briefly describe any material pending legal proceeding to which it or any of its subsidiaries is a party.

|

- Administrative or judicial proceeding arising under any Federal, State, or local provisions regulating the discharge of materials into the environment or for the purpose of protecting the environment if certain materiality thresholds are met

|

MD&A

Item 303 requires disclosure known as the Management’s Discussion and Analysis of Financial Condition and Results of Operations, or MD&A.

|

- No specific MD&A requirements related to climate, but registrants must identify and disclose known trends, events, demands, commitments and uncertainties that are reasonably likely to have a material effect on their financial condition or operating performance

|

Risk factors

Item 105 requires a registrant to provide a discussion of the material factors that make an investment in the registrant or offering speculative or risky.

|

- Does not refer specifically to environmental risks, but requires all risks to be disclosed if significant to the company or the offering

- May require disclosure regarding existing or pending legislation or regulation that relates to climate change

|

Foreign private issuers (FPIs)

While FPIs are not subject to Regulation S-K, Form 20-F includes similar provisions that may require disclosures related to climate change:

- Item 3.D requires the disclosure of material risks.

- Item 4.B.8 requires a description of the material effects of government regulation on the business.

- Item 4.D requires a description of environmental issues that may impact how a company uses its assets.

- Item 5.D requires disclosure of any known trends, uncertainties, demands, commitments, or events reasonably likely to have a material effect on the company’s financial condition and results of operations.

- Item 8.A.7 requires information on any legal or arbitration proceedings that may have or have had significant effects on the company’s financial position or profitability.

If certain information that happens to fall in any of the ESG categories is material to that company, the company needs to disclose it. We expect management and the board to do that, and we will come after them when they don’t.

Commissioner Elad Roisman, Keynote Speech at the Society for Corporate Governance National Conference, July 7, 2020

In its 2010 guidance, the SEC included the following examples of the types of events that may require disclosure under one or more of the Regulation S-K rules. These are only examples and registrants should consider their own circumstances, and consider discussion with SEC counsel, within the context of the SEC’s rules and requirements.

|

Impact of legislation and regulation

- Costs to purchase, or profits from sales of, allowances, or credits under a “cap and trade” system

- Costs required to improve facilities and equipment to reduce emissions in order to comply with regulatory limits or to mitigate the financial consequences of a “cap and trade” regime

- Changes to profit or loss arising from increased or decreased demand for goods and services produced by the registrant arising directly from legislation or regulation, and indirectly from changes in costs of goods sold

|

|

International accords

- The impact of treaties or international accords relating to climate change, if material to the business (e.g., the Kyoto Protocol, the EU emissions trading system)

|

|

Indirect consequences of regulation or business trends

- Decreased demand for goods that produce significant greenhouse gas emissions

- Increased demand for goods that result in lower emissions than competing products

- Increased competition to develop innovative new products

- Increased demand for generation and transmission of energy from alternative energy sources

- Decreased demand for services related to carbon based energy sources, such as drilling services or equipment maintenance services

|

|

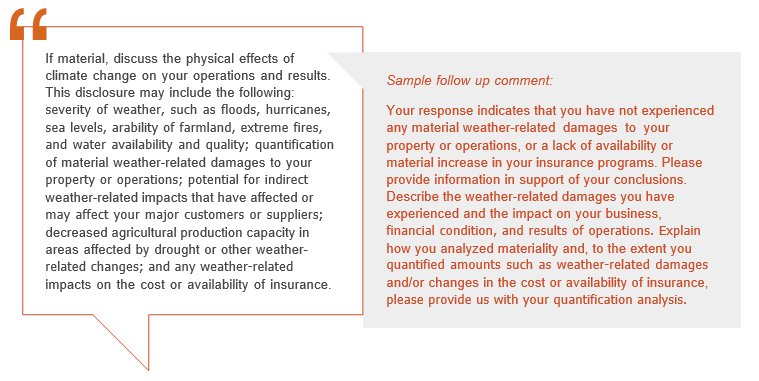

Physical impacts of climate change

- The effects of climate change on the severity of weather (for example, floods or hurricanes), sea levels, the arability of farmland, and water availability and quality, have the potential to affect a registrant’s operations and results.

- Consequences of severe weather include:

- For registrants with operations concentrated on coastlines, property damage and disruptions to operations, including manufacturing operations or the transport of manufactured products

- Indirect financial and operational impacts from disruptions to the operations of major customers or suppliers from severe weather, such as hurricanes or floods

- Increased insurance claims and liabilities for insurance and reinsurance companies

- Decreased agricultural production capacity in areas affected by drought or other weather-related changes

- Increased insurance premiums and deductibles, or a decrease in the availability of coverage, for registrants with plants or operations in areas subject to severe weather

|

| |

In addition, the SEC issued guidance that became effective in February 2020 related to the use of key performance indicators and metrics in MD&A. In that release, the SEC noted that some companies voluntarily disclose environmental metrics. The main intent of the release was to remind companies that when disclosing metrics, further information may be necessary under existing MD&A requirements to make the presentation of the metric not misleading. According to the SEC, adequate context for an investor to understand the disclosed metric would generally be expected to include:

- a clear definition of the metric and how it is calculated;

- a statement indicating the reasons why the metric provides useful information to investors; and

- a statement indicating how management uses the metric in managing or monitoring the performance of the business.

Disclosure of the estimates or assumptions underlying the metric or its calculation may also be necessary context for the metric.

|

In September 2021, the SEC’s Division of Corporation Finance reiterated the importance of the 2010 interpretive guidance and published some examples of staff comments the Division may issue to companies regarding climate-related disclosures. Since that time, the Division has issued comment letters to both domestic and foreign SEC registrants across a wide range of industries specifically focused on climate-related disclosures. As of March 22, 2022, the comment letters for 28 registrants have been made public. Based on our review, each registrant received an average of six initial questions, each of which mirrored the examples published in September 2021. Broadly, the letters asked about topics such as (1) inconsistencies between a registrant’s corporate social responsibility report and its SEC filings and (2) the lack of disclosure in a registrant’s SEC filing of the risks, trends, and impact of climate change for the registrant and its business.

In general, registrants responded to the initial questions by indicating that the matters were quantitatively and qualitatively immaterial such that further disclosure was not warranted. Follow up comment letters were issued to all 28 registrants; these letters most commonly requested that the registrant support its assessment of materiality, referring in several instances to initial responses as “conclusory,” indicating that the registrant did not “adequately address the specific items” from the prior comment.

Letters exchanged with 2 of the 28 registrants required 3 rounds of responses, while the letters for the remaining registrants were resolved after the second round. Of the approximately 160 comments issued, only a few ultimately required the registrant to expand its disclosures.

Examples of common staff comments and follow up comments in the letters made public to date follow.

Final thoughts

When the SEC’s guidance was issued in 2010, the stated purpose was to “remind companies of their obligations under existing federal securities laws and regulations to consider climate change and its consequences as they prepare disclosure documents to be filed with [the SEC] and provided to investors.” In our current culture of enhanced environmental focus and demands from both regulators and legislators for increased transparency, and in the face of the recent comment letters, companies would be well served to evaluate their impact on the climate and the climate’s impact on them, and to make transparent disclosures now based on that evaluation. And it shouldn’t be just about risk; if climate change, or the reaction to climate change results in business opportunities, those should be disclosed, too.

The SEC’s proposed disclosures call for a phased transition beginning with fiscal year 2023 (filings in 2024) with some registrants not required to apply the new disclosures until 2026 filings. Until then, we continue to believe that in light of a heightened focus from a variety of stakeholders, what a company does not say can be as influential as what it does say. There is much that investors and other stakeholders want to know, and much that current SEC rules already require.

To have a deeper discussion, contact:

|