Non-GAAP measures continue to be a focus area for the SEC staff, as they consistently top the list of comment letter topics and have recently been at the center of SEC enforcement actions. This In depth summarizes the focus of the SEC staff comments through September 30, 2023 and provides additional insights on non-GAAP measures. It also provides a summary of recent SEC staff updates to its interpretative guidance on non-GAAP measures and comment letter trends in 2023 specific to these updates. Finally, it includes recommendations for companies’ presentation of non-GAAP measures consistent with the guidance.

What is a non-GAAP measure?

Non-GAAP measures are commonly used by companies as supplements to their financial statements to deepen investors’ understanding of their performance or financial condition. Companies also use them to show management’s view of core operations, typically by eliminating charges or gains and other amounts they believe are not indicative of ongoing operational performance, such as major strategic restructurings, impairments, or gains (losses) on debt extinguishment.

A measure becomes a non-GAAP measure and is subject to the SEC’s non-GAAP rules and interpretive guidance when it excludes amounts that are included in (or includes amounts that are excluded from) the most directly comparable GAAP measure. Operating or other statistical measures (for example, unit sales, number of employees, and number of subscribers), certain ratios, and financial information that does not provide numerical measures that are different from the comparable GAAP measures are not subject to the non-GAAP guidance.

Some common non-GAAP measures are:

EBIT - earnings before interest and taxes

EBITDA - earnings before interest, taxes, depreciation, and amortization

Adjusted gross margin or adjusted contribution margin – revenue less certain expenses (e.g., expenses included in cost of sales)

Adjusted earnings or adjusted EBITDA - removes various additional items (e.g., stock-based compensation, restructuring charges, and other unusual charges) from earnings or EBITDA

Adjusted earnings per share – a non-GAAP performance measure (e.g., adjusted earnings) on a per share basis

Free cash flow - typically calculated as cash flows from operating activities less capital expenditures

The applicable guidance for a non-GAAP measure depends on where it is disclosed, whether in an SEC filing (such as a Form 10-K or Form 10-Q), earnings release, or other public disclosure. Companies that plan to disclose non-GAAP measures should be familiar with the SEC’s rules and interpretations in Regulation G, Regulation S-K Item 10(e) and the SEC staff Compliance and Disclosure Interpretations (C&DIs) on non-GAAP measures.

Summary of non-GAAP rules

SEC filings (e.g., Form 10-K, Form 10-Q)

Earnings release

Any public disclosure (e.g., company website, analyst presentation)

Applicable rule

Reg S-K, Item 10(e)

Reg S-K, Item 10(e)(1)(i)

Reg G

1.

The non-GAAP measure taken together with the accompanying information cannot be misleading

✓

✓

✓

2.

The most directly comparable GAAP measure must be disclosed

✓

✓

✓

3.

A reconciliation of the non-GAAP measure to the most directly comparable GAAP measure must be included

✓

✓

✓

4.

The GAAP measure must be presented with equal or greater prominence than the non-GAAP measure

✓

✓

5.

Management must disclose why it believes the non-GAAP measure is useful to investors

✓

✓

6.

If material, management must disclose the additional purposes, if any, for which it uses the non-GAAP measure

✓

✓

7.

Charges or liabilities that require cash settlement cannot be excluded from any measure of liquidity

✓

8.

A measure cannot be labeled as nonrecurring or infrequent (or any similar title) if it excludes amounts resulting from an event that has occurred in the last two years or is expected to occur again in the next two years

✓

9.

Non-GAAP measures cannot be presented on the face of the financial statements or in the notes

✓

10.

Non-GAAP measures cannot be presented on the face of any pro forma financial information

✓

11.

Non-GAAP measures must not use titles or descriptions that are the same as, or confusingly similar to, GAAP titles

✓

Why are non-GAAP measures relevant?

Most S&P 500 companies currently use non-GAAP measures and key performance indicators to provide stakeholders such as investors, analysts, and bankers with additional tools to evaluate performance and financial condition, which ultimately are factored into the valuation of companies.

The SEC’s requirements for non-GAAP financial measures were created in 2003 in response to statutory requirements in the Sarbanes-Oxley Act of 2002 (SOX). The SOX requirements, and the subsequent SEC rules implementing those requirements, focused on two key principles relating to the presentation of non-GAAP information:

Requirements that information “does not contain an untrue statement of a material fact or omit to state a material fact necessary in order to make the pro forma financial information, in light of the circumstances under which it is presented, not misleading,” and

Reconciliation of the non-GAAP information to the financial statements.

Since those original rules were issued, the SEC staff has periodically issued updates to its interpretive guidance that continue to focus on avoiding misleading non-GAAP financial measures. In December 2022, the SEC staff announced updates to its C&DIs relating to non-GAAP financial measures. During the 2022 AICPA & CIMA Conference on Current SEC and PCAOB Developments and as part of the announcement, the staff noted that the updates were intended to memorialize existing staff views provided through public statements or comment letters. The following table highlights the main changes.

C&DI update

Description of update

100.01 (updated)

These updates clarify existing interpretive guidance stating a non-GAAP measure may be considered misleading if it excludes cash operating expenses that are “normal” and “recurring” in the operation of the business.

The staff provided additional context on what is “normal” and “recurring” by stating that:

The nature and effect of a non-GAAP adjustment is assessed within the context of a company’s operations, revenue generating activities, business strategy, industry, and regulatory environment; and

An operating expense that occurs repeatedly or occasionally, including at irregular intervals, could still be viewed as recurring.

100.04 (updated)

These updates clarify existing interpretive guidance for non-GAAP adjustments that change GAAP recognition and measurement principles (individually tailored accounting principles) and specifies that such adjustments may cause the presentation of the non-GAAP measure to be misleading.

The updates also included examples of such adjustments that the staff may consider misleading.

100.05 (new)

These updates memorialize the staff’s views that (1) non-GAAP measures and any adjustments should be appropriately labeled and clearly described as non-GAAP within the disclosures and (2) the relevant measure should not have a title that is confusingly similar to a GAAP measure.

100.06 (new)

These updates provide the SEC staff’s view that a non-GAAP measure could mislead investors to such a degree that even extensive, detailed disclosure about the nature and effect of each adjustment would not prevent the non-GAAP measure from being materially misleading.

102.10 (updated)

These updates expanded the previous C&DI to include three subsections that provide guidance and examples of non-GAAP measures that are considered more prominent than the corresponding GAAP measures.

This includes the presentation of a non-GAAP income statement, which the staff has clarified is an income statement that is comprised of non-GAAP measures and all or most of the line items and subtotals in a GAAP income statement.

What is the SEC’s focus on non-GAAP?

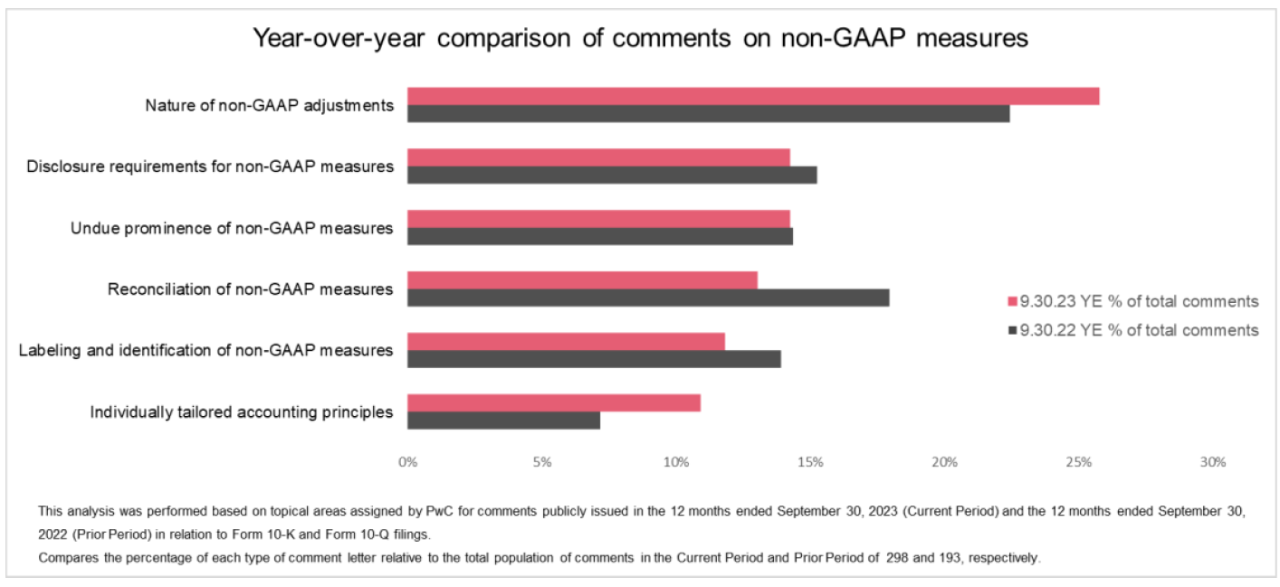

A search of publicly available Division of Corporation Finance staff comments illustrates a continued focus on company disclosure of non-GAAP financial measures; this topic has consistently trended as one of the top comment letter topics over the past five years and the top comment letter topic of 2023 so far.

We conducted an analysis

of staff comments from its reviews of Forms 10-K and 10-Q during the twelve months ended September 30, 2023 (2023 period) compared to the twelve months ended September 30, 2022 (2022 period) and noted that the absolute total number of comments issued has increased, although the percentage of comments pertaining to non-GAAP measures relative to all comments remained relatively stable.

During the 2023 period, the SEC issued 1,346 comment letters as compared to 863 comment letters in the 2022 period and approximately 30% of comment letters during each of those periods contained at least one comment related to non-GAAP measures.

The most common issues raised on non-GAAP measures during those periods were as follows:

The percentage of comments questioning the nature of non-GAAP adjustments slightly increased in the 2023 period compared with the 2022 period, from comprising 22% of comments for the 2022 period to 26% of comments for the 2023 period; it remains the most common type of comment. Among the other issues raised in comments, individually tailored accounting principles also increased (slightly from 8% for the 2022 period to 12% of all non-GAAP comments for the 2023 period), and the relative percentage of all other categories of non-GAAP comments went down year over year. The most significant drops pertained to comments on the reconciliation of non-GAAP measures and the labeling and identification of non-GAAP measures.

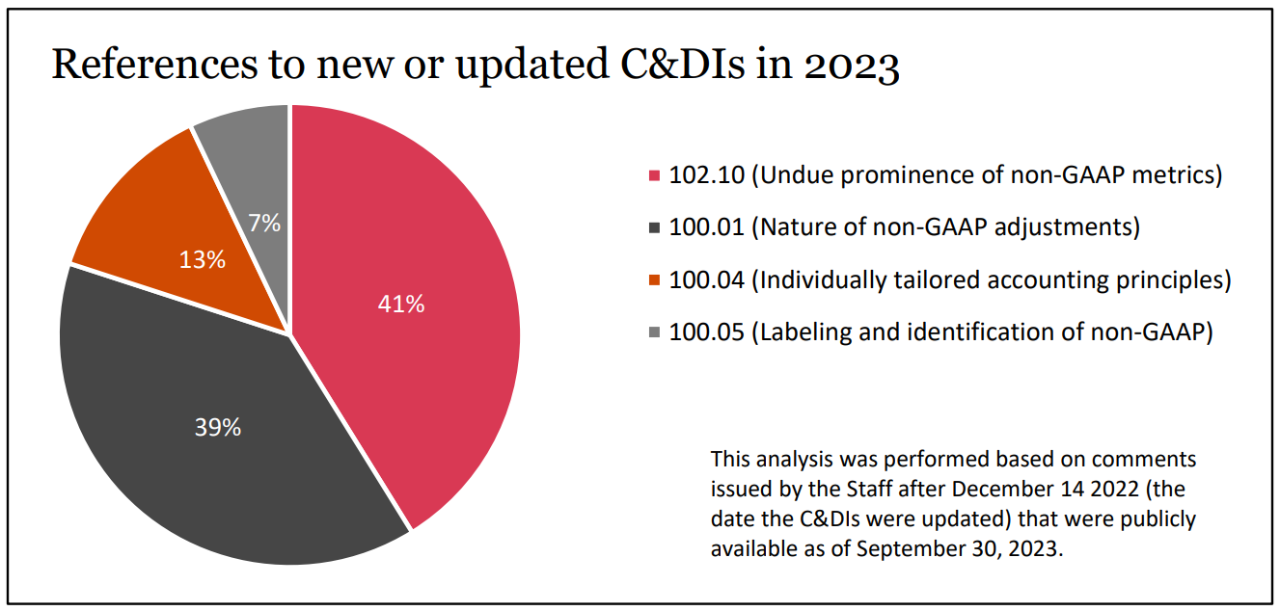

In addition, since the staff’s 2022 updates to C&DIs, it has issued approximately 150 comments related to non-GAAP measures, with almost half of those comments referencing the updated C&DIs. Of the comments that referenced the updated C&DIs, the following provides a breakdown of the C&DIs referenced.

In addition to SEC staff focus on non-GAAP through comment letters, the SEC’s Division of Enforcement has also focused on these measures. In early 2023, the SEC charged a registrant with making misleading disclosures about its non-GAAP financial performance measures over a multi-year period in its earnings releases and annual and quarterly reports. The SEC stated that the registrant’s disclosure controls and procedures (DC&P) were not adequate to ensure that the non-GAAP measures disclosed by the company were not misleading. A public company’s DC&P are required controls to ensure information disclosed by the registrant is recorded, processed, summarized, and reported in a timely manner. Because the presentation of non-GAAP measures is accompanied by specific preparation and disclosure requirements, non-GAAP measures fall within DC&P. Although no company individuals were specifically charged in the case, the registrant consented to a cease-and-desist order; agreed to address gaps in its DC&P, including creation and implementation of appropriate non-GAAP policies; and paid a seven-figure penalty.

What are some examples of SEC comments?

Presented below is a description of the most common types of SEC staff comments and example comments for each category:

Nature of non-GAAP adjustments

Disclosure requirements for non-GAAP measures

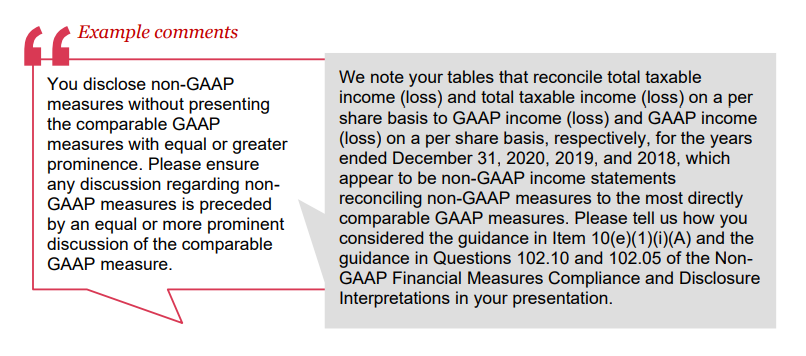

Undue prominence of non-GAAP measures

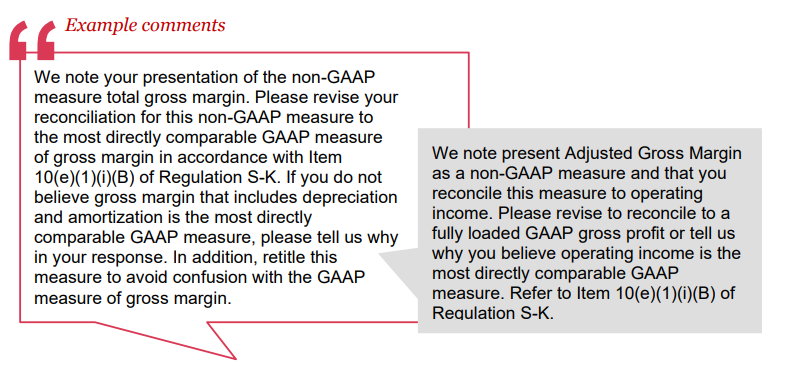

Reconciliation of non-GAAP measures to the most directly comparable GAAP measure

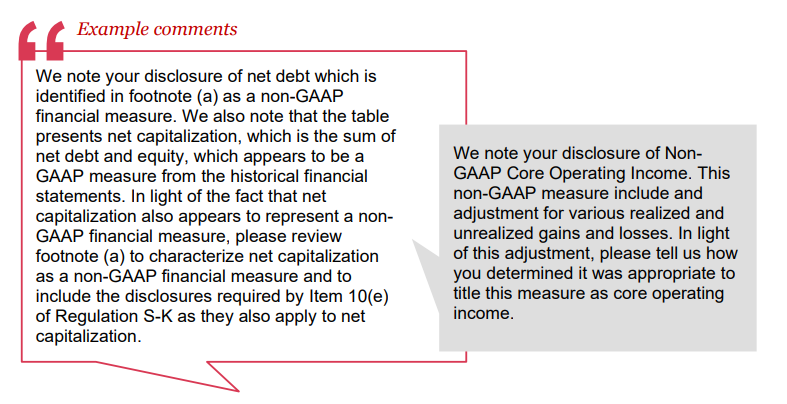

Labeling and identification of non-GAAP measures

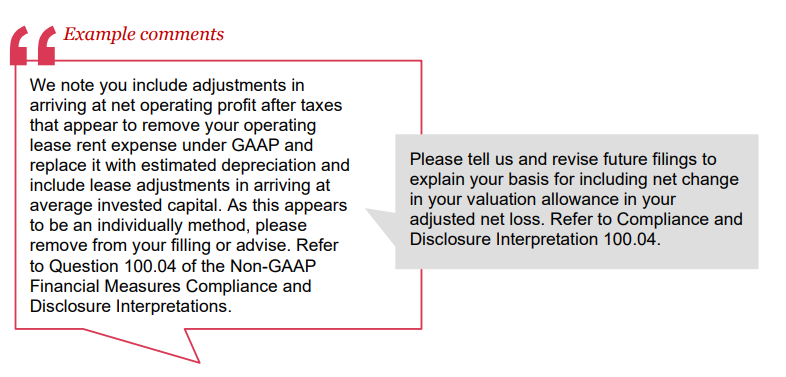

Individually tailored accounting principles

We also provide a general summary of responses to each category of comments in the 2023 period.

1. Nature of non-GAAP adjustments

These comments generally include questions about the appropriateness of specific adjustments made to a GAAP measure to arrive at the non-GAAP financial measure, including whether the adjustment may violate a provision of the non-GAAP rules or may conflict with specific staff interpretive guidance. Comments may also seek to better understand the nature of specific adjustments, particularly when it is not otherwise apparent by the label or other disclosures. Recently, comments in this area have focused on adjustments that remove or exclude cash operating expenses that are normal and recurring in the operation of the business.

Because non-GAAP adjustments are specific to the facts and circumstances of a company, there is diversity in how these comments were resolved. Companies generally explained why the adjustment(s) being questioned did not violate the provisions of the non-GAAP rules and interpretive guidance, including why they believed the adjustments were not misleading. With respect to questions regarding adjustments for items that may be considered normal, recurring, cash operating expenses, responses focused on why the registrant did not believe the items were “normal” or “recurring” operating expenses. Otherwise, companies generally agreed to either enhance their disclosure in future filings to comply with the staff’s comment or, in some cases, remove the non-GAAP adjustment in future filings.

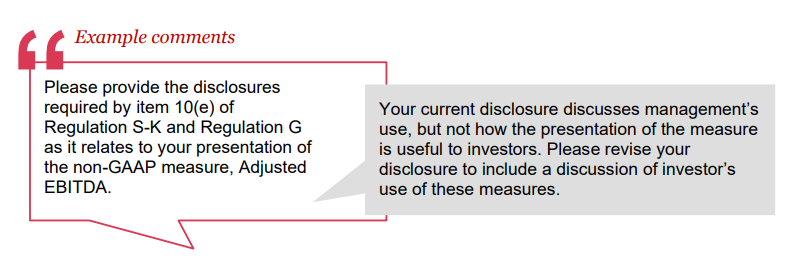

2. Disclosure requirements for non-GAAP measures

The SEC staff will often raise questions regarding the lack of required disclosures associated with non-GAAP financial measures, as required by Item 10(e) of Regulation S-K, including why the company believes the presentation of the non-GAAP financial measure provides useful information to investors regarding the company's financial condition and results of operations.

In response to these comments, companies generally included enhanced disclosures required by Item 10(e) of Regulation S-K or to enhance certain parts of existing disclosure of non-GAAP measures. At times, companies decided to remove disclosure of the non-GAAP measure from their future filings.

3. Undue prominence of non-GAAP measures

These comments pertain to non-GAAP financial measures that are presented with greater prominence than the most directly comparable GAAP measure, including (1) beginning the non-GAAP reconciliation with the non-GAAP measure or (2) not providing an equally expansive discussion and analysis of the most comparable GAAP measure when such a discussion and analysis is provided for the non-GAAP measure. This category can also include staff comments on a company’s presentation of a non-GAAP income statement. Finally, comments in this category can reference the overall quantity of non-GAAP measures presented.

Companies generally agreed to revise disclosures in future filings to ensure the directly comparable GAAP measure was presented with greater prominence than the related non-GAAP measure, including through removing certain measures or altering the presentation format to avoid the appearance of a non-GAAP income statement.

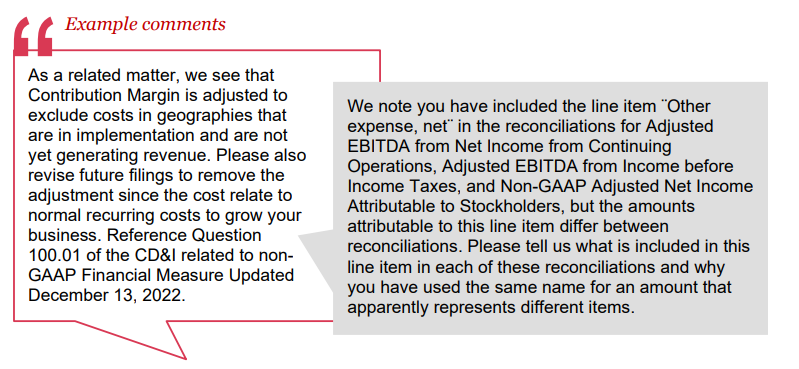

4. Reconciliation of non-GAAP measures to the most directly comparable GAAP measure

These comments commonly question whether the GAAP measure in the reconciliation is the most directly comparable GAAP measure. They may also include questions regarding the lack of a reconciliation of a non-GAAP measure to its most directly comparable GAAP measure.

In response to these comments, companies generally agreed to revise disclosures in future filings to include the directly comparable GAAP measure and/or the reconciliation to the directly comparable GAAP measure called for by Item 10(e) of Regulation S-K, or they otherwise were able to explain why they believed the GAAP measure in the reconciliation was the most directly comparable GAAP measure. At times, companies removed the non-GAAP measure from the disclosure altogether from its future filings, which commonly occurred when either gross margin or gross profit was the most directly comparable GAAP measure and the company did not present either of these measures in its financial statements.

5. Labeling and identification of non-GAAP measures

These comments generally pertain to a company not clearly identifying a measure as a non-GAAP measure and, as a result, excluding the disclosures required by Item 10(e) of Regulation S-K. Generally, these comments related to situations when the label used for a measure or the disclosure of the adjustments that comprised a measure could cause a reader to confuse the measure with a GAAP measure with the same or similar label.

In response to these comments, companies generally agreed to comply with the staff’s recommendations to revise the label of the measure, to include additional disclosure to comply with the non-GAAP guidance, or to remove the non-GAAP measure in its entirety from its future filings.

6. Individually tailored accounting principles

These comments relate to the appropriateness of non-GAAP adjustments that change the recognition and measurement principles used to calculate the measure to be inconsistent with GAAP, which the SEC staff has indicated it believes could be misleading. For example, C&DI Question 100.04 notes that adjustments that alter the recognition pattern of revenue (e.g., accelerating revenue recognition) or that change the basis of accounting from accrual to cash basis may be considered misleading.

Although some companies articulated to the staff why the non-GAAP measure was not an individually tailored accounting principle or agreed to clarify their disclosures going forward to make that point more evident, companies generally agreed to amend their non-GAAP measure disclosure or decided to remove the non-GAAP measure in its entirety from its future filings.

What can companies do to be better prepared?

The staff comments are based on both the published rules and interpretive guidance on non-GAAP measures. The best way to reduce the risk of comments on its non-GAAP measures is for a company to be thoughtful about the non-GAAP measures and adjustments it presents and to be knowledgeable of the rules and guidance. This includes ensuring non-GAAP measures are clearly labeled and appropriately reconciled to the most directly comparable GAAP measure. In addition, companies should ensure it has included appropriate disclosure to inform the reader as to the nature of adjustments made in a non-GAAP measure and why these measures may be useful to investors. Companies should also consider consulting with legal counsel regarding the published rules and interpretive guidance on non-GAAP measures.

In addition, a company should have robust policies and procedures to prepare and review non-GAAP adjustments, which includes oversight over the completeness and accuracy of the information that is used as the basis for any adjustment. Since adjustments should be evaluated within the context of the company’s operations (revenue generating activities, strategy, industry, and regulatory environment), which change over time, companies should also have processes in place to monitor such changes and any needed updates to the non-GAAP measures as a result.

The following table includes some common comments on non-GAAP measures, the related rule or interpretative guidance on which the comment is generally based, and recommendations for how companies can appropriately apply the respective non-GAAP rule.

Observation

Guidance

Recommendation

Presentation of non-GAAP measures with greater or undue prominence than the most directly comparable GAAP measure

Item 10(e)(1)(i)(A) of Regulation S-K

C&DI 102.10(b)

Ensure that disclosures, including reconciliations, begin with the most directly comparable GAAP measure.

Evaluate the overall number of non-GAAP measures presented and the format of the presentation and consider whether the quantity or presentation format could place undue prominence on the non-GAAP information.

Reconciliation of a non-GAAP measure to its directly comparable GAAP measure

Item 10(e)(1)(i)(B) of Regulation S-K

C&DI 102.10(b)

Be thoughtful as to what is considered the directly comparable GAAP measure, including considering the reasons why management believes the measure may be useful to investors. For instance, non-GAAP measures that are margin-based may need to be reconciled to GAAP gross margin or GAAP gross profit – even if the company does not present gross margin or gross profit in its financial statements.

If the non-GAAP measure is a liquidity measure, the SEC would generally expect this measure to be reconciled to GAAP cash flows from operations.

Types of adjustments that companies make to the directly comparable GAAP measure to arrive at their respective non-GAAP measure

C&DI 100.01 C&DI 100.02 C&DI 100.03 C&DI 102.03

Be aware that reflecting any of the following items within a non-GAAP measure could invite scrutiny from the SEC staff:

Exclusion of items that are recurring in nature (including those that occur repeatedly or occasionally, including at irregular intervals);

Elimination of cash items considered core to operating a company’s business;

Exclusion of charges but not similar gains; or

Inconsistent presentation of a non-GAAP measure and/or the adjustment(s) that comprise that non-GAAP measure

Take a holistic view and evaluate and document what is and is not a normal, recurring, cash operating expense within the context of the company’s historical operations and what is expected in the near future. In fact, we find that a best practice is to have a formal written policy that clearly lays out these criteria.

This analysis should consider what is normal within the context of its operations, revenue generating activities, strategy, industry, and regulatory environment, which can change over time. As is noted in C&DI 100.01, even an operating expense that occurs occasionally, including at irregular intervals, may be considered recurring. For example, costs associated with opening a new store location in the retail industry could be considered “normal and recurring” given that opening and closing stores are part of a company’s business strategy and revenue-generating activities.

Companies should also not be too narrow in defining what is considered recurring in nature. Generally, only those costs that are incremental in nature would fit within the definition of non-recurring. If the costs represent expenses that the company would have incurred regardless, the Staff may view the costs as recurring and, as a result, costs that should not be excluded in the respective company’s non-GAAP measure.

Questions concerning the nature of an adjustment and/or what an adjustment is comprised of

Aim to be clear — whether in the caption of the adjustment or separately as a part of an accompanying disclosure —as to the nature of an adjustment, including the key components, so that a reader can understand everything that is included in an adjustment and why the adjustment is being made.

COVID Non-GAAP guidance is not just for COVID

In March 2020, the SEC staff issued disclosure guidance related to COVID-19, including how non-GAAP measures could be impacted by the pandemic and what companies should consider in their non-GAAP disclosures. One topic discussed was when a non-GAAP measure is reconciled back to a comparable GAAP measure that is still provisional in nature because the measure may be impacted by adjustments that may require additional information and analysis. The SEC staff has recently stated that this guidance is not specific to COVID-19 and should be applied to other situations that could impact a company’s nonGAAP measures as well. Companies should continue to consider this guidance.

When to adjust non-GAAP measures

At the time of the 2022 C&DI update, the SEC staff noted that when it objects to a non-GAAP measure because it believes it is misleading, it expects that the measure will be removed in the next filing or public disclosure, with prior periods recast to remove the measure as well. However, before the SEC staff objects to a non-GAAP measure, it will issue a comment letter seeking to understand the company’s analysis. As a result, companies should strive to be thorough and thoughtful in their responses throughout the process until the matter is finalized (which could occur after only one round of comment and response). In addition, companies should consider reaching out to the member(s) of the SEC staff reviewing the filing and/or the non-GAAP expert(s) in the Division of Corporation Finance to receive any needed clarification on the questions being asked and ultimate resolution of the matters being discussed.

Final thoughts

Non-GAAP measures have become a common part of financial reporting and various stakeholders, including preparers, investors, analysts, and the SEC staff, are focused on these measures. We anticipate the upward trend of SEC staff comments on non-GAAP measures to continue for the foreseeable future, which may include an increased focus on specific types of adjustments, including adjustments for tax impacts, restructuring charges, and litigation charges.

These recent trends are likely understated as well. Because the SEC staff is only required to review each company’s public filings once every three years, there are likely many companies whose non-GAAP measures have not been reviewed in a few years. Even if a company’s non-GAAP measures have been reviewed previously, we have observed instances of the SEC staff objecting to them — even when they had not previously objected in the past.

As a result, it is important that companies be knowledgeable about the guidance that governs non-GAAP measures and thoughtful in its application to prevent being unprepared when outside parties, including the SEC staff, have questions. Companies should also focus on their governance processes, including the disclosure controls and procedures underpinning the preparation and disclosure of their non-GAAP measures.

For more PwC accounting and reporting content, visit us at viewpoint.pwc.com. On the go? Take our PwC accounting podcast series with you at the Viewpoint podcasts page or wherever you listen to your podcasts.

1 The analysis of SEC comment letters includes those comments that are publicly available as of September 30, 2023 relating to Forms 10-K and 10-Q. The SEC releases comments publicly approximately 20 days after the completion of its review and, as a result, there may be additional comment letters released subsequently that relate to the periods discussed.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Add to favorites

Preparing TOC

Link copied

Add to favorites

Please ensure

that you select Print Background (colors and images)

when printing.