The emergence and growth of ‘virtual’ businesses provided conspicuous evidence that, in the digital age, value accrues to ideas, R&D, brands, content, data and human capital—i.e. intangible assets—rather than industrial machinery, factories or other physical assets.”

- Carlyle Group, Global Insights, When the Future Arrives Early, September 2020

Business models in many industries have evolved in the last decade to increasingly create economic value from investments in intangible assets, such as brands, technology, and customer relationships. And this intangible-centric approach has been more obvious since the start of the global pandemic. Companies have made and continue to make substantial investments that create or enhance the value of intangibles, which are inextricably linked to their strategy. They may, for example:

- research new technologies,

- cultivate customer relationships that form the basis for future revenue streams,

- foster relationships with partners and service providers that complement in-house capabilities,

- run advertising and promotions that enhance product recognition and brand affinity,

- identify, hire, and nurture a workforce that can efficiently and effectively deliver on the company’s value proposition, or

- develop strong processes, know-how, and trade-secrets that create efficiencies and value.

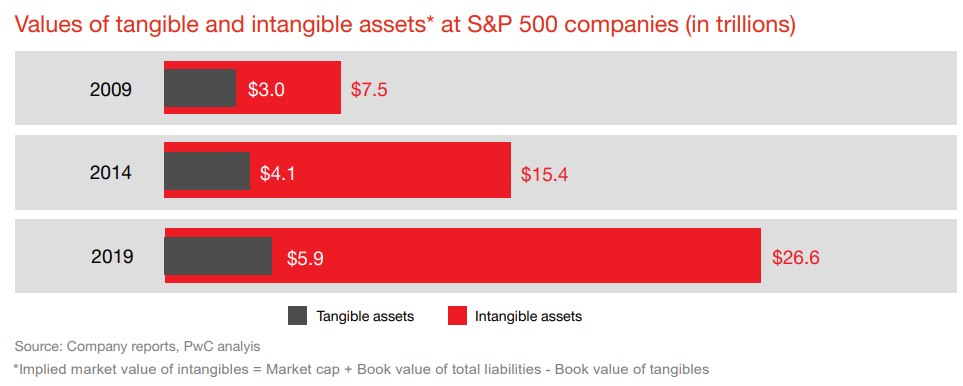

Since 2009, the implied market value of intangible assets at S&P 500 companies increased 255%, while the book value of tangible assets only increased 97% over the same period.

While this value creation has happened, the accounting model has remained unchanged. Current accounting guidance does not always recognize the value created by intangibles, either on the balance sheet or in the footnotes. Although hard assets, such as property and equipment, appear on company balance sheets, investments in internally-generated intangibles are generally expensed as incurred. As a result, a company’s most valuable assets often do not appear on its balance sheet. The result can be a large gap between the book value of the company and its market capitalization.

To enhance the relevance of financial reporting, we believe it will need to reflect the transition to a knowledge-based economy and provide greater insight into intangible investments. Communicating this information as part of the financial reporting process, rather than through other avenues, subjects it to the rigorous processes and controls in the financial reporting ecosystem that are designed to produce information that is reliable, consistent from year to year, and comparable between companies. This is especially important as investors are increasingly focused on a company’s environmental, social, and governance (ESG) strategy, which highlights management’s stewardship of certain intangibles, such as human capital.

The question is how financial statements can most effectively and efficiently communicate information about intangible assets to stakeholders. Given the wide array of intangibles, there may not be a one-size-fits-all approach. Instead, stakeholders may need to work together to develop a mixed model of recognition and disclosure to communicate the relevant decision-useful information.

The value of intangibles

The increasing proportion of company value represented by intangible assets reflects not only greater investment, but also some attributes of these assets that may make a company worth more than its book value. Many intangible assets, such as certain technologies, are infinitely-scalable, meaning they can be deployed in additional situations for no or little additional cost; as a result, their economies of scale often dwarf those that can be achieved through tangible assets. In addition, some intangibles, such as patents, are unique and protected by legal or other barriers to competition, thereby enhancing their value.

Despite the extraordinary value of intangibles, financial statements are generally not designed to directly capture and communicate information related to them unless they arise in connection with the acquisition of a business. In fact, the financial reporting ecosystem as a whole devotes minimal attention to assets that are not recognized on the balance sheet, such as internally-generated intangibles.

Inconsistencies in accounting models for investments

Today’s financial reporting model evolved over time, resulting in inconsistent models for different types of investments even though management applies a similar capital allocation process to all significant investments.

The result: GAAP earnings metrics reflect the return on other investments, but not internally-generated intangible assets. As a result of the non-recognition of internally-generated intangibles, the company value created by investing in intangible assets is only observable to stakeholders in an indirect, lagging way (for example, through growing revenues or expanding margins). Similarly, there is only indirect information about management’s stewardship of those assets. Decoupling an expenditure from the associated economic benefit—as we do for internally-generated intangibles—may drive users to other data sources to assess value creation and preservation, calling into question the relevance of the financial statements.

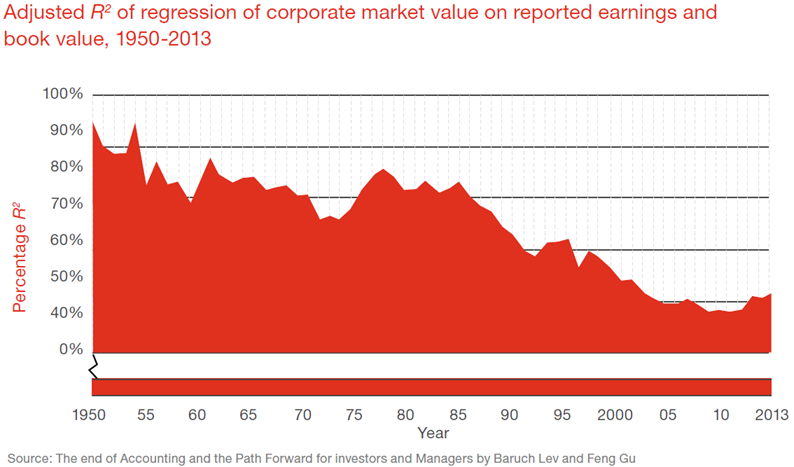

Investors are already beginning to get their information elsewhere. The End of Accounting and the Path Forward for Investors and Managers reports a significant decrease in correlation between GAAP earnings and book value with market capitalization between 1950 and 2013. The authors believe the lack of information on internally-generated intangibles is one reason for this decrease. The increasing business focus on intangibles may exacerbate the potential disconnect between financial reporting and investing in the future.

A path forward

As financial reporting continues to mature, the accounting hallmark of relevance must be a key component of the financial reporting framework. We believe information about intangibles is becoming increasingly important to maintaining the relevance of financial reporting in the new economy, where intangibles represent such a large portion of many companies’ value and often reflect some of their most significant investment decisions.

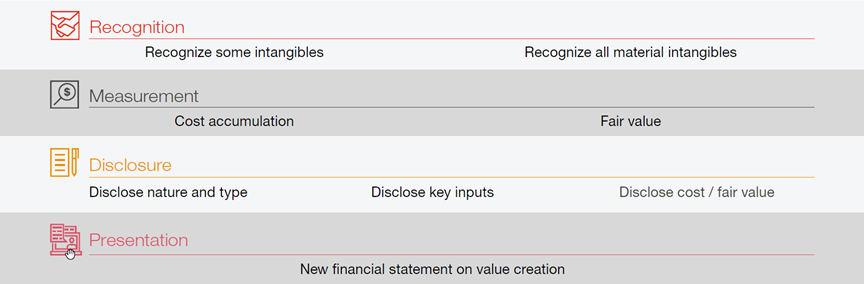

Given the complexity and evolving nature of intangibles and diversity in how companies manage intangibles and investors evaluate them, there may not be a one-size-fits-all approach. There is a wide range of alternatives to providing decision-useful information to investors, which could include recognition of all or some material intangibles, whether at cost or fair value, disclosure of key intangibles in addition to or instead of recognition, or even a new financial statement that provides measure of value creation. Each of these alternatives has different information needs and benefits; some information is already captured.

Companies already track the cost and return information, such as intellectual property (IP), using a cost accumulation approach. Also, they closely track IP for legal, tax, and other purposes such as ESG reporting, and often explicitly consider their return on investment when deciding which IP projects to fund. In addition, companies in some industries already supply information on key drivers of the value of assets such as customer relationships. For example, companies with a subscription-based business model will often disclose customer attrition data. Another source of disclosure information for certain intangibles, such as workforce assets, is information increasingly contemplated as part of ESG disclosures.

Stakeholder engagement and evolution of the accounting and disclosure model

The largest standard setters are recognizing the need for action in this area. The FASB has a research project on its agenda on the accounting for and disclosure of intangibles, and the IASB agenda consultation this spring will seek stakeholder feedback on such a project. Both projects are in their early days and are clean slates, which provide both boards opportunities to make some of the biggest impacts on the relevance of financial reporting in decades.

Considering its relevance, EFRAG invites the IASB to start working on [intangibles].

In considering the accounting for intangible assets, EFRAG considers it necessary that the IASB takes into account the concerns of investors who want to compare companies that grow by acquisitions more easily with those that grow organically and, as such, starts a project on IAS 38 Intangible Assets.

- European Financial Reporting Advisory Group, 28 January 2021

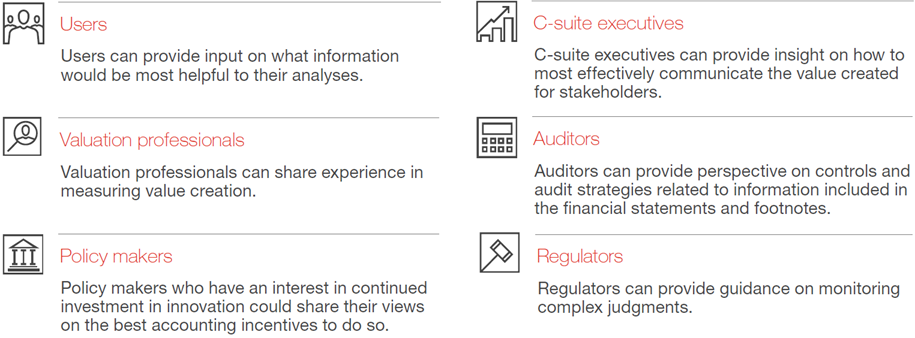

When considering alternatives, it will be critical for standard setters to engage all types of stakeholders to gather each of their unique perspectives.

Conclusion

Transformational changes to the financial statements, such as recording and/or disclosing all or some internally-generated intangible assets, pursued with a high degree of business community engagement, will help the financial reporting process to keep pace with business innovation and remain relevant.

Maintaining relevance is a continuous process. The nature of the information captured in the financial statements needs to continue to evolve, and the best approach to communicating information on value creation may change over time. We should not wait to begin the conversation on how to communicate this important information to stakeholders.

To have a deeper discussion, reach out to us: