2420.1

Overview (Last updated: 3/31/2009)

NOTE to SECTION 2420.1

With the exception of Section 2410.1, the guidance in Section 2410 also applies to calculating S-X 4-08(g) significance. Section 2410 includes important clarifying points, which may not be reproduced below, related to measuring S-X 4-08(g) significance. Therefore, you should refer to Section 2410 (except Section 2410.1) as well as Section 2420 when seeking guidance on calculating S-X 4-08(g) significance. Section 2410.1 does not apply to S-X 4-08(g) significance because the number of significance tests and the significance thresholds used under S-X 4-08(g) can differ from the number of significance tests and the significance thresholds used under S-X 3-09. See further discussion in the chart below and Note 3 to Section 2420.3. (Last updated: 6/30/2010) |

The requirements to present summarized financial data of the registrant's equity method investees in a footnote to the registrant's financial statements apply to all registrants. The significance tests and thresholds used to determine whether such disclosure is required as well as the level of disclosure may differ depending on whether:

- The registrant is a smaller reporting company and

- The registrant's financial statements are for an annual or interim period.

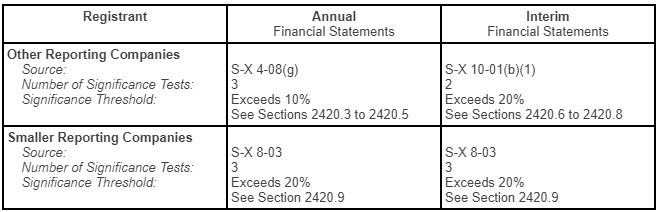

The following table includes an overview of the sources of these requirements as well as the number of significance tests that must be computed and the significance thresholds. See the Sections noted in the chart for further detail.

2420.2

Definitions — The summarized financial data requirements apply to "Subsidiaries Not Consolidated" and "50% or Less-owned Persons." See Sections 2405.2 and 2405.3 for definitions of these terms.

2420.3

Other Reporting Companies - Annual Financial Statements - Overview [S-X 4-08(g)] (Last updated: 3/31/2013)Determine significance of each investee for each of the registrant's fiscal years required to be presented in the filing using all 3 tests in S-X 1-02(w) (investment, asset and income tests). Present summarized financial data described in Section 2420.4 in the registrant's financial statement footnotes for all investees (not just the investee that is significant) if significance of any individual or any combination of investee(s) exceeds 10%. See exception below at Section 2420.5 Interaction of S-X 4-08(g) with S-X 3-09.

NOTES to SECTION 2420.3

- De Minimis Exception - Annual Financial Statements - SAB Topic 6K.4.b. notes that the staff recognizes that exclusion of summarized information for certain, but not all, investees may be appropriate in some circumstances where it is impracticable to accumulate and the summarized information to be excluded is de minimis.

- Significance — Number of Tests - The requirement to determine significance for purposes of S-X 4-08(g) using all 3 tests in S-X 1-02(w) differs from S-X 3-09, which only requires significance to be determined based on 2 tests (investment and income tests). In 1994, S-X 3-09 was revised to delete the asset test; however the asset test was retained for S-X 4-08(g) to ensure a minimum level of financial information about an investee when the investment test significance was small, but the registrant's proportionate interest in the investee's assets was material, as might be the case for a highly leveraged investee.

- Significance — Number of Periods - Significance should be measured for each fiscal year presented. The staff believes that the purpose of the S-X 4- 08(g) reference to S-X 1-02(w) is to describe the mechanics of the significance tests, not to limit application of the tests to the most recently completed fiscal year. (Last updated: 6/30/2010)

|

2420.4

Other Reporting Companies - Annual Financial Statements — Minimum Disclosure [S-X 4-08(g) references S-X 1-02(bb)]

(Last updated: 6/30/2010)If S-X 4-08(g) significance is met in any fiscal year presented, the registrant's financial statement footnotes for each of the registrant's fiscal years presented should include, at a minimum, the following summarized financial data for all investees (not just the investees that are significant): current and noncurrent assets and liabilities; redeemable stock and noncontrolling interests; revenues; gross profit; income from continuing operations; and net income. The summarized annual financial data for each investee may be aggregated, but it should not be labeled "unaudited."

2420.5

Other Reporting Companies - Annual Financial Statements — Interaction of S-X 4-08(g) with S-X 3-09SAB Topic 6K.4.b. notes that if a registrant includes separate financial statements (i.e.,

S-X 3-09 financial statements) for an investee in its annual report, then it need not include the summarized financial information required by

S-X 4-08(g) for that investee. [

S-X 4-08(g) and

SAB Topic 6K.4.b.]. The reason for this conclusion is that separate financial statements of an investee would include the minimum information required by

S-X 4-08(g) and therefore such information need not be repeated in the registrant's financial statement footnotes. As noted in Section 2405, in certain circumstances

S-X 3-09 financial statements may be filed after the original due date of the registrant's

Form 10-K. If

S-X 3-09 financial statements are not filed at the same time as the

Form 10-K, the registrant must include

S-X 4-08(g) summarized financial information in its audited financial statements included in the

Form 10-K.

NOTE to SECTION 2420.5

SAB Topic 6K.4.b. discusses the Annual Report to Shareholders. The Annual Report to Shareholders differs from the Annual Report on Form 10-K in certain significant respects. See Proxy Rules 14a-3 for a discussion of the Annual Report to Shareholders. However, CF-OCA applies the rationale in SAB Topic 6K.4.b. to the Annual Report on Form 10-K. |

2420.6

Other Reporting Companies - Interim Financial Statements — Overview [

S-X 10-01(b)(1)]

(Last updated: 3/31/2009)Present summarized statement of comprehensive income information for each investee for which both:

- Investee is significant, measured using either the income or investment tests described in S-X 1-02(w) substituting 20% for 10%; and

- Form 10-Q financial information (i.e., Part 1 of Form 10-Q) would be required if investee was a registrant. Examples of registrants that do not need to file Form 10-Q Part 1 include foreign private issuers, asset-backed issuers, mutual life insurance companies and certain mining companies. See Exchange Act Rule 13a-13 and Exchange Act Rule 15d-13 for a complete list and explanation.

NOTE to SECTION 2420.6

Measuring Significance — See Implementation points in Section 2420.7.

|

2420.7

Other Reporting Companies - Interim Financial Statements — Significance Tests Implementation Points [S-X 10-01(b)(1)]

- Income Test: Use the year-to-date interim period statement of comprehensive income for the current year in lieu of either the quarterly financial statements or the financial statements for the most recently completed fiscal year (except the first quarter where the quarterly and year-to-date period are the same); and

- Income Test: Omit income averaging [i.e., computational note 2 of S-X 1-02(w)].

- Investment Test: Use both the most recent balance sheet, which should correspond to the end of the year-to-date (cumulative) interim period used to measure significance under the income test, and the balance sheet as of the end of the most recently completed fiscal year that is included in the quarterly report.

NOTE to SECTION 2420.7

Investment Test — It is important to use the balance sheet as of the end of the most recently completed fiscal year that is included in the quarterly report as it may differ from the corresponding balance sheet included in the most recently filed Form 10-K if a transaction or event has occurred since filing the Form 10-K that requires retrospective application in the subsequently filed Form 10-Q, such as a change in accounting principle.

|

2420.8

Other Reporting Companies - Interim Financial Statements — Minimum Disclosure [S-X 10-01(b)(1)]

(Last updated: 6/30/2010)When interim summarized statement of comprehensive income information is required, it need only be provided for investees that are significant. Minimum disclosure for each significant investee, which may be aggregated with such minimum disclosure for other significant investees, must include: revenues; gross profit; income from continuing operations; and net income. If S-X 10-01(b)(1) significance is met for any year-to-date (cumulative) interim period included in a quarterly report (See Sections 2420.6 and 2420.7), then the registrant should present the minimum disclosure for both the current and prior year comparative year-to-date periods included in that quarterly report.

2420.9

Smaller Reporting Companies — Annual and Interim Financial Statements [S-X 8-03] (Last updated: 6/30/2010)Determine significance of each investee for any of the registrant's fiscal years required to be presented in the filing using all 3 tests in S-X 1-02(w) (investment, asset and income tests), substituting 20% for 10%. If significance of any individual or any combination of investee(s) exceeds 20%, include in the registrant's financial statement footnotes summarized financial data for all investees for each period presented. Summarized annual financial data should not be labeled "unaudited." Interim financial statements need only include summarized financial data for each investee that is significant. Summarized financial data should quantify at a minimum the investee's: revenues; gross profit; income from continuing operations; and net income.

NOTES to SECTION 2420.9

- Source of Requirement - The smaller reporting company requirement for summarized financial information is located within the S-X 8-03 requirements for interim financial statements. Notwithstanding the location of this requirement, the staff applies the S-X 8-03 requirement for summarized financial information to both annual and interim financial statements.

- Significance - S-X 8-03(b)(3) states that significance should be determined based on "a registrant's consolidated assets, equity or income from continuing operations." Comparing a registrant's investment to its equity, rather than its total assets as required in S-X 4-08(g) and S-X 10-01(b)(1), would likely have the unintended consequence of requiring a smaller reporting company registrant [as defined in S-K 10(f)] to disclose summarized financial information more often than a registrant that is not a smaller reporting company. The staff did not intend for the disclosure requirements for a smaller reporting company to be more onerous than those for a registrant that is not a smaller reporting company. Therefore, the staff determines significance for purposes of reporting summarized financial information by smaller reporting companies in a manner consistent with S-X 1-02(w), substituting 20% for 10%.

- De Minimis Exception - Annual Financial Statements - SAB Topic 6K.4.b. notes that the staff recognizes that exclusion of summarized information for certain, but not all, investees may be appropriate in some circumstances where it is impracticable to accumulate and the summarized information to be excluded is de minimis.

|

2420.10

Change from Cost Method to Equity Method - If a registrant's

financial statements are retroactively adjusted in accordance with

ASC 323-10-35-33 to reflect equity method accounting for an investment previously accounted for under the cost method, S-X 3-09 financial statements, or summarized financial information required by S-X 4-08(g), S-X 8-03, or S-X 10-01(b)(1), may be required for periods in which the cost method was previously used if the significance tests are met.

2420.11

Multiple Series Registrants - Information required by S-X 4-08(g) must be provided on an individual series level. See Section 2410.9 for more information.

(Last updated: 9/30/2009)