Search within this section

Select a section below and enter your search term, or to search all click Staff Legal Bulletins

Favorited Content

120 days before the release date disclosed in the previous year's proxy statement |

Proposals for a regularly scheduled annual meeting must be received at the company's principal executive offices not less than 120 calendar days before the release date of the previous year's annual meeting proxy statement. Both the release date and the deadline for receiving rule 14a-8 proposals for the next annual meeting should be identified in that proxy statement. |

14-day notice of defect(s)/response to notice of defect(s) |

If a company seeks to exclude a proposal because the shareholder has not complied with an eligibility or procedural requirement of rule 14a-8, generally, it must notify the shareholder of the alleged defect(s) within 14 calendar days of receiving the proposal. The shareholder then has 14 calendar days after receiving the notification to respond. Failure to cure the defect(s) or respond in a timely manner may result in exclusion of the proposal. |

80 days before the company files its definitive proxy statement and form of proxy |

If a company intends to exclude a proposal from its proxy materials, it must submit its no-action request to the Commission no later than 80 calendar days before it files its definitive proxy statement and form of proxy with the Commission unless it demonstrates "good cause" for missing the deadline. In addition, a company must simultaneously provide the shareholder with a copy of its no-action request. |

30 days before the company files its definitive proxy statement and form of proxy |

If a proposal appears in a company's proxy materials, the company may elect to include its reasons as to why shareholders should vote against the proposal. This statement of reasons for voting against the proposal is commonly referred to as a statement in opposition. Except as explained in the box immediately below, the company is required to provide the shareholder with a copy of its statement in opposition no later than 30 calendar days before it files its definitive proxy statement and form of proxy. |

Five days after the company has received a revised proposal |

If our no-action response provides for shareholder revision to the proposal or supporting statement as a condition to requiring the company to include it in its proxy materials, the company must provide the shareholder with a copy of its statement in opposition no later than five calendar days after it receives a copy of the revised proposal. |

Rule 14a-8 no-action requests submitted by registered investment companies and business development companies, as well as shareholder responses to those requests, should be sent to

U.S. Securities and Exchange Commission

Division of Investment Management Office of Chief Counsel 450 Fifth Street, N.W. Washington, D.C. 20549 All other rule 14a-8 no-action requests and shareholder responses to those requests should be sent to

U.S. Securities and Exchange Commission

Division of Corporation Finance Office of Chief Counsel 450 Fifth Street, N.W. Washington, D.C. 20549 |

View image

View image

Example

A company receives a proposal relating to executive compensation from a shareholder who owns only shares of the company's class B common stock. The company's class B common stock is entitled to vote only on the election of directors. Does the shareholder's ownership of only class B stock provide a basis for the company to exclude the proposal?

Yes. This would provide a basis for the company to exclude the proposal because the shareholder does not own securities entitled to be voted on the proposal at the meeting.

|

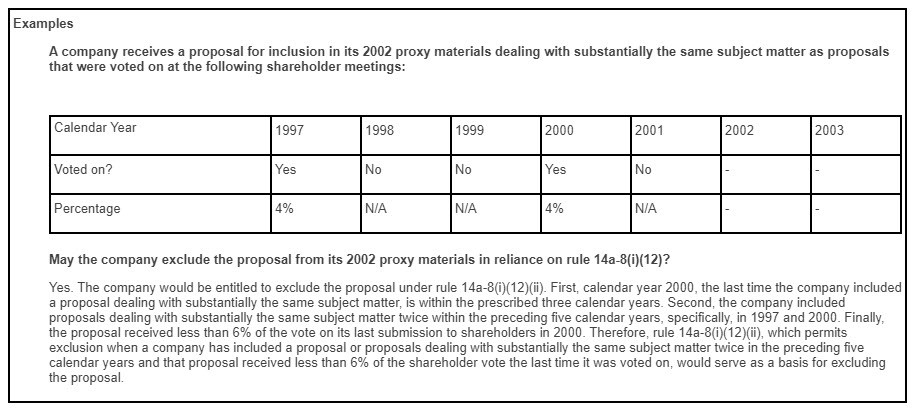

Examples

If a company is planning to have a regularly scheduled annual meeting in May of 2003 and the company disclosed that the release date for its 2002 proxy statement was April 14, 2002, how should the company calculate the deadline for submitting rule 14a-8 proposals for the company's 2003 annual meeting?

If the 120th calendar day before the release date disclosed in the previous year's proxy statement is a Saturday, Sunday or federal holiday, does this change the deadline for receiving rule 14a-8 proposals?

No. The deadline for receiving rule 14a-8 proposals is always the 120th calendar day before the release date disclosed in the previous year's proxy statement. Therefore, if the deadline falls on a Saturday, Sunday or federal holiday, the company must disclose this date in its proxy statement, and rule 14a-8 proposals received after business reopens would be untimely.

|

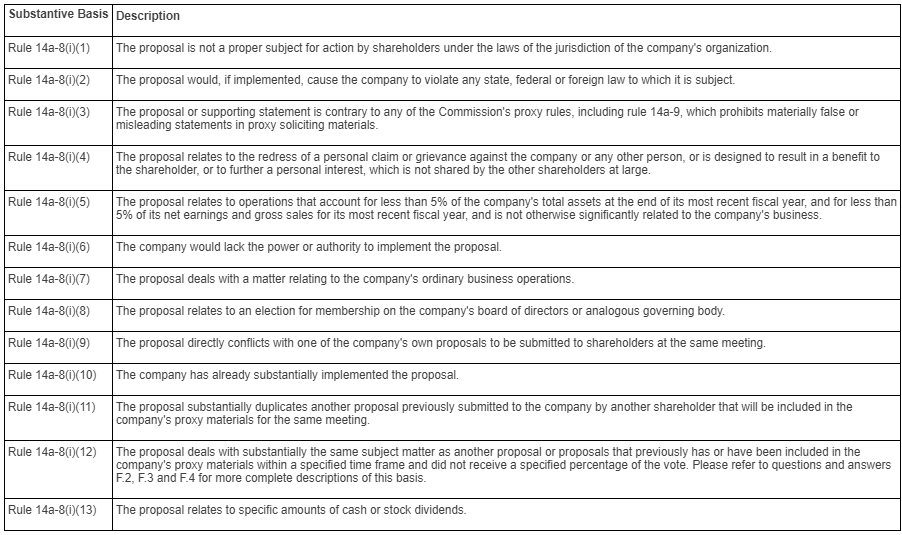

Basis |

Type of revision that we may permit |

Rule 14a-8(i)(1) |

When a proposal would be binding on the company if approved by shareholders, we may permit the shareholder to revise the proposal to a recommendation or request that the board of directors take the action specified in the proposal. |

Rule 14a-8(i)(2) |

If implementing the proposal would require the company to breach existing contractual obligations, we may permit the shareholder to revise the proposal so that it applies only to the company's future contractual obligations. |

Rule 14a-8(i)(3) |

If the proposal contains specific statements that may be materially false or misleading or irrelevant to the subject matter of the proposal, we may permit the shareholder to revise or delete these statements. Also, if the proposal or supporting statement contains vague terms, we may, in rare circumstances, permit the shareholder to clarify these terms. |

Rule 14a-8(i)(6) |

Same as rule 14a-8(i)(2), above. |

Rule 14a-8(i)(7) |

If it is unclear whether the proposal focuses on senior executive compensation or director compensation, as opposed to general employee compensation, we may permit the shareholder to make this clarification. |

Rule 14a-8(i)(8) |

If implementing the proposal would disqualify directors previously elected from completing their terms on the board or disqualify nominees for directors at the upcoming shareholder meeting, we may permit the shareholder to revise the proposal so that it will not affect the unexpired terms of directors elected to the board at or prior to the upcoming shareholder meeting. |

Rule 14a-8(i)(9) |

Same as rule 14a-8(i)(8), above. |

Example

A proposal received the following votes at the company's last annual meeting:

How is the shareholder vote of this proposal calculated for purposes of rule 14a-8(i)(12)?

This percentage is calculated as follows:  Applying this formula to the facts above, the proposal received 62.5% of the vote.

|

This is a work of the U.S. Government

Select a section below and enter your search term, or to search all click Staff Legal Bulletins