2. Add paragraphs 820-10-35-16A through 35-16G, with a link to transition paragraph 820-10-65-5, as follows:

820-10-35-16A A fair value measurement assumes that a liability is exchanged in an orderly transaction between market participants. However, liabilities are rarely transferred in the marketplace because of contractual or other legal restrictions preventing the transfer of liabilities. Some liabilities (for example, debt obligations), however, are traded in the marketplace as assets.

820-10-35-16B If a quoted price in an active market for the identical liability is available, it represents a Level 1 measurement. In circumstances in which a quoted price in an active market for the identical liability is not available, a reporting entity shall measure fair value using one or more of the following techniques:

a. A valuation technique that uses:

1. The quoted price of the identical liability when traded as an asset

2. Quoted prices for similar liabilities or similar liabilities when traded as assets.

b. Another valuation technique that is consistent with the principles of this Topic. Two examples would be an income approach, such as a present value technique, or a market approach, such as a technique that is based on the amount at the measurement date that the reporting entity would pay to transfer the identical liability or would receive to enter into the identical liability.

820-10-35-16C In all instances, the reporting entity shall maximize the use of relevant observable inputs and minimize the use of unobservable inputs. Furthermore, a reporting entity shall apply all applicable guidance in this Topic in determining fair value when the volume and level of activity for an asset or liability have significantly decreased and in identifying transactions that are not orderly.

820-10-35-16D When measuring the fair value of a liability using the quoted price of the liability when traded as an asset, the reporting entity shall not adjust the quoted price of the asset for the effect of a restriction preventing its sale. However, the quoted price of the liability when traded as an asset shall be adjusted for factors specific to the asset that are not applicable to the fair value measurement of the liability. Some circumstances in which a reporting entity shall consider whether the quoted price of the asset should be adjusted include the following:

- The quoted price for the asset relates to a similar (but not identical) liability traded as an asset.

- The unit of account for the asset is not the same as for the liability (for example, the quoted price for the asset includes the effect of a third-party credit enhancement). See paragraph 820-10-35-18A for further guidance.

820-10-35-16E When estimating the fair value of a liability, a reporting entity shall not include a separate input or adjustment to other inputs relating to the existence of a restriction that prevents the transfer of the liability (see paragraphs 820-10-55-71 through 55-76). The effect of a restriction that prevents the transfer of a liability is either implicitly or explicitly already included in the other inputs to the fair value measurement. For example, at the transaction date, both the creditor and the obligor are willing to accept the transaction price for the liability with full knowledge that the obligation includes a restriction that prevents its transfer. As a result of the restriction already being included in the transaction price, a separate input or adjustment to an existing input into the fair value measurement of a liability is not required at the transaction date to reflect the effect of the restriction on transfer. Additionally, a separate input or adjustment to other inputs into the fair value measurement of a liability is not required at subsequent measurement dates to reflect the effect of the restriction on transfer.

820-10-35-16F In addition, there are two fundamental differences between the fair value measurement of an asset and a liability that justify different treatments for asset restrictions and for liability restrictions. First, restrictions on the transfer of a liability relate to performance under the obligation (that is, the reporting entity is legally obligated to satisfy the obligation and needs to do something to be relieved of the obligation), whereas restrictions on the transfer of an asset relate to the marketability of the asset. Second, virtually all liabilities include a restriction preventing the transfer of the liability, whereas most assets do not include a similar restriction. As a result, the effect of a restriction preventing the transfer of a liability would, theoretically, be consistent for all liabilities. However, the inclusion of a restriction preventing the sale of the asset typically results in a lower fair value for the restricted asset versus the nonrestricted asset, all other factors being equal.

820-10-35-16G When measuring the fair value of a liability using a valuation technique, a reporting entity shall ensure that the fair value measurement is consistent with the principles of this Topic, that is, the price that would be paid to transfer a liability in an orderly transaction between market participants at the measurement date. For example, when using a technique based on the amount at the measurement date that the reporting entity would receive to enter into the identical liability (see paragraph 820-10-35-16B), the inputs shall reflect the assumptions that market participants would use (or the reporting entity's own assumption about the assumptions that market participants would use) in the principal or most advantageous market for issuance of a liability with the same contractual terms.

3. Amend paragraph 820-10-35-41, with a link to transition paragraph 820-10-65-5, as follows:

820-10-35-41 A quoted price in an active market provides the most reliable evidence of fair value and shall be used to measure fair value whenever available, except as discussed in

the following

paragraphs

820-10-35-16D, 820-10-35-42, and

paragraph

820-10-35-43.

4. Add paragraph 820-10-35-41A, with a link to transition paragraph 820-10-65-5, as follows:

820-10-35-41A A Level 1 fair value measurement for the liability is a quoted price in an active market for the identical liability at the measurement date. In addition, the quoted price for the identical liability when traded as an asset in an active market also is a Level 1 fair value measurement for that liability when no adjustments to the quoted price of the asset are required. However, a reporting entity needs to determine whether the quoted price for the identical liability when traded as an asset in an active market should be adjusted for factors specific to the liability and the asset (see paragraph 820-10-35-16D). Any adjustment to the quoted price of the asset shall render the fair value measurement of the liability a lower level measurement.

5. Amend paragraph 820-10-35-50, with a link to transition paragraph 820-10-65-5, as follows:

820-10-35-50 Adjustments to Level 2 inputs will vary depending on factors specific to the asset or liability. Those factors include the following:

- The condition and/or location of the asset or liability

- The extent to which the inputs relate to items that are comparable to the asset or liability, including those factors discussed in paragraph 820-10-35-16D

- The volume and level of activity in the markets within which the inputs are observed.

6. Add paragraphs 820-10-55-65 through 55-76 and related headings, with a link to transition paragraph 820-10-65-5, as follows:

> > Example 9: Measuring Liabilities

820-10-55-65 The following Cases illustrate the measurement of liabilities:

- Asset Retirement Obligation (Case A)

- Debt Obligation: Quoted Price (Case B)

- Debt Obligation: Present Value Technique (Case C).

> > > Case A: Asset Retirement Obligation

820-10-55-66 On January 1, 20X1, Entity A completes construction of and places into service an offshore oil platform. The entity is legally required to dismantle and remove the platform at the end of its useful life, which is estimated to be 10 years. According to the guidance in paragraph 410-20-25-4, the entity is required to recognize, at fair value, an asset retirement obligation.

820-10-55-67 On the basis of the guidance in paragraph 410-20-30-1, Entity A uses the expected present value technique to measure the fair value of the asset retirement obligation.

820-10-55-68 If Entity A was contractually allowed to transfer its asset retirement obligation to a market participant, Entity A believes a market participant would use all of the following inputs, probability-weighted as appropriate, in determining the price it would expect to receive:

- Labor costs

- Allocation of overhead costs

- Profit on labor and overhead costs

- Effect of inflation on estimated costs and profits

- Risk premium for bearing the uncertainty inherent in cash flows, other than inflation

- Time value of money, represented by the risk-free rate

- Nonperformance risk relating to the liability, including Entity A's own credit risk.

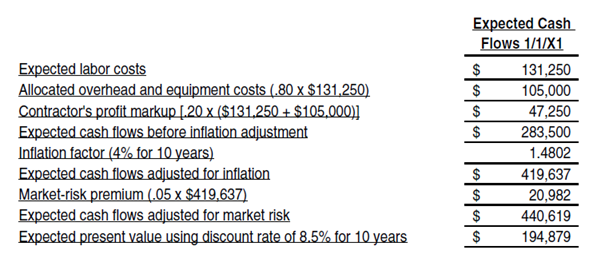

820-10-55-69 The significant assumptions used in Entity A's estimate of fair value are as follows:

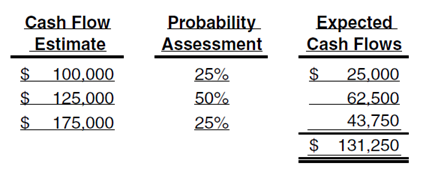

a. Labor costs are based on current marketplace wages required to hire contractors to dismantle and remove offshore oil platforms. Entity A assigns probability assessments to a range of cash flow estimates as follows.

The probability assessments are based on Entity A's experience with fulfilling obligations of this type and its knowledge of the market.

b. Entity A estimates allocated overhead and equipment operating costs using the rate it applies to labor costs (80 percent of expected labor costs). This is consistent with the cost structure of market participants.

c. A contractor typically adds a markup on labor and allocated internal costs to provide a profit margin on the job. The profit margin used (20 percent) represents Entity A's understanding of the operating profit that contractors in the industry generally earn to dismantle and remove offshore oil platforms. Entity A believes this rate is consistent with the rate a market participant would demand as a return for bearing the obligation.

d. Entity A assumes a rate of inflation of 4 percent over the 10-year period on the basis of available market data.

e. A contractor would typically demand and receive a premium (market risk premium) for bearing the uncertainty inherent in locking in today's price for a project that will not occur for 10 years. Entity A estimates the amount of that premium to be 5 percent of the expected cash flows, adjusted for inflation.

f. The risk-free rate of interest for a 10-year maturity on January 1, 20X1, is 5 percent. Entity A adjusts that rate by 3.5 percent to reflect its risk of nonperformance. Therefore, the discount rate used to compute the present value of the cash flows is 8.5 percent.

820-10-55-70 Entity A believes that its assumptions would be used by market participants. In addition, Entity A does not adjust its fair value measurement for the existence of a restriction preventing it from transferring the liability. As illustrated in the following table, Entity A estimates the fair value of its liability for the asset retirement obligation to be $194,879.

> > > Case B: Debt Obligation: Quoted Price

820-10-55-71 On January 1, 20X1, Entity B issues at par a $2 million BBB-rated exchange-traded 5-year fixed-rate debt instrument with an annual 10 percent interest coupon. Entity B has elected to account for this instrument under the fair value option.

820-10-55-72 On December 31, 20X1, the instrument is trading as an asset in an active market at $929 per $1,000 of par value after payment of accrued interest. Entity B uses the quoted price for the asset in an active market as its initial input into the fair value measurement of its liability ($929 × [$2 million ÷ $1,000] = $1,858,000). In determining whether the quoted price for the asset in an active market represents the fair value of the liability, Entity B evaluates whether the quoted price for the asset includes the effect of factors not applicable to the fair value measurement of a liability, for example, whether the quoted price for the asset includes the effect of third-party credit enhancements. Entity B determines that no adjustments are required to the quoted price of the asset. Accordingly, Entity B concludes that the fair value of its debt instrument at December 31, 20X1, is $1,858,000. Entity B categorizes and discloses the fair value measurement of its debt instrument as a Level 1 measurement.

> > > Case C: Debt Obligation: Present Value Technique

820-10-55-73 On January 1, 20X1, Entity C issues at par in a private placement a $2 million BBB-rated 5-year fixed-rate debt instrument with an annual 10 percent interest coupon. Entity C has elected to account for this instrument under the fair value option.

820-10-55-74 At December 31, 20X1, Entity C still carries a BBB credit rating. Market conditions, including available interest rates, credit spreads for a BBB-quality credit rating and liquidity, remain unchanged from the issuance date of the debt instrument. However, Entity C's credit spread has deteriorated by 50 basis points due to a change in its risk of nonperformance. After considering all market conditions, Entity C concludes that if it was to issue the instrument at the measurement date, the instrument would bear a rate of interest of 10.5 percent or Entity C would receive less than par in proceeds from the issuance of the instrument.

820-10-55-75 For the purpose of this example, the fair value of Entity C's liability is calculated using a present value technique. Entity C believes a market participant would use all of the following inputs (consistent with paragraph 820-10-55-5) in determining the price the market participant would expect to receive to assume Entity C's obligation:

a. Terms of the debt instrument, including all of the following:

1. Coupon interest rate of 10 percent

2. Principal amount of $2 million

3. Term of 4 years.

b. Change in risk of nonperformance from the date of issuance of 50 basis points.

820-10-55-76 On the basis of its present value technique, Entity C concludes that the fair value of its liability at December 31, 20X1, is $1,968,641. Entity C does not include any additional input into its present value technique for risk or profit that a market participant might require for compensation for assuming the liability. Because Entity C's obligation is a financial liability, Entity C believes the interest rate already captures the risk or profit that a market participant would require for compensation for assuming the liability. Furthermore, Entity C does not adjust its present value technique for the existence of a restriction preventing it from transferring the liability.

7. Add paragraph 820-10-65-5 and related heading as follows:

> Transition Related to Accounting Standards Update 2009-05, Measuring Liabilities under Topic 820

820-10-65-5 The following represents the transition and effective date information related to Accounting Standards Update 2009-05:

- The pending content that links to this paragraph shall be effective for the first reporting period, including interim periods, beginning after issuance.

- Early application is permitted if financial statements for prior periods have not been issued.

- Revisions resulting from a change in valuation technique or its application shall be accounted for as a change in accounting estimate (see the guidance beginning in paragraph 250-10-45-17).

- In the period of adoption, a reporting entity shall disclose a change, if any, in valuation technique and related inputs resulting from the application of the pending content that links to this paragraph, and quantify the total effect, if practicable.