Search within this section

Select a section below and enter your search term, or to search all click ASU 2010-20—Receivables (Topic 310)

Favorited Content

Copyright © 2010 by Financial Accounting Foundation. All rights reserved. Content copyrighted by Financial Accounting Foundation may not be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the Financial Accounting Foundation. Financial Accounting Foundation claims no copyright in any portion hereof that constitutes a work of the United States Government.

|

Paragraph Number |

Action |

Accounting Standards Update |

Date |

Class of Financing Receivable |

Added |

2010-20 |

07/21/2010 |

Credit Quality Indicator |

Added |

2010-20 |

07/21/2010 |

Financing Receivable |

Added |

2010-20 |

07/21/2010 |

Portfolio Segment |

Added |

2010-20 |

07/21/2010 |

Related Parties |

Added |

2010-20 |

07/21/2010 |

Troubled Debt Restructuring |

Added |

2010-20 |

07/21/2010 |

310-10-15-2 |

Amended |

2010-20 |

07/21/2010 |

310-10-35-11 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-1 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-1A |

Added |

2010-20 |

07/21/2010 |

310-10-50-2 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-4 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-4A |

Added |

2010-20 |

07/21/2010 |

310-10-50-5A |

Added |

2010-20 |

07/21/2010 |

310-10-50-5B |

Added |

2010-20 |

07/21/2010 |

310-10-50-6 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-7 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-7A |

Added |

2010-20 |

07/21/2010 |

310-10-50-7B |

Added |

2010-20 |

07/21/2010 |

310-10-50-9 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-10 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-11A through 50-11C |

Added |

2010-20 |

07/21/2010 |

310-10-50-12 |

Superseded |

2010-20 |

07/21/2010 |

310-10-50-13 |

Superseded |

2010-20 |

07/21/2010 |

310-10-50-14A |

Added |

2010-20 |

07/21/2010 |

310-10-50-15 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-17 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-20 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-21 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-22 |

Superseded |

2010-20 |

07/21/2010 |

310-10-50-23 |

Superseded |

2010-20 |

07/21/2010 |

310-10-50-26 |

Amended |

2010-20 |

07/21/2010 |

310-10-50-27 through 50-34 |

Added |

2010-20 |

07/21/2010 |

310-10-55-2 |

Amended |

2010-20 |

07/21/2010 |

310-10-55-3 |

Amended |

2010-20 |

07/21/2010 |

310-10-55-7 through 55-22 |

Added |

2010-20 |

07/21/2010 |

310-10-65-2 |

Added |

2010-20 |

07/21/2010 |

Paragraph Number |

Action |

Accounting Standards Update |

Date |

Financing Receivable |

Added |

2010-20 |

07/21/2010 |

310-40-50-1A |

Added |

2010-20 |

07/21/2010 |

310-40-50-5 |

Amended |

2010-20 |

07/21/2010 |

310-40-50-6 |

Amended |

2010-20 |

07/21/2010 |

Paragraph Number |

Action |

Accounting Standards Update |

Date |

Financing Receivable |

Added |

2010-20 |

07/21/2010 |

840-30-50-4A |

Added |

2010-20 |

07/21/2010 |

840-30-50-5A |

Added |

2010-20 |

07/21/2010 |

Paragraph Number |

Action |

Accounting Standards Update |

Date |

Financing Receivable |

Added |

2010-20 |

07/21/2010 |

270-10-50-1 |

Amended |

2010-20 |

07/21/2010 |

Paragraph Number |

Action |

Accounting Standards Update |

Date |

450-20-50-2A |

Added |

2010-20 |

07/21/2010 |

Element Name |

Standard Label |

Definition |

Codification Reference |

ReceivablesPolicyTextBlock* |

Receivables, Policy |

Describes an entity's accounting policy for trade and other accounts receivable, and finance, loan and lease receivables, including those classified as held for investment and held for sale. This disclosure may include (1) the basis at which such receivables are carried in the entity's statements of financial position (2) how the level of the valuation allowance for receivables is determined (3) when impairments, charge-offs or recoveries are recognized for such receivables (4) the treatment of origination fees and costs, including the amortization method for net deferred fees or costs (5) the treatment of any premiums or discounts or unearned income (6) the entity's income recognition policies for such receivables, including those that are impaired, past due or placed on nonaccrual status and (7) the treatment of foreclosures or repossessions (8) the nature and amount of any guarantees to repurchase receivables. |

310-20-50-4; 310-20; 310-20-50-1; 310-10-50-6; 310-10-50-15(b); 310-10-50-2; 310-10-50-9; 235-10-50-3; 310-10 |

TradeAndOtherAccountsReceivablePolicy* |

Trade and Other Accounts Receivable, Policy |

Describes an entity's accounting policy for trade and other accounts receivables. This disclosure may include the basis at which such receivables are carried in the entity's statements of financial position (for example, net realizable value), how the entity determines the level of its allowance for doubtful accounts, when impairments, charge-offs or recoveries are recognized, and the entity's income recognition policies for such receivables, including its treatment of related fees and costs, its treatment of premiums, discounts or unearned income, when accrual of interest is discontinued, how the entity records payments received on nonaccrual receivables and its policy for resuming accrual of interest on such receivables. If the enterprise holds a large number of similar loans, disclosure may include the accounting policy for the anticipation of prepayments and significant assumptions underlying prepayment estimates for amortization of premiums, discounts, and nonrefundable fees and costs. |

235-10-50-3; 310-10-50-2; 310-10-50-6; 310-10-50-15(d) |

FinanceLoansAndLeasesReceivablePolicy* |

Finance, Loans and Leases |

Describes an entity's accounting policy for finance, |

310-10-50-6;310-10-50-9;235-10-50-3; |

Receivable, Policy |

loan and lease receivables, including those held for investment and those held for sale. This disclosure may include (1) the basis at which such receivables are carried in the entity's statements of financial position (2) how the level of the allowance for loan and lease losses is determined (3) when impairments, charge-offs or recoveries are recognized for such receivables (4) the treatment of origination fees and costs, including the amortization method for net deferred fees or costs (5) the treatment of any premiums or discounts or unearned income (6) the entity's income recognition (revenues, expenses and gains and losses arising from committing to issue, issuing, granting, collecting, terminating, modifying and holding loans)policies for such receivables, including those that are impaired, past due or placed on nonaccrual status and (7) the treatment of foreclosures or repossessions. |

310-10-50-2; 310-10-50-15(b) and 15(d) |

|

LoansAndLeasesReceivableNonaccrualLoanAndLeaseStatusPolicy* |

Loans and Leases Receivable Nonaccrual Loan and Lease Status, Policy |

Describes the policy as to when a loan ceases to accrue interest or other revenue because the borrower is in financial difficulty. May also describe the treatment of previously earned but uncollected interest income on loans in nonaccrual status, how cash received from borrowers is recorded on loans that are in nonaccrual status, and the policy for resuming accrual of interest. Also includes the policy for charging off uncollectible loans and trade receivables, and the policy for determining past-due or delinquency status (i.e. whether past-due status is based on how recently payments have been received or on contractual terms). |

310-10; 235-10-50-3; 310-10-50-6; 310-10-50-15(b) and 15(d) |

ScheduleOfFinancingReceivablesPastDueTable |

Schedule of Financing Receivables Past Due |

Schedule detailing the recorded investment of financing receivables that are past due but not impaired and financing receivables that are 90 days past due and still accruing. The schedule also includes financing receivables on nonaccrual status. |

310-10-50-7;310-10-50-7A |

FinancingReceivableRecordedInvestmentByClassOfFinancingReceivableAxis |

Financing Receivable, Recorded Investment, By Class of Financing Receivable |

Recorded investment in financing receivables past due, 90 days past due and still accruing, and receivables on nonaccrual status by class of financing receivables. |

310-10-50-7; 310-10-50-7A |

FinancingReceivableRecordedInvestmentClassOfFinancingReceivableDomain |

Financing Receivable, Recorded Investment, Class of Financing Receivable |

Listing of the classes of financing receivables. Classes of financing receivables generally are a disaggregation of a portfolio segment. |

Class of Financing Receivable |

ClassOfFinancingReceivableMember |

Class of Financing Receivable |

Class of financing receivables. Classes of financing receivables are generally a disaggregation of a portfolio segment. |

Class of Financing Receivable |

CommercialRealEstateConstructionFinancingReceivableMember |

Commercial Real Estate Construction Financing Receivable |

Class of financing receivables related to commercial real estate construction financing receivables. |

Class of Financing Receivable |

CommercialRealEstateOtherReceivable Member |

Commercial Real Estate Other Receivable |

Class of financing receivables related to real estate financing receivables other than those related to commercial real estate construction. |

Class of Financing Receivable |

ConsumerCreditCardFinancingReceivab leMember |

Consumer Credit Card Financing Receivable |

Class of financing receivables related to consumer credit card financing receivables. |

Class of Financing Receivable |

ConsumerOtherFinancingReceivableMember |

Consumer Other Financing Receivable |

Class of financing receivables related to other consumer financing receivables. |

Class of Financing Receivable |

ConsumerAutoFinancingReceivableMember |

Consumer Auto Financing Receivable |

Class of financing receivables related to consumer auto financing receivables |

Class of Financing Receivable |

ResidentialPrimeFinancingReceivableMember |

Residential, Prime, Financing Receivable |

Class of financing receivables related to prime residential financing receivables. |

Class of Financing Receivable |

ResidentialSubprimeFinancingReceivableMember |

Residential, Subprime, Financing Receivable |

Class of financing receivables related to subprime residential financing receivables. |

Class of Financing Receivable |

FinanceLeasesFinancingReceivableMember |

Finance Leases Financing Receivable |

Class of financing receivables related to finance lease financing receivables. |

Class of Financing Receivable |

FinancingReceivableRecordedInvestmentPastDueLineItems |

Financing Receivable, Recorded Investment, Past Due |

Line items represent financial concepts included in a table. These concepts are used to disclose reportable information associated with domain members defined in one or many axes to the table. |

|

FinancingReceivableRecordedInvestmentCurrent |

Financing Receivable, Recorded Investment, Current |

Financing receivables that are current. |

310-10-50-7A |

FinancingReceivableRecordedInvestment1To29DaysPastDue |

Financing Receivable, Recorded Investment, 1 - 29 Days Past Due |

Financing receivables that are less 30 days past due. |

310-10-50-7A |

FinancingReceivableRecordedInvestment30To59DaysPast Due |

Financing Receivable, Recorded Investment, 30 - 59 Days Past Due |

Financing receivables that are less than 60 days past due but 29 or more days past due. |

310-10-50-7A |

FinancingReceivableRecordedInvestment60To89DaysPast Due |

Financing Receivable, Recorded Investment, 60 - 89 Days Past Due |

Financing receivables that are less than 90 days past due but 59 or more days past due. |

310-10-50-7A |

FinancingReceivableRecordedInvestmentEqualToorGreater Than90DaysPastDue |

Financing Receivable, Recorded Investment, Equal to or Greater Than 90 Days Past Due |

Financing receivables that are equal to or greater than 90 days past due. |

310-10-50-7A |

FinancingReceivableRecordedInvestmentGreaterThan90Da ysPastDueAndStillAccruing |

Financing Receivable, Recorded Investment, 90 Days Past Due and Still Accruing |

Financing receivables that are 90 days past due and still accruing. |

310-10-50-7(b) |

FinancingReceivableRecordedInvestmentPastDue |

Financing Receivable, Recorded Investment, Past Due |

Recorded investment of financing receivables that are past due at the balance sheet date. |

310-10-50-7A |

FinancingReceivableRecordedInvestmentNonaccrualStatus |

Financing Receivable, Recorded Investment, Nonaccrual Status |

Financing receivables that are on nonaccrual status as of the balance sheet date. |

310-10-50-7(a) |

Financing ReceivableAllowanceForCreditLossesTable |

Financing Receivable, Allowance for Credit Losses |

Schedule detailing information related to financing receivables and the activity in the allowance for credit losses account by portfolio segment. |

310-10-50- 11B(c) |

FinancingReceivableAllowanceActivityAxis |

Financing Receivable Allowance Activity |

Information related to financing receivables and activity in the allowance for credit losses by financing receivable portfolio segment. |

310-10-50- 11B(c) |

FinancingReceivableAllowanceDomain |

Financing Receivable Allowance |

Represents financing receivable portfolio segments. |

310-10-50- 11B(c) |

CommercialPortfolioSegmentMember |

Commercial Portfolio Segment |

Portfolio segment of the company's total financing receivables related to commercial receivables. |

310-10-50-11B |

ConsumerPortfolioSegmentMember |

Consumer Portfolio Segment |

Portfolio segment of the company's total financing receivables related to consumer receivables. |

310-10-50-11B |

CommercialRealEstatePortfolioSegment Member |

Commercial Real Estate Portfolio Segment |

Portfolio segment of the company's total financing receivables related to commercial real estate. |

310-10-50-11B |

ResidentialPortfolioSegmentMember |

Residential Portfolio Segment |

Portfolio segment of the company's total financing receivables related to residential financing receivables. |

310-10-50-11B |

FinanceLeasesPortfolioSegmentMember |

Finance Leases Portfolio Segment |

Portfolio segment of the company's total financing receivables related to finance leases. |

310-10-50-11B |

FinancingReceivableAllowanceForCreditLossesLineItems |

Financing Receivable, Allowance for Credit Losses |

Line items represent financial concepts included in a table. These concepts are used to disclose reportable information associated with domain members defined in one or many axes to the table. |

|

FinancingReceivableAllowanceForCreditLossesRollForward |

Financing Receivable, Allowance for Credit Losses |

||

FinancingReceivableAllowanceForCreditLosses |

Financing Receivable, Allowance for Credit Losses |

A valuation allowance for financing receivables that are expected to be uncollectible. |

310-10-50-11B(c)(1) |

FinancingReceivableAllowanceForCreditLossesWriteOffs |

Financing Receivable, Allowance for Credit Losses, Write -offs |

Reduction to the allowance for credit losses related to financing receivables deemed uncollectible. |

310-10-50- 11B(c)(3) |

Financing Receivable, AllowanceForCreditLossesRecoveries |

Financing Receivable, Allowance for Credit Losses, Recoveries |

Reduction to the allowance for credit losses related to collections on financing receivables which have been partially or fully charged off as bad debts. |

310-10-50- 11B(c)(5) |

FinancingReceivableAllowanceForCreditLossesProvisions |

Financing Receivable, Allowance for Credit Losses, Provisions |

Charge to expense for financing receivables that are expected to be uncollectible. |

310-10-50- 11B(c)(2) |

FinancingReceivableAllowanceForCreditLossesEffectOfChangeInMethod |

Financing Receivable, Allowance for Credit Losses, Effect of Change in Method |

The effect of a change in method or methods for calculating the allowance for credit losses on the current period provision. |

310-10-50- 11B(c)(4) |

FinancingReceivableAllowanceForCreditLossesPeriodIncreaseDecrease |

Financing Receivable, Allowance for Credit Losses, Period Increase (Decrease) |

Net change in the allowance for credit losses related to financing receivables. |

310-10-50- 11B(c) |

FinancingReceivableRiskCharacteristicsUsedInEstimatingAllowanceForCreditLosses |

Financing Receivable, Risk Characteristics Used in Estimating Allowance for Credit Losses |

Description of the risk characteristics used in estimating the allowance for credit losses. |

310-10-50- 11B(a)(2) |

FinancingReceivableAllowanceForCreditLossesIndividuallyEvaluatedForImpairment |

Financing Receivable, Allowance for Credit Losses, Individually Evaluated for Impairment |

Ending balance of allowance for credit losses related to financing receivables individually evaluated for impairment. |

310-10-50- 11B(f) |

FinancingReceivableAllowanceForCreditLossesCollectively EvaluatedForImpairment |

Financing Receivable, Allowance for Credit Losses, Collectively Evaluated for Impairment |

Ending balance of allowance for credit losses related to financing receivables collectively evaluated for impairment. |

310-10-50- 11B(f) |

FinancingReceivableAllowanceForCreditLossesAcquiredWithDeterioratedCredit Quality |

Financing Receivable, Allowance for Credit Losses, Acquired with Deteriorated Credit Quality |

Ending balance of allowance for credit losses related to financing receivables acquired with deteriorated credit quality. |

310-10-50- 11B(f) |

FinancingReceivableIndividuallyEvaluatedForImpairment |

Financing Receivable, Individually Evaluated for Impairment |

The balance of financing receivables that were individually evaluated for impairment. |

310-10-50- 11B(g) |

FinancingReceivableCollectivelyEvaluatedForImpairment |

Financing Receivable, Collectively Evaluated for Impairment |

The balance of financing receivables that were collectively evaluated for impairment. |

310-10-50- 11B(g) |

FinancingReceivableAcquiredWithDeterioratedCreditQuality |

Financing Receivable, Acquired with Deteriorated Credit Quality |

The balance of financing receivables acquired with deteriorated credit quality. |

310-10-50- 11B(g) |

FinancingReceivableAllowanceForCreditLossesFactorsThatInfluencedManagementsJudgment |

Financing Receivable, Allowance for Credit Losses, Factors that Influenced Management's Judgment |

A description of the factors that influenced management's judgment concerning the allowance for credit losses. |

310-10-50- 11B(a)(1) |

FinancingReceivableAllowanceForCreditLossesRiskCharacteristics |

Financing Receivable, Allowance for Credit Losses, Risk Characteristics |

A description of the risk elements relevant to each portfolio segment. |

310-10-50- 11B(a)(2) |

FinancingReceivableAllowanceForCreditLossesPolicyOrMethodologyChange |

Financing Receivable, Allowance for Credit Losses, Policy or Methodology Change |

A description of any changes to a creditor's accounting policies or methodology from the prior period and management's rationale for the change should be discussed. |

310-10-50- 11B(a)(3) |

FinancingReceivableAllowanceForCreditLossesPolicyForUncollectibleAmounts |

Financing Receivable, Allowance for Credit Losses, Policy for Uncollectible Amounts |

A description of the policy for charging off uncollectible financing receivables. |

310-10-50- 11B(b) |

FinancingReceivableSignificantPurchases |

Financing Receivable, Significant Purchases |

The amount of any significant purchases of financing receivables during the reporting period. |

310-10-50- 11B(d) |

FinancingReceivableSignificantSales |

Financing Receivable, Significant Sales |

The amount of any significant sales of financing receivables during the reporting period. |

310-10-50- 11B(e) |

FinancingReceivableReclassificationToHeldForSale |

Financing Receivable, Reclassification to Held for Sale |

The amount of financing receivables reclassified to held for sale during the reporting period. |

310-10-50- 11B(e) |

FinancingReceivable |

Financing Receivable |

A contractual right to receive money on demand or on fixed or determinable dates that is recognized as an asset in the creditor's statement of financial position. Examples include, but are not limited to, accounts receivable (with terms exceeding one year), notes receivable and receivables relating to lessor's rights to payments from leases other than operating leases that have been recorded as assets. |

Financing Receivable |

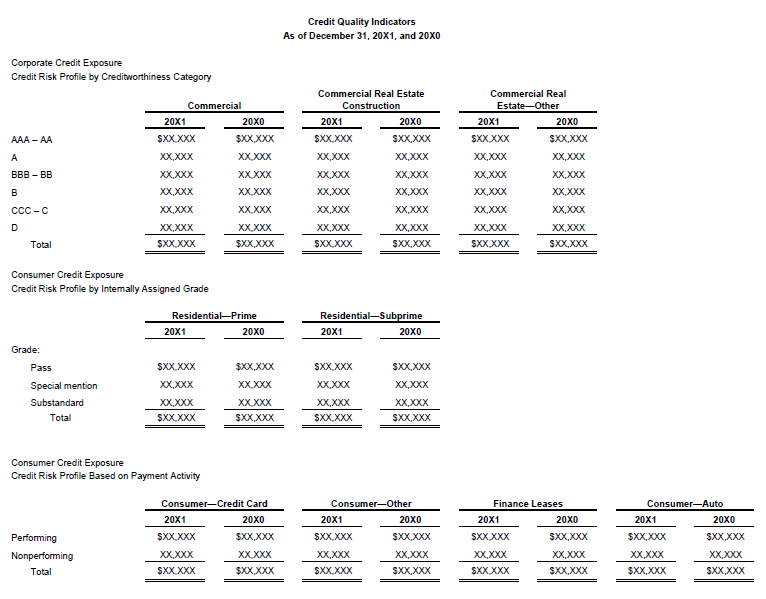

FinancingReceivableRecordedInvestmentCreditQualityTable |

Financing Receivable, Recorded Investment, Credit Quality Indicator |

Schedule detailing credit quality information related to financing receivables by credit quality indicator and by class of financing receivable. |

310-10-50-29 |

FinancingReceivableRecordedInvestmentByCreditQualityIndicatorAxis |

Financing Receivable, Recorded Investment, By Credit Quality Indicator |

The credit quality indicator of a financing receivable by class of financing receivable. |

310-10-50-29 |

FinancingReceivableByCreditQualityIndicatorDomain |

Financing Receivable, By Credit Quality Indicator |

Credit quality indicators related to financing receivables. |

310-10-50-29 |

ConsumerCreditScoreMember |

Consumer Credit Score |

Set of credit quality indicators related to consumer credit scores. |

310-10-50-29 |

PassMember |

Pass |

A category of financing receivables not considered to be special mention, substandard, doubtful, and loss receivables. |

310-10-50-29 |

SpecialMentionMember |

Special Mention |

A category of financing receivables considered to have potential weaknesses that deserve management's close attention. If left uncorrected, those potential weaknesses may result in a deterioration of the repayment prospects for the asset or of the creditor's position at some future date. |

310-10-50-29 |

SubstandardMember |

Substandard |

A category of financing receivables that are inadequately protected by the current sound worth and paying capacity of the obligor or of the collateral pledged, if any. Loans so classified have a well-defined weakness or weaknesses that jeopardize the liquidation of the debt. They are characterized by the distinct possibility that the creditor will sustain some loss if the deficiencies are not corrected. |

310-10-50-29 |

DoubtfulMember |

Doubtful |

A category of financing receivables that have all the weaknesses inherent in those classified as substandard, with the added characteristic that the weaknesses make collection or liquidation in full, on the basis of currently existing facts, conditions, and values, highly questionable and improbable. |

310-10-50-29 |

LossMember |

Loss |

A category of financing receivables that are considered uncollectible or of little value. This classification does not mean that the loan has absolutely no recovery or salvage value, but rather, that it is not practical or desirable to defer writing off this basically worthless asset even though partial recovery may be affected in the future. |

310-10-50-29 |

PerformingFinancingReceivableMember |

Performing Financing Receivable |

A category of financing receivables that are current in regards to payments made on the financing receivables. |

310-10-50-29 |

NonperformingFinancingReceivableMember |

Nonperforming Financing Receivable |

A category of financing receivables that are not current in regards to payments made on the financing receivables. |

310-10-50-29 |

CorporateCreditQualityIndicatorMember |

Corporate Credit Quality Indicator |

Credit quality indicators related to corporate risk profiles. |

310-10-50-29 |

InternallyAssignedGradeMember |

Internally Assigned Grade |

Credit quality indicators that are developed and used internally by the company. |

310-10-50-29 |

FinancingReceivableRecordedInvestmentLineItems |

Financing Receivable, Carrying Amount |

Line items represent financial concepts included in a table. These concepts are used to disclose reportable information associated with domain members defined in one or many axes to the table. |

|

FinancingReceivableCreditQualityAdditionalInformation |

Financing Receivable, Credit Quality, Additional Information |

Includes any additional disclosures related to the credit quality of financing receivables. This may include a description of a credit quality indicator or a description of how the internal risk ratings used by a company relate to the likelihood of loss. |

310-10-50- 29(a); 310-1050-30 |

FinancingReceivableCreditQualityDateRatingsUpdated |

Financing Receivable, Credit Quality, Date Ratings Updated |

Includes a disclosure detailing the date that the consumer credit scores were last updated. |

310-10-50- 29(c) |

FinancingReceivableCreditQualityRangeOfDatesRatingsUpdated |

Financing Receivable, Credit Quality, Range of Dates Ratings Updated |

Includes a disclosure detailing the range of dates that the consumer credit scores were last updated. |

310-10-50- 29(c) |

ImpairedFinancingReceivableTable |

Impaired Financing Receivable |

Schedule detailing the carrying amount, unpaid principal balance, associated allowance, average carrying amount, accounting policies, and interest income recognized on the accrual and cash basis by class of financing receivable. |

310-10-50-15 |

ImpairedFinancingReceivablewithNoRelatedAllowanceAxis |

Impaired Financing Receivable with No Related Allowance |

Attributes of financing receivables classified as impaired with no allowance related to the receivables by class of financing receivable. |

310-10-50-15 |

ImpairedFinancingReceivableWithNoRelatedAllowanceDomain |

Impaired Financing Receivable with No Related Allowance |

Represents a subset of a class of financing receivables that have no allowances related to the impaired receivables. |

310-10-50-15 |

ImpairedFinancingReceivableWithNoRelatedAllowanceMember |

Impaired Financing Receivable with No Related Allowance |

Represents a subset of a class of financing receivables that have no allowances related to the impaired receivables. |

310-10-50-15 |

ImpairedFinancingReceivableWithARelatedAllowanceAxis |

Impaired Financing Receivable with a Related Allowance |

Attributes of financing receivables classified as impaired with allowance related to the receivables by class of financing receivable. |

310-10-50-15 |

ImpairedFinancingReceivableWithARelatedAllowanceDomain |

Impaired Financing Receivable with a Related Allowance |

Represents a subset of a class of financing receivables that have allowances related to the impaired receivables. |

310-10-50-15 |

ImpairedFinancingReceivableWithARelatedAllowanceMember |

Impaired Financing Receivable with a Related Allowance |

Represents a subset of a class of financing receivables that have allowances related to the impaired receivables. |

310-10-50-15 |

FinancingReceivableImpairedLineItems |

Financing Receivable, Impaired |

Line items represent financial concepts included in a table. These concepts are used to disclose reportable information associated with domain members defined in one or many axes to the table. |

|

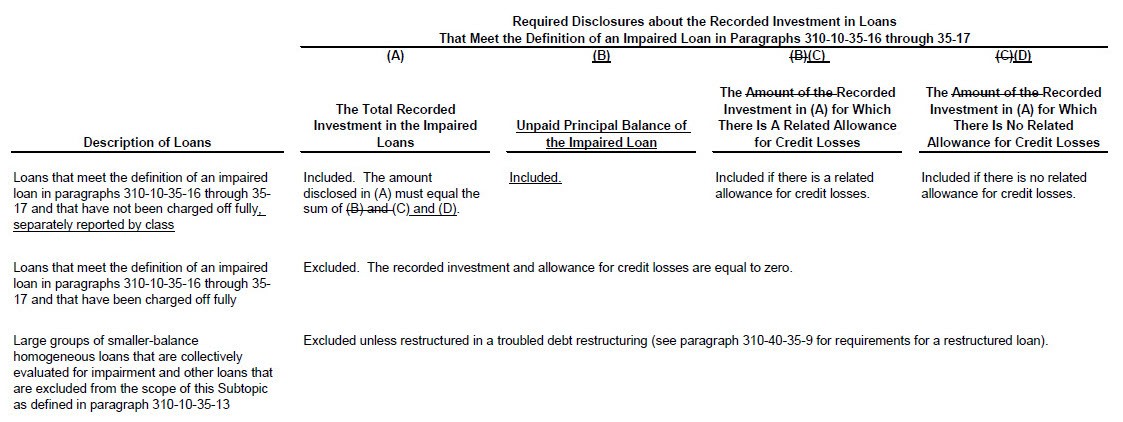

ImpairedFinancingReceivableUnpaidPrincipalBalance |

Impaired Financing Receivable, Unpaid Principal Balance |

The unpaid principal balance related to impaired financing receivables. |

310-10-50- 15(a)(2) |

ImpairedFinancingReceivableAverageRecordedInvestment |

Impaired Financing Receivable, Average Recorded Investment |

The average recorded investment related to impaired financing receivables. |

310-10-50- 15(c)(1); 310- 10-50-17 |

ImpairedFinancingReceivableRecordedInvestment |

Impaired Financing Receivable, Recorded Investment |

The recorded investment related to impaired financing receivables. |

310-10-50- 14A(b) |

ImpairedFinancingReceivableInterestIncomeAccrualMethod |

Impaired Financing Receivable, Interest Income, Accrual Method |

The interest income recognized during the time within that period that the financing receivables were impaired. |

310-10-50- 15(c)(2) |

ImpairedFinancingReceivableInterestIncomeCashBasisMethod |

Impaired Financing Receivable, Interest Income, Cash Basis Method |

The interest income recognized on a cash-basis method of accounting during the time within that period that the financing receivables were impaired. |

310-10-50- 15(c)(3) |

ImpairedFinancingReceivablePolicy |

Impaired Financing Receivable, Policy |

Represents the disclosure about the policy for recognizing interest income on impaired financing receivables, including how cash receipts are recorded, the policy for determining which loans the entity assesses for impairment, and the factors the creditor considered in determining that the financing receivable is impaired. |

310-10-50-14A(a); 310-10-50-15(b, d, e) |

FinancingReceivableModificationsTable |

Financing Receivable, Modifications |

Schedule detailing information related to troubled debt restructurings by type of financing receivable modification with further disaggregation by class of financing receivable and portfolio segment. |

310-10-50-32; 310-10-50-33 |

FinancingReceivableTroubledDebtRestructuringsAxis |

Financing Receivable, Troubled Debt Restructurings |

Information related to troubled debt restructurings granted in the current period by class of financing receivable and portfolio segment. |

310-10-50-32 |

FinancingReceivableTroubledDebtRestructuringsDomain |

Financing Receivable, Troubled Debt Restructurings |

Represents classes of financing receivables and portfolio segments related to troubled debt restructurings granted in the current period. |

310-10-50-32 |

FinancingReceivableTroubledDebtRestructuringsThatSubsequentlyDefaultedAxis |

Financing Receivable, Troubled Debt Restructurings That Subsequently Defaulted |

Information related to troubled debt restructurings within the last 12 months and for which there was a payment default in the current reporting period by class of financing receivable and portfolio segment. |

310-10-50-33 |

FinancingReceivableTroubledDebtRestructuringsThatSubsequentlyDefaultedDomain |

Financing Receivable, Troubled Debt Restructurings That Subsequently Defaulted |

Represents classes of financing receivables and portfolio segments related to troubled debt restructurings within the last twelve months and for which there was a payment default in the current reporting period. |

310-10-50-33 |

FinancingReceivableModificationsLineItems |

Financing Receivable, Modifications |

Line items represent financial concepts included in a table. These concepts are used to disclose reportable information associated with domain members defined in one or many axes to the table. |

|

FinancingReceivableModificationsNumberOfContracts |

Financing Receivable, Modifications, Number of Contracts |

The number of financing receivables that have been modified by troubled debt restructurings. |

310-10-50-32; 310-10-50-33 |

FinancingReceivableModificationsPreModificationRecordedInvestment |

Financing Receivable, Modifications, Pre-Modification Recorded Investment |

The amount of the outstanding recorded investment related to financing receivables that have been modified by troubled debt restructurings before the financing receivable has been modified. |

310-10-50-32; 310-10-50-33 |

FinancingReceivableModificationsPostModificationRecordedInvestment |

Financing Receivable, Modifications, Post-Modification Recorded Investment |

The amount of the outstanding recorded investment related to financing receivables that have been modified by troubled debt restructurings after the financing receivable has been modified. |

310-10-50-32; 310-10-50-33 |

FinancingReceivableModificationsRecordedInvestment |

Financing Receivable, Modifications, Recorded Investment |

The amount of the outstanding recorded investment related to financing receivables that have been modified by troubled debt restructurings. |

310-10-50-32; 310-10-50-33 |

FinancingReceivableModificationsNatureAndExtentOfTheTransaction |

Financing Receivable, Modifications, Nature and Extent of The Transaction |

Description of the nature and the extent of troubled debt restructurings related to financing receivables. |

310-10-50-32; 310-10-50-33 |

FinancingReceivableModificationsDeterminationOfTheAllowanceForCreditLosses |

Financing Receivable, Modifications, Determination of The Allowance for Credit Losses |

Description of the factors considered about how such troubled debt restructurings are factored into the determination of the allowance for credit losses. |

310-10-50-32; 310-10-50-33 |

LoansAndLeasesReceivableChargeOf fPolicy* |

Loans and Leases Receivable, Charge off, Policy |

Sets forth the basis for charging to bad debt expense all or a portion of loan receivables because it is probable, based on collection experience or on specific facts and circumstances, that collection of amounts due will not be made. For example, historical experience may indicate that amounts uncollected for a specified number of days after due date are likely to remain uncollected and some or all of the amounts due should be reflected as a credit loss. |

310-10; 310- 10-50-6(d) |

PremiumsReceivableAllowanceForDoubtfulAccountsWriteOffOfUncollectiblePremiumsPolicy* |

Premiums Receivable, Allowance for Doubtful Accounts, Write-off of Uncollectible Premiums, Policy |

Describes an insurance entity's accounting policy for determining when premium amounts due are determined to be not collectible and are removed from the general ledger, along with the related amount from the allowance for doubtful accounts (for example, customer bankruptcy). |

844-310; 235-10-50-3; 310-10-50-6(d) |

ProvisionForLeaseLosses* |

Provision for Lease Losses |

Allowance expense during the period based on estimated losses to be realized from lease transaction. |

942-225-S99-1; 310-10-50-12 |

ProvisionForLoanLossesExpensed* |

Provision for Loan Losses Expensed |

Allowance expensed for the period based on estimated losses to be realized from loan transactions. |

942-225-S99-1; 310-10-50- 12 |

ProvisionForLoanAndLeaseLosses* |

Provision for Loan and Lease Losses |

The sum of the periodic provision charged to operations, based on an assessment of the uncollectibility of the loan and lease portfolio, the offset to which is either added to or deducted from the allowance account for the purpose of reducing loan receivable and leases to an amount that approximates their net realizable value (the amount expected to be collected). |

230-10-45-28(a); 942-225-S99-1; 310-10-50-12 |

ProvisionForLoanLeaseAndOtherLosses* |

Provision for Loan, Lease, and Other Losses |

The sum of the periodic provision charged to earnings, based on an assessment of uncollectibility from the counterparty on account of loan, lease or other credit losses, to reduce these accounts to the amount that approximates their net realizable value. |

310-10-50-12; 230-10-45-28(a) |

LoansAndLeasesReceivableImpairedTroubledDebtRestructuringAmount* |

Loans and Leases Receivable, Impaired, Troubled Debt Restructuring, Amount |

Reflects the carrying amount of loans with terms that have been modified because of the inability of the borrower, for financial reasons, to comply with the terms of the original loan agreement. |

310-10-50-15(a); 310-40- 50-2 |

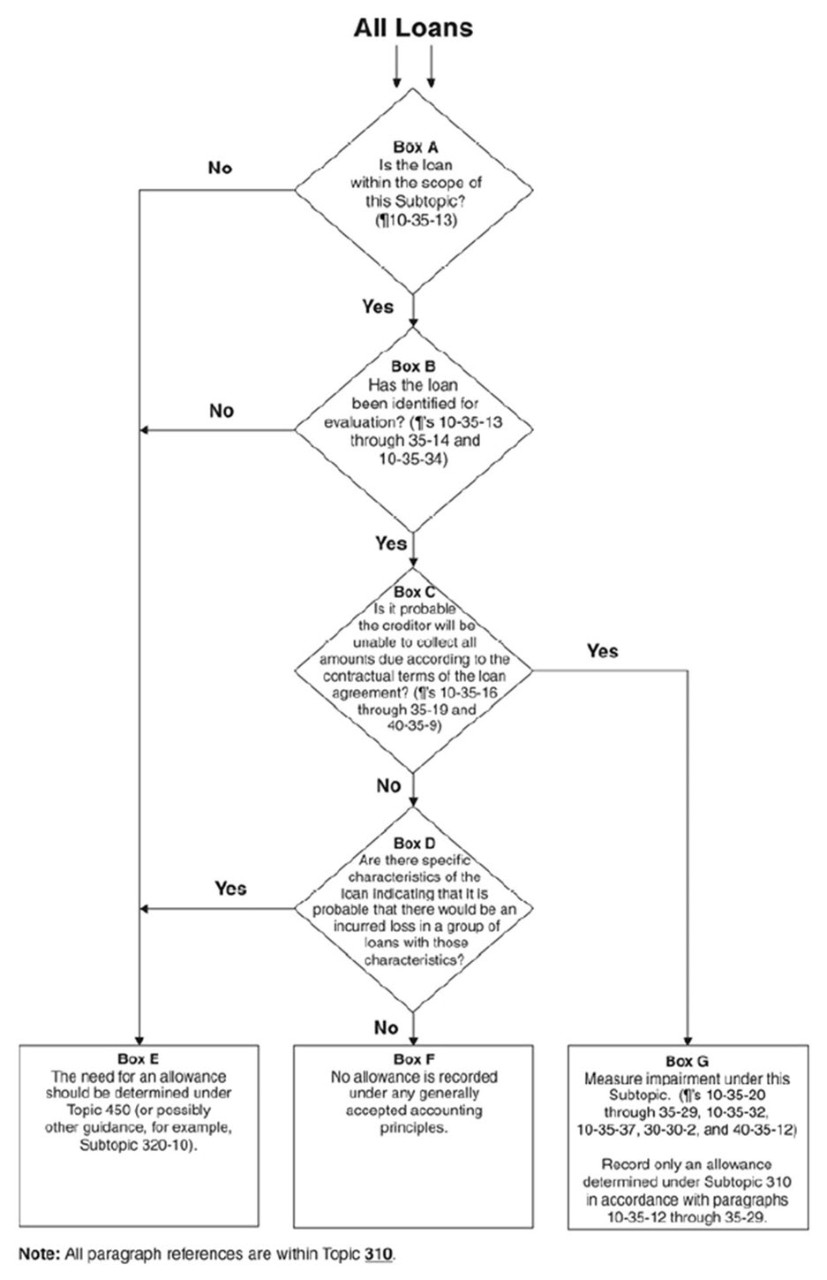

LoansAndLeasesReceivableImpairedAtCarryingValue* |

Loans and Leases Receivable, Impaired, at Carrying Value |

Reflects the adjusted carrying amount of loans for which it is probable, based on current facts and circumstances, that a creditor will not initially be able to collect all amounts due according to the contractual terms of the loan agreement, or will not recover the previously reported carrying amount of the loan. |

310-10-50- 15(a) |

LoansAndLeasesReceivableImpairedAllowanceForLoanLosses* |

Loans and Leases Receivable, Impaired, Allowance for Loan Losses |

Reflects amount of allowance for credit losses pertaining to impaired loans. |

310-10-50-15(a)(1) |

LoansAndLeasesReceivableImpairedEndOfPeriodInAllowanceForLoanLoss* |

Loans and Leases Receivable, Impaired, End of Period, in Allowance for Loan Loss |

Reflects the carrying amount of loans which have been written down and for which there is a related reserve for credit loss. |

310-10-50-15(a)(1) |

LoansAndLeasesReceivableImpairedEndOfPeriodNotInAllowanceForLoanLoss* |

Loans and Leases Receivable, Impaired, End of Period, Not in Allowance for Loan Loss |

Reflects the carrying amount of loans which have been written down and for which there is no related reserve for credit loss. |

310-10-50-15(a)(1) |

LoansAndLeasesReceivableImpairedDescription* |

Loans and Leases Receivable, Impaired, Description |

Describes the policies and procedures for identifying and measuring losses on loans when the present value of expected cash flows discounted at the loan's effective interest rate, or, alternatively, a loan's observable market price or fair value of the underlying collateral is less than the carrying amount of the loan, and sets forth the amount of the loss. Also sets forth material facts pertaining to significant loan modifications in a troubled debt restructuring, describes the method for valuing a loan deemed to be impaired or nonperforming, indicates whether income on impaired or nonperforming loans are being recognized and describes the method for recognizing the income. |

310-10-35-22; 310-10-50- 15(b); 235-10- 50-3 |

LoansAndLeasesReceivableImpairedAverageInvestment* |

Loans and Leases Receivable, Impaired, Average Investment |

Reflects the average recorded investment in impaired loans during each period. |

310-10-50-15(e) |

LoansAndLeasesReceivableImpairedInterestIncomeRecognized* |

Loans and Leases Receivable, Impaired, Interest Income Recognized |

Reflects the amount of interest income on impaired and nonperforming loans that was recognized as income during the reporting period. |

310-10-50-19; 310-10-50-15(e) |

LoansAndLeasesReceivableImpairedInterestIncomeCashBasisMethod* |

Loans and Leases Receivable, Impaired, Interest Income, Cash-Basis Method |

Reflects the amount of interest income recognized using a cash-basis method during the period that loans were deemed to be impaired. |

310-10-50-15(e) |

LoansAndLeasesReceivableImpairedNonperformingAccrualOfInterest |

Loans and Leases Receivable, Impaired, Nonperforming, Accrual of Interest |

Reflects the carrying amount of loans deemed to be questionable as to collection on which interest is continuing to be earned or accrued. |

|

LoansAndLeasesReceivableImpairedNonperformingOver90 DaysAccrualOfInterest |

Loans and Leases Receivable, Impaired, Nonperforming, over 90 Days, Accrual of Interest* |

Reflects the carrying amount of loans past due ninety days or more on which interest is continuing to be earned or accrued. |

310-10-50-7(b) |

LoansAndLeasesReceivableImpairedNonperformingNonaccrualOfInterest |

Loans and Leases Receivable, Impaired, Nonperforming, Nonaccrual of Interest* |

Reflects the carrying amount of loans deemed to be questionable as to collection on which no interest is continuing to be recognized. |

310-10-50-7(a) |

LoansAndLeasesReceivableImpairedInterestLostOnNonaccrualLoans |

Loans and Leases Receivable, Impaired, Interest Lost on Nonaccrual Loans* |

Reflects the amount of additional interest income that would have been recorded if impaired or nonperforming loans were instead current, in compliance with their original terms, and outstanding throughout the reporting period or since origination (if held for part of the period). |

|

LoansAndLeasesReceivableImpairedTroubledDebtInterestIncome |

Loans and Leases Receivable, Impaired, Troubled Debt, Interest Income* |

The gross interest income that would have been recorded in the period on troubled debt restructurings, if the loans had been current in accordance with their original terms and had been outstanding throughout the period or since origination, if held for part of the period. |

|

DiscontinuedOperationDescriptionOfMaterialContingentLiabilitiesRemaining* |

Discontinued Operation, Description of Material Contingent Liabilities Remaining |

Nature and amounts of material contingent liabilities, such as product or environmental liabilities or litigation, that remain with the entity despite the disposal of the disposal group that is classified as a component of the entity. Also includes any reasonably likely range of possible loss. |

450-20-50-6; 310-10-50-22; 450-20-50-3; 450-20-50-2; 450-20-50-5; 460-10-50-2; 450-20-50-1; 450-20-50-4; 205-20-S99-2; 310-10-50-21 |

Copyright #year# by Financial Accounting Foundation, Norwalk, Connecticut.

Select a section below and enter your search term, or to search all click ASU 2010-20—Receivables (Topic 310)