2. Amend paragraphs 220-10-45-14A and 220-10-45-17 and add paragraphs 220-10-45-17A through 45-17B and 220-10-45-18A through 45-18B, with a link to transition paragraph 220-10-65-3, as follows:

Comprehensive Income—Overall

Other Presentation Matters

> Presentation of Income Tax Effects

220-10-45-12 An entity shall present the amount of income tax expense or benefit allocated to each component of other comprehensive income, including reclassification adjustments, in the statement in which those components are presented or disclose it in the notes to the financial statements. Example 1 (see paragraphs 220-10-55-7 through 55-8B) illustrates the alternative formats for disclosing the tax effects related to the components of other comprehensive income.

> Reporting Accumulated Other Comprehensive Income

220-10-45-14 The total of other comprehensive income for a period shall be transferred to a component of equity that is presented separately from retained earnings and additional paid-in capital in a statement of financial position at the end of an accounting period. A descriptive title such as accumulated other comprehensive income shall be used for that component of equity.

220-10-45-14A An entity shall present,

either on the face of the financial statements or as a separate disclosure in the notes, the changes in the accumulated balances for each component of other comprehensive income included in that separate component of equity, as required in paragraph 220-10-45-14.

In addition to theThe

presentation of changes in accumulated balances, an entity shall present separately for each component of other comprehensive income, current period reclassifications out of accumulated other comprehensive income and other amounts of current-period other comprehensive income. Both before-tax and net-of-tax presentations are permitted provided the entity complies with the requirements in paragraph 220-10-45-12.correspond to the components of other comprehensive income in the statement in which other comprehensive income for the period is presented

. Paragraph 220-10-55-15 illustrates the disclosure of

changes in accumulated balances for components of other comprehensive income as a separate disclosure in the notes to financial statements.

> Reclassification Adjustments

220-10-45-17 An entity may present reclassification adjustments out of accumulated other comprehensive income on the face of the statement in which the components of other comprehensive income are presented, or it may disclose those reclassification adjustments in the notes to the financial statements. Therefore, for all classifications of other comprehensive income, an entity may use either a gross display on the face of the financial statement or a net display on the face of the financial statement and disclose the gross change in the notes to the financial statements. If displayed gross, reclassification adjustments are reported separately from other changes in the respective balance; thus, the total change is reported as two amounts. If displayed net, reclassification adjustments are combined with other changes in the other comprehensive income item balance; thus, the total change is reported as a single amount. Gross and net displays are illustrated in Example 1 (see paragraph 220-10-55-4). Cases A and B (see paragraphs 220-10-55-21 through 55-26) illustrate the calculation of reclassification adjustments for available-for sale equity and debt securities

.

An entity shall separately provide information about the effects on net income of significant amounts reclassified out of each component of accumulated other comprehensive income if those amounts all are required under other Topics to be reclassified to net income in their entirety in the same reporting period. An entity shall provide this information together, in one location, in either of the following ways:

- On the face of the statement where net income is presented

- As a separate disclosure in the notes to the financial statements.

The following paragraph describes the information requirements for presentation on the face of the statements where net income is presented, and paragraph 220-10-45-17B describes the information requirements for disclosure in the notes to the financial statements.

220-10-45-17A If an entity chooses to present information about the effects of significant amounts reclassified out of accumulated other comprehensive income on net income, on the face of the statement where net income is presented, the entity shall present parenthetically by component of other comprehensive income the effect of significant reclassification amounts on the respective line items of net income. An entity also shall present parenthetically the aggregate tax effect of all significant reclassifications on the line item for income tax benefit or expense in the statement where net income is presented. If an entity is unable to identify the line item of net income affected by any significant amount reclassified out of accumulated other comprehensive income in a reporting period (including when all reclassifications for the period are not to net income in their entirety), the entity must follow the guidance in the following paragraph. Paragraph 220-10-55-17F provides an example of presentation of the effect of reclassification on the face of the statement where net income is presented.

220-10-45-17B If an entity chooses to present information about significant amounts reclassified out of accumulated other comprehensive income in the notes to the financial statements or is required to do so by the preceding paragraph, it shall present the significant amounts by each component of accumulated other comprehensive income and provide a subtotal of each component of comprehensive income. The subtotals for each component shall agree with the requirements in paragraph 220-10-45-14A. Both before-tax and net-of-tax presentations are permitted provided the entity complies with the requirements in paragraph 220-10-45-12. For each significant reclassification amount, the entity shall identify, for those amounts that are required under other Topics to be reclassified to net income in their entirety in the same reporting period, each line item affected by the reclassification on the statement where net income is presented. For any significant reclassification for which other Topics do not require that reclassification to net income in its entirety in the same reporting period, the entity shall cross-reference to the note where additional details about the effect of the reclassifications are disclosed. Paragraph 220-10-55-17E provides an example of a note presentation in a tabular format of the effect of reclassifications out of accumulated other comprehensive income.

> Interim-Period Reporting

220-10-45-18 Subtopic 270-10 clarifies the application of accounting principles and reporting practices to interim financial information, including interim financial statements and summarized interim financial data of publicly traded companies issued for external reporting purposes. An entity shall report a total for comprehensive income in condensed financial statements of interim periods in a single continuous statement or in two consecutive statements.

220-10-45-18A {add glossary link to 1st definition}Publicly traded companies{add glossary link to 1st definition} must meet the reporting requirements in this Subtopic at each reporting period. Companies shall follow the guidance in Subtopic 270-10 for the level of detail required for condensed financial statements for interim-period financial statements.

220-10-45-18B {add glossary link to 1st definition}Nonpublic entities{add glossary link to 1st definition} must meet the reporting requirements in this Subtopic at each reporting period, except for the requirements in paragraphs 220-10-45-17 through 45-17B. Nonpublic entities are not required to meet the requirements in paragraphs 220-10-45-17 through 45-17B for interim reporting periods but are required to meet them for annual reporting periods.

3. Amend paragraph 220-10-55-15 and add paragraphs 220-10-55-15A through 55-15C and 220-10-55-17A through 55-17F and their related heading, with a link to transition paragraph 220-10-65-3, as follows:

Implementation Guidance and Illustrations

> Implementation Guidance

220-10-55-1 This Section provides Examples of reporting formats for comprehensive income, required disclosures, and a corresponding statement of financial position. The illustrations are intended as examples only. Other formats or levels of detail may be appropriate for certain circumstances. An entity is encouraged to provide information in ways that are most understandable to investors, lenders, and other external users of financial statements. For simplicity, the Examples provide information only for a single period; however, most entities are required to provide comparative financial statements. In addition to the Examples in this Section, paragraph 810-10-55-4C illustrates one method for reporting comprehensive income if the entity has one or more less-than-wholly-owned subsidiaries.

> Illustrations

> > Example 2: Presenting Accumulated Other Comprehensive Income

> > > Disclosure of Changes in Accumulated Other Comprehensive Income Balances

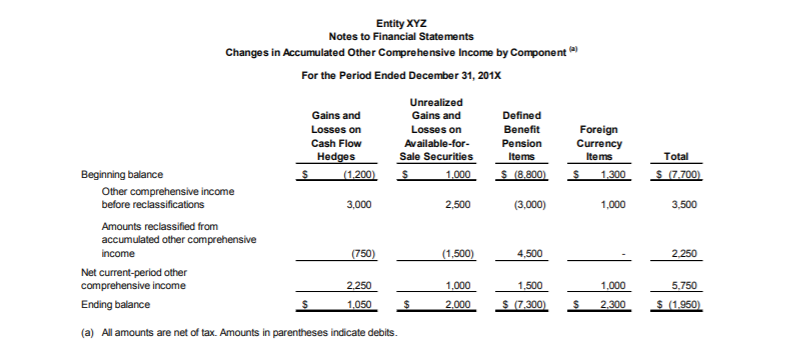

220-10-55-15 The following table illustrates

the disclosure disclosures in the notes to financial statements for the year ended December 31, 201X

, of changes in the balances of each component of accumulated

other comprehensive income, as

required bydiscussed

in paragraph 220-10-45-14A.

The amounts in this illustration correspond to the amounts in the Example in paragraph 220-10-55-17E and demonstrate the relationship between the requirements in paragraph 220-10-45-14A and the requirements in paragraph 220-10-45-17B for this entity.

View image

View image

[For ease of readability, this table is not underlined as new text.]

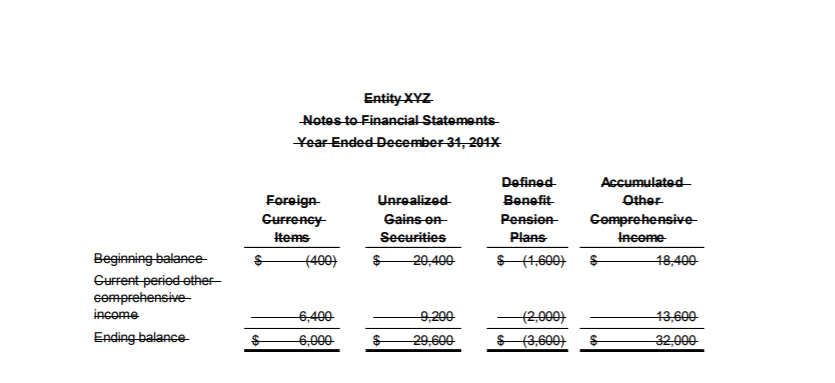

220-10-55-15A The following table illustrates the disclosure of changes in the balances of each component of accumulated other comprehensive income, as required by paragraph 220-10-45-14A. The amounts in this illustration correspond to the amounts in the Example in paragraph 220-10-55-17F.

[For ease of readability, this table is not underlined as new text.]

View image

View image

220-10-55-15B The presentation of unrealized gains and losses on available-for-sale securities illustrated in paragraphs 220-10-55-15 through 55-15A is aggregated for simplicity and, therefore, does not necessarily comply with all of the disclosures that may be required in Topic 320 (for example, disclosures about other-than-temporary-impairments in paragraph 320-10-45-9A).

220-10-55-15C For life insurers, amounts reclassified out of accumulated other comprehensive income exclude changes in unrealized gains and losses on available-for-sale securities associated with direct adjustments made to deferred acquisition costs, certain intangible assets, and policy liabilities necessary to reflect these balances as if such unrealized gains and losses were realized.

> > > Disclosure of Amounts Reclassified Out of Accumulated Other Comprehensive Income

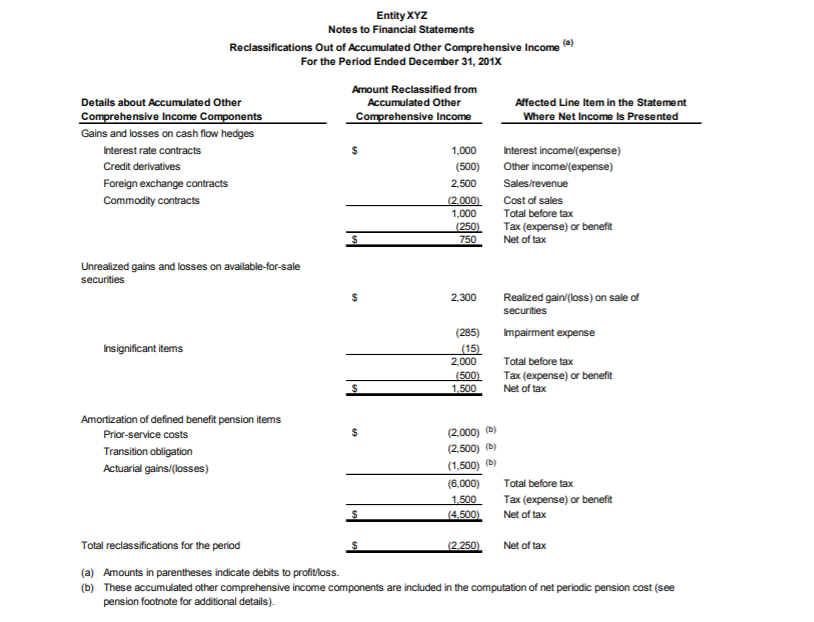

220-10-55-17A The effect of reclassifications on the line items in the statement in which net income is presented, as described in paragraph 220-10-45-17, should be presented on either a before-tax basis or a net-of-tax basis consistent with the entity’s method of presentation for the line items in the statement where net income is presented. In either case, the total for this disclosure should agree with the total amount of reclassifications for each component of comprehensive income that complies with the presentation requirements in paragraph 220-10-45-14A. The illustration in paragraph 220-10-55-17E presents the effect of reclassifications on the line items of net income on a before-tax basis, but it also shows totals for each component, which agree with the ending balances presented in paragraph 220-10-55-15, which is on an after-tax basis.

220-10-55-17B Topic 715 does not require an entity to reclassify the amortization of defined benefit pension and other employee benefit cost components from accumulated other comprehensive income directly to net income in their entirety. Rather, it requires an entity to reclassify those amortized costs in their entirety to net periodic pension cost. Some portion of net periodic pension cost is immediately reported in net income, but other portions may be capitalized to an asset balance such as fixed assets or inventory. An entity with significant defined benefit pension costs reclassified out of accumulated other comprehensive income but not to net income in its entirety in the same reporting period should identify the amount of each pension cost component reclassified out of accumulated other comprehensive income and make reference to the relevant pension cost disclosure that provides greater detail about these reclassifications.

220-10-55-17C A life insurer may make adjustments to unrealized gains and losses on available-for-sale securities for the effect on relevant assets and liabilities (as specified in paragraph 320-10-S99-2 for public entities) as if the unrealized gains and losses had been realized. In such cases, the life insurer should cross-reference to the related notes.

220-10-55-17D Some entities may not have a separate line item for realized gains/(losses) on the sale of securities and, instead, will include this amount as part of another line item, for example, other income/(expense).

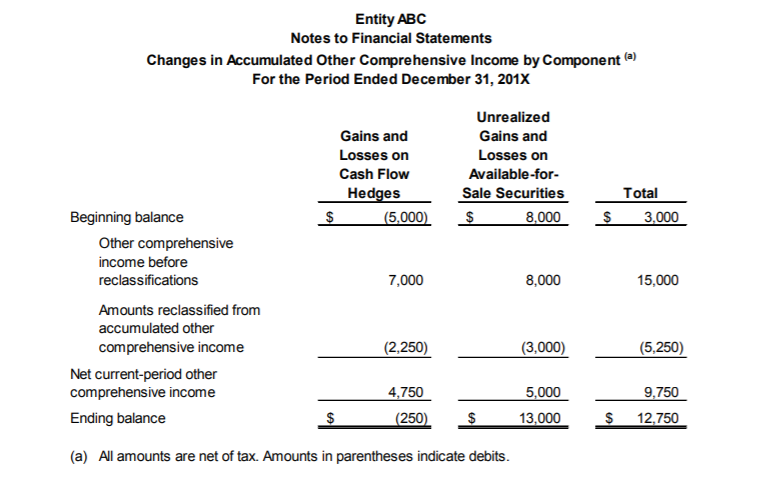

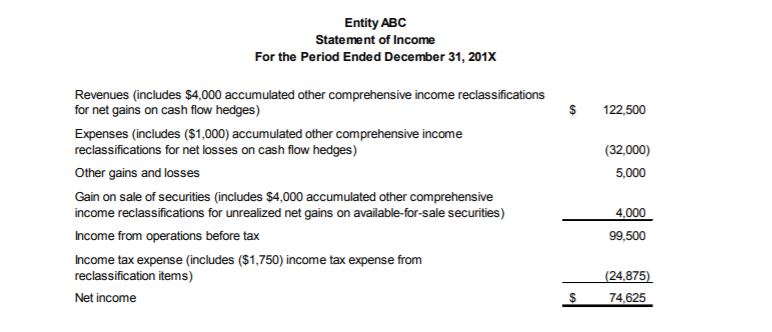

220-10-55-17E The following illustrates a disclosure in a tabular format of significant amounts reclassified out of each component of accumulated other comprehensive income, as required by paragraph 220-10-45-17B. The amounts used in this Example correspond to those in the Example in paragraph 220-10-55-15.

[For ease of readability, this table is not underlined as new text.]

View image

View image

220-10-55-17F The following illustrates presentation of the effect on certain line items of net income of significant amounts reclassified out of each component of accumulated other comprehensive income, as required by paragraph 220-10-45-17A. The amounts in this Example agree with the amounts in the Example in paragraph 220-10-55-15A. This presentation should only be used if all significant reclassifications out of accumulated other comprehensive income are reclassified to net income in their entirety in the same reporting period.

[For ease of readability, this illustration is not underlined as new text.]

View image

View image

4. Add paragraph 220-10-65-3 and its related heading as follows:

220-10-65-3 The following represents the transition and effective date information related to Accounting Standards Update No. 2013-02, Comprehensive Income (Topic 220): Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income:

- The pending content that links to this paragraph shall be applied prospectively and is effective as follows:

- For public entities, for fiscal years, and interim periods within those years, beginning after December 15, 2012.

- For {add glossary link to 1st definition}nonpublic entities{add glossary link to 1st definition}, for fiscal years beginning after December 15, 2013, and interim and annual periods thereafter.

- Early adoption of the pending content that links to this paragraph is permitted.

5. Amend paragraph 270-10-50-1 by adding item r, with a link to transition paragraph 220-10-65-3, as follows:

Interim Reporting—Overall

Disclosure

> Disclosure of Summarized Interim Financial Data by Publicly Traded Companies

270-10-50-1 Many publicly traded companies report summarized financial information at periodic interim dates in considerably less detail than that provided in annual financial statements. While this information provides more timely information than would result if complete financial statements were issued at the end of each interim period, the timeliness of presentation may be partially offset by a reduction in detail in the information provided. As a result, certain guides as to minimum disclosure are desirable. (It should be recognized that the minimum disclosures of summarized interim financial data required of publicly traded companies do not constitute a fair presentation of financial position and results of operations in conformity with generally accepted accounting principles [GAAP]). If publicly traded companies report summarized financial information at interim dates (including reports on fourth quarters), the following data should be reported, as a minimum:

r. The information about changes in accumulated other comprehensive income required by paragraphs 220-10-45-14A and 220-10-45-17 through 45-17B.

6. Amend paragraph 220-10-00-1, by adding the following items to the table, as follows:

220-10-00-1 The following table identifies the changes made to this Subtopic.

Paragraph Number |

Action |

Accounting Standards Update |

Date |

220-10-45-14A |

Amended |

2013-02 |

2/05/2013 |

220-10-45-17 |

Amended |

2013-02 |

2/05/2013 |

220-10-45-17A |

Added |

2013-02 |

2/05/2013 |

220-10-45-17B |

Added |

2013-02 |

2/05/2013 |

220-10-45-18A |

Added |

2013-02 |

2/05/2013 |

220-10-45-18B |

Added |

2013-02 |

2/05/2013 |

220-10-55-15 |

Amended |

2013-02 |

2/05/2013 |

220-10-55-15A through 55-15C |

Added |

2013-02 |

2/05/2013 |

220-10-55-17A through 55-17F |

Added |

2013-02 |

2/05/2013 |

220-10-65-3 |

Added |

2013-02 |

2/05/2013 |

7. Amend paragraph 270-10-00-1, by adding the following item to the table, as follows:

270-10-00-1 The following table identifies the changes made to this Subtopic.

Paragraph Number |

Action |

Accounting Standards Update |

Date |

270-10-50-1 |

Amended |

2013-02 |

2/05/2013 |

The amendments in this Update were adopted by the unanimous vote of the seven members of the Financial Accounting Standards Board:

Leslie F. Seidman, Chairman

Daryl E. Buck

Russell G. Golden

Thomas J. Linsmeier

R. Harold Schroeder

Marc A. Siegel

Lawrence W. Smith