Search within this section

Select a section below and enter your search term, or to search all click ASU 2016-20—Technical corrections and improvements to Topic 606, revenue from contracts with customers

Favorited Content

Area for Correction or Improvement |

Summary of Amendments |

Issue 1: Loan Guarantee Fees

Topic 606 specifically identifies a scope exception for guarantees (other than product or service warranties) within the scope of Topic 460, Guarantees. Stakeholders indicated that a few consequential amendments included in Update 2014-09 are inconsistent on whether fees from financial guarantees are within the scope of Topic 606.

|

The amendments in this Update clarify that guarantee fees within the scope of Topic 460 (other than product or service warranties) are not within the scope of Topic 606. Entities should see Topic 815, Derivatives and Hedging, for guarantees accounted for as derivatives. |

Issue 2: Contract Costs—Impairment Testing

Subtopic 340-40, Other Assets and Deferred Costs—Contracts with Customers, includes impairment guidance for costs capitalized in accordance with the recognition provisions of that Subtopic.

Stakeholders raised some questions about the impairment testing of those capitalized costs. |

The amendments in this Update clarify that when performing impairment testing an entity should (a) consider expected contract renewals and extensions and (b) include both the amount of consideration it already has received but has not recognized as revenue and the amount it expects to receive in the future. |

Issue 3: Contract Costs—Interaction of Impairment Testing with Guidance in Other Topics

Some stakeholders raised questions about the interaction of the impairment testing in Subtopic 340-40 with guidance in other Topics.

|

The amendments in this Update clarify that impairment testing first should be performed on assets not within the scope of Topic 340, Topic 350, Intangibles—Goodwill and Other, or Topic 360, Property, Plant, and Equipment (such as Topic 330, Inventory), then assets within the scope of Topic 340, then asset groups and reporting units within the scope of Topic 360 and Topic 350. |

Issue 4: Provisions for Losses on Construction-Type and ProductionType Contracts

When issuing Update 2014-09, the Board decided to exclude specific guidance in Topic 606 for onerous contracts. However, the Board decided to retain the guidance on the provision for loss contracts in Subtopic 605-35, Revenue Recognition—ConstructionType and Production-Type Contracts.

In the consequential amendments of Update 2014-09, the testing level was changed to the performance obligation level (from the segment level). Stakeholders indicated that this amendment, in some circumstances, may require an entity to perform the loss assessment at a lower level than current practice. |

The amendments in this Update require that the provision for losses be determined at least at the contract level. However, the amendments allow an entity to determine the provision for losses at the performance obligation level as an accounting policy election. |

Issue 5: Scope of Topic 606

In Topic 606, a scope exception exists for insurance contracts within the scope of Topic 944, Financial Services— Insurance. The Board's intention was to exclude from Topic 606 all contracts that are within the scope of Topic 944, not only insurance contracts (for example, investment contracts that do not subject an insurance entity to insurance risk).

|

The amendments in this Update remove the term insurance from the scope exception to clarify that all contracts within the scope of Topic 944 are excluded from the scope of Topic 606. |

Issue 6: Disclosure of Remaining Performance Obligations

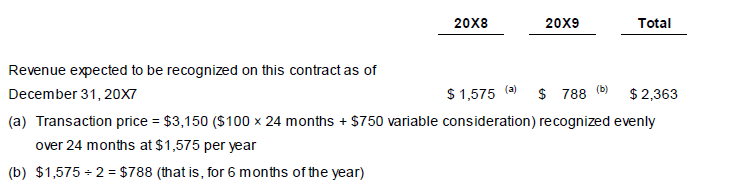

Topic 606 requires an entity to disclose information about its remaining performance obligations, including the aggregate amount of the transaction price allocated to performance obligations that are unsatisfied (or partially unsatisfied) as of the end of the reporting period. Topic 606 also includes optional exemptions from that disclosure for contracts with an original duration of one year or less and performance obligations in which revenue is recognized in accordance with paragraph 606-10-55-18. Stakeholders questioned whether the Board intended for an entity to estimate variable consideration for disclosure in other circumstances in which an entity is not required to estimate variable consideration to recognize revenue.

|

The amendments in this Update provide optional exemptions from the disclosure requirement for remaining performance obligations for specific situations in which an entity need not estimate variable consideration to recognize revenue.

The amendments in this Update also expand the information that is required to be disclosed when an entity applies one of the optional exemptions.

|

Issue 7: Disclosure of Prior-Period Performance Obligations

Topic 606 requires an entity to disclose revenue recognized in the reporting period from performance obligations satisfied (or partially satisfied) in previous periods. Stakeholders indicated that the placement of the disclosure in the Codification results in confusion about whether this disclosure applies only to performance obligations with corresponding contract balances or to all performance obligations.

|

The amendments in this Update clarify that the disclosure of revenue recognized from performance obligations satisfied (or partially satisfied) in previous periods applies to all performance obligations and is not limited to performance obligations with corresponding contract balances. |

Issue 8: Contract Modifications Example

Example 7 in Topic 606 illustrates the application of the guidance on contract modifications. Some stakeholders perceived minor inconsistencies with the contract modifications guidance in Topic 606.

|

The amendments in this Update better align Example 7 with the principles in Topic 606. |

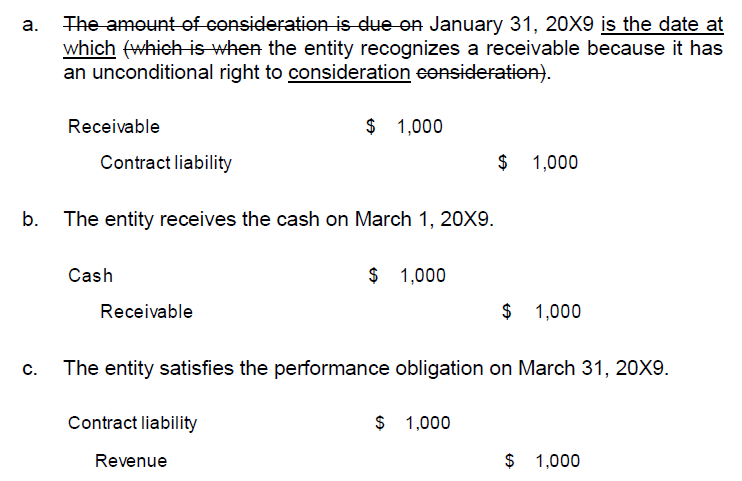

Issue 9: Contract Asset versus Receivable

Example 38, Case B in Topic 606 illustrates the application of the presentation guidance on contract assets and receivables. Some stakeholders expressed concern that the example indicates that an entity cannot record a receivable before its due date.

|

The amendments in this Update provide a better link between the analysis in Example 38, Case B and the receivables presentation guidance in Topic 606. |

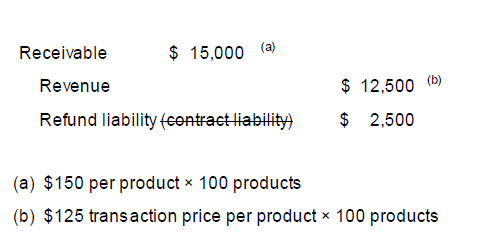

Issue 10: Refund Liability

Example 40 in Topic 606 illustrates the recognition of a receivable and a refund liability. Some stakeholders expressed concern that the example indicates that a refund liability should be characterized as a contract liability.

|

The amendment in this Update removes the reference to the term contract liability from the journal entry in Example 40. |

Issue 11: Advertising Costs

Update 2014-09 supersedes much of the guidance in Subtopic 340-20, Other Assets and Deferred Costs— Capitalized Advertising Costs, because it would have conflicted with new cost capitalization guidance in Subtopic 340-40. Therefore, an entity that previously capitalized advertising costs in accordance with the guidance in Subtopic 340-20 would apply the capitalization guidance in Subtopic 340-40 upon the adoption of Update 201409. Guidance on when to recognize a liability had been included within Subtopic 340-20 and was inadvertently superseded by Update 2014-09.

|

The amendments in this Update reinstate the guidance on the accrual of advertising costs and also move the guidance to Topic 720, Other Expenses. |

Issue 12: Fixed-Odds Wagering Contracts in the Casino Industry

Subtopic 924-605, Entertainment— Casinos—Revenue Recognition, currently includes explicit guidance that identifies fixed-odds wagering as gaming revenue. That industry-specific guidance was superseded by Update 2014-09, along with nearly all existing industry-specific revenue guidance in GAAP. Therefore, some stakeholders questioned whether fixed-odds wagering contracts are within the scope of Topic 606 or, rather, whether they should be accounted for as derivatives within the scope of Topic 815.

|

The amendments in this Update (a) create a new Subtopic 924-815, Entertainment—Casinos— Derivatives and Hedging, which includes a scope exception from derivatives guidance for fixed odds wagering contracts and (b) includes a scope exception within Topic 815 for fixed-odds wagering contracts issued by casino entities. |

Issue 13: Cost Capitalization for Advisors to Private Funds and Public Funds

A consequential amendment included in Update 2014-09 moved cost guidance from Subtopic 946-605, Financial Services—Investment Companies—Revenue Recognition, to Subtopic 946-720, Financial Services— Investment Companies—Other Expenses. This amendment was intended to move the guidance only and was not intended to change practice. However, the consequential amendment in Update 2014-09 could have resulted in inconsistent accounting for offering costs among advisors to public funds and private funds.

|

The amendments in this Update align the cost-capitalization guidance for advisors to both public funds and private funds in Topic 946. |

Paragraph |

Action |

Accounting Standards Update |

Date |

270-10-50-1A |

Amended |

2016-20 |

12/21/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

310-10-60-4 |

Amended |

2016-20 |

12/21/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

340-40-35-3 through 35-5 |

Amended |

2016-20 |

12/21/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

605-35-25-47 |

Amended |

2016-20 |

12/21/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

606-10-15-2 |

Amended |

2016-20 |

12/21/2016 |

606-10-50-8 |

Amended |

2016-20 |

12/21/2016 |

606-10-50-12A |

Added |

2016-20 |

12/21/2016 |

606-10-50-14 |

Amended |

2016-20 |

12/21/2016 |

606-10-50-14A |

Added |

2016-20 |

12/21/2016 |

606-10-50-14B |

Added |

2016-20 |

12/21/2016 |

606-10-50-15 |

Amended |

2016-20 |

12/21/2016 |

606-10-55-125 |

Amended |

2016-20 |

12/21/2016 |

606-10-55-127 |

Amended |

2016-20 |

12/21/2016 |

606-10-55-128 |

Amended |

2016-20 |

12/21/2016 |

606-10-55-285 |

Amended |

2016-20 |

12/21/2016 |

606-10-55-286 |

Amended |

2016-20 |

12/21/2016 |

606-10-55-293 |

Amended |

2016-20 |

12/21/2016 |

606-10-55-300 |

Amended |

2016-20 |

12/21/2016 |

606-10-55-305A |

Added |

2016-20 |

12/21/2016 |

606-10-65-1 |

Amended |

2016-20 |

12/21/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

720-35-05-1 |

Amended |

2016-20 |

12/21/2016 |

720-35-15-5 |

Added |

2016-20 |

12/21/2016 |

720-35-25-1A |

Added |

2016-20 |

12/21/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

815-10-15-13 |

Amended |

2016-20 |

12/21/2016 |

815-10-15-82A |

Added |

2016-20 |

12/21/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

924-10-05-1 |

Amended |

2016-20 |

12/21/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

924-815-05-1 |

Added |

2016-20 |

12/21/2016 |

924-815-15-1 |

Added |

2016-20 |

12/21/2016 |

924-815-25-1 |

Added |

2016-20 |

12/21/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

942-825-50-2 |

Amended |

2016-20 |

12/21/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

946-720-25-3 |

Amended |

2016-20 |

12/21/2016 |

946-720-25-4 |

Amended |

2016-20 |

12/21/2016 |

Copyright #year# by Financial Accounting Foundation, Norwalk, Connecticut.

Select a section below and enter your search term, or to search all click ASU 2016-20—Technical corrections and improvements to Topic 606, revenue from contracts with customers