4. Add paragraphs 958-605-15-2A, 958-605-15-5A, 958-605-15-7A, 958-605-25-2A, 958-605-25-5A through 25-5F and the related heading, and 958-605-45-4A through 45-4B and their related heading, amend paragraphs 958-605-15-4 through 15-6, 958-605-25-1 through 25-2, 958-605-25-11, 958-605-25-13, and 958-605-45-4, and supersede paragraphs 958-605-25-12 and 958-605-25-14, with a link to transition paragraph 958-10-65-2, as follows:

Not-for-Profit Entities—Revenue Recognition—Contributions

Scope and Scope Exceptions

General

>Overall Guidance

958-605-15-1 This Subtopic follows the same Scope and Scope Exceptions as outlined in the Overall Subtopic, see Section 958-10-15.

958-605-15-2 The General Subsection of this Section establishes the pervasive scope for this Subtopic, with specific exceptions noted in the other Subsections of this Section.

958-605-15-2A A business entity shall consider the guidance in this Subtopic when determining whether a transaction is a contribution within the scope of this Subtopic. Additionally, paragraphs 958-605-55-4 through 55-7 and 958-605-55-13A through 55-14I apply to all resource providers, including business entities that act as resource providers.

Contributions Received

>Entities

958-605-15-4 Accounting for contributions is an issue primarily for not-for-profit entities (NFPs) because contributions received are a significant source of revenues for many of those entities. However, except for Section 958-605-45, the guidance in the Contributions Received Subsections applies to all entities (NFPs and business entities) that receive contributions unless otherwise indicated.

>Transactions

958-605-15-5 The guidance in the Contributions Received Subsections applies to the following transactions and activities:

a. Contributions of cash and other assets, including promises to give, or a reduction, settlement, or cancellation of liabilities.

958-605-15-5A In determining whether a transfer of assets is an exchange transaction in which a resource provider (for example, a government agency, a foundation, a corporation, or other entity) receives commensurate value in return for the resources transferred or a contribution, the type of resource provider shall not factor into the determination and an entity shall evaluate the terms of an agreement and consider the following (additional clarification is provided in paragraphs 958-605-55-4 through 55-7 and 958-605-55-13A through 55-14I):

a. The resource provider (including a foundation, a government agency, a corporation, or other entity) is not synonymous with the general public. A benefit received by the public as a result of the assets transferred is not equivalent to commensurate value received by the resource provider. Therefore, if the resource provider receives indirect value in exchange for the assets transferred or if the value received by the resource provider is incidental to the potential public benefit from using the assets transferred, the transaction shall not be considered commensurate value received in return.

b. Execution of the resource provider’s mission or the positive sentiment from acting as a donor shall not constitute commensurate value received by the resource provider for purposes of determining whether the transfer of assets is a contribution or an exchange.

c. If the expressed intent asserted by both the recipient and the resource provider is to exchange resources for goods or services that are of commensurate value, the transaction shall be indicative of an exchange transaction. The transaction shall be indicative of a contribution if the recipient solicits assets from the resource provider without the intent of exchanging goods or services of commensurate value.

d. If the resource provider has full discretion in determining the amount of the transferred assets, the transaction shall be indicative of a contribution. If both the recipient and the resource provider agree on the amount of assets transferred in exchange for goods and services that are of commensurate value, the transaction shall be indicative of an exchange transaction.

e. If the penalties assessed on the recipient for failure to comply with the terms of the agreement are limited to the delivery of assets or services already provided and the return of the unspent amount, the transaction is generally indicative of a contribution. The existence of contractual provisions for economic forfeiture beyond the amount of assets transferred by the resource provider to penalize the recipient for nonperformance generally indicates that the transaction is an exchange of commensurate value.

958-605-15-6 The guidance in the Contributions Received Subsections does not apply to the following transactions and activities:

a. Transfers of assets that are in substance purchases of goods or services—exchange transactions in which each party receives and sacrifices commensurate value (in accordance with the guidance in paragraph 958-605-15-5A). However, if an entity voluntarily transfers assets to another or performs services for another in exchange for assets of substantially lower value and no unstated rights or privileges are involved, the contribution received that is inherent in that transaction is within the scope of the Contributions Received Subsections.

b. Transfers of assets in which the reporting entity acts as an

agent,

trustee, or

intermediary, rather than as a donor or donee (see the Transfers of Assets to a Not-for-Profit Entity or Charitable Trust That Raises or Holds Contributions for Others Subsections of

thisThis

Subtopic).

c. Tax exemptions, tax incentives, or tax abatements.

d. Transfers of assets from

governmental units

government entities to business entities.

e. Transfers of assets (typically from a government entity) that are part of an existing exchange transaction between a recipient and an identified customer. Some examples include payments under Medicare and Medicaid programs, provisions of health care or education services by a government for its employees, and Pell Grants or similar state or local government tuition assistance programs. In those instances, an entity shall apply the applicable guidance (for example, Topic 606 on revenue from contracts with customers) to the underlying transaction with the customer, and the payments from the third parties would be payments on behalf of those customers.

958-605-15-7A Contribution revenue within the scope of this Subtopic can be presented in the financial statements of an entity using different terms (for example, gift, grant, donation, or other terms). While some of those terms are generally not used in this guidance, the term used in the presentation of financial statements to label revenue that is accounted for within the scope of this Subtopic is not a factor in determining whether an agreement is within the scope of this Subtopic.

Recognition

General

958-605-25-1 Exchange transactions shall be accounted for in accordance with other applicable Topics, such as Topic 606 on revenue from contracts with customers.

Contributions Received

958-605-25-2 Except as provided in paragraphs 958-605-25-16 through

25-18

25-19 (related to contributed services, works of art, historical treasures, and similar items), contributions received shall be recognized as revenues or gains in the period received and as assets, decreases of liabilities, or expenses depending on the form of the benefits received. The classification of contributions received as revenues or gains depends on whether the transactions are part of the NFP’s ongoing major or central activities (revenues), or are peripheral or incidental to the NFP (gains). A contribution made and a corresponding contribution received generally are recognized by both the donor and the donee at the same time, that is,

when made or received, respectively, or if conditional, when the barrier is overcome upon occurrence of the underlying event—the nonreciprocal transfer of an economic benefit.

The definition of a contribution encompasses both a transfer of cash or other assets to an entity and a reduction, settlement, or cancellation of its liabilities.

958-605-25-2A After a contribution has been deemed not to contain a donor-imposed condition (see paragraphs 958-605-25-5A through 25-5F), an entity shall consider whether the contribution includes a donor-imposed restriction, which includes the consideration about how broad or narrow the purpose of the agreement is and whether the resources can be used only after a specified date.

958-605-25-5A A donor-imposed condition must have both:

a. One or more barriers that must be overcome before a recipient is entitled to the assets transferred or promised

b. A right of return to the contributor for assets transferred (or for a reduction, settlement, or cancellation of liabilities) or a right of release of the promisor from its obligation to transfer assets (or reduce, settle, or cancel liabilities).

958-605-25-5B For a donor-imposed condition to exist, it must be determinable from the agreement (or another document referenced in the agreement) that a recipient is only entitled to the transferred assets or a future transfer of assets if it has overcome the barrier. An agreement does not need to include the specific phrase right of return or release from obligation; however, an agreement should be sufficiently clear to be able to support a reasonable conclusion about when a recipient would be entitled to the transfer of assets. In the absence of any apparent indication that a recipient is only entitled to the transferred assets or a future transfer of assets if it has overcome a barrier, the agreement shall not be considered to contain a right of return of assets transferred or a right of release from obligation and shall be deemed a contribution without donor-imposed conditions.

>Barrier

958-605-25-5C An entity must evaluate the facts and circumstances of an agreement to determine whether a stipulation represents a barrier that must be overcome before the recipient is entitled to the assets transferred or promised. A barrier often places specific requirements on an organization about the use of the transferred assets to be entitled to those assets. A probability assessment about whether the recipient is likely to meet the stipulation is not a factor when determining whether an agreement contains a barrier. In cases of ambiguous donor stipulations, see paragraph 958-605-25-5E.

958-605-25-5D The following table contains a list of indicators that may be helpful in determining whether an agreement contains a barrier. Depending on the facts and circumstances, some indicators may be more significant than others, and no single indicator shall be determinative. See paragraphs 958-605-55-17A through 55-17F and 958-605-55-70A through 55-70T for implementation guidance and illustrative examples on determining whether a contribution is conditional.

|

Measurable Performance-Related Barrier or Other Measurable Barrier |

The agreement includes a measurable performance-related barrier or other measurable barrier.

Measurable performance-related barriers or other measurable barriers often are coupled with a time limitation (for example,indicating that the outcomes are to-be achieved within a specified time frame).

Examples of measurable performance-related barriers include a requirement that indicates that a recipient's entitlement to transferred assets is contingent upon the achievement of any of the following:

a. A specified level of service

b. An identified number of units of output

c. A specific outcome.

Other measurable barriers stipulate that a recipient is entitled to the resources if an identified event occurs (for example, a matching requirement).

|

Limited Discretion by the Recipient on the Conduct of an Activity |

The recipient has limited discretion over the manner in which activity can be conducted. Limited discretion of the recipient is more specific than a donor-imposed restriction. Restrictions limit the use of a contribution to a specific activity or time but do not necessarily place limitations on how the activity is performed. Examples of limited discretion could include a requirement to follow specific guidelines about incurring qualifying expenses, a requirement to hire specific individuals as part of the workforce conducting the activity (such as the hiring of specified employees or an identified professor at a university), and a specific protocol that must be adhered to. |

Stipulations That Are Related to the Purpose of the Agreement |

The stipulations are related to the purpose of the agreement. Examples could include a requirement for (a) a homeless shelter to provide a specified number of meals to the homeless (also an example of a measurable performance-related barrier), (b) an animal shelter to expand its facility to accommodate a specified number of additional animals, and (c) a research report that summarizes the findings from a grant on gluten-related allergies.

A stipulation that is unrelated to the purpose of the agreement (for example, administrative and trivial stipulations) is not indicative of a barrier.

Administrative and trivial stipulations could include routine reporting such as a requirement to provide (a) an annual report or (b) a report that summarizes the recipient's performance to demonstrate the underlying actions that were taken to meet the barrier(s) specified in the agreement.

For example, a report that indicates the number of meals that a homeless shelter provided to the homeless is typically not a stipulation that would contribute to achieving the purpose of the agreement. Rather, the action of providing a specified number of meals to the homeless would meet the stipulation that is required by a recipient to achieve the purpose of the agreement.

|

958-605-25-5E Determining whether a

contributionpromise

is conditional

or unconditional

can be difficult if it contains donor stipulations that do not clearly state whether

both:

a. One or more barriers exist

b.

the

The right to receive

or retain payment or delivery of the promised assets depends on meeting those

stipulations

barriers.

It may be difficult to determine whether those stipulations are conditions or restrictions.

In cases of ambiguous donor stipulations, a

contributionpromise

containing stipulations that are not clearly unconditional shall be presumed to be a

conditional contribution conditional promise

.

[Content amended as shown and moved from paragraph 958-605-25-14]

958-605-25-5F A transfer of assets

that is a conditional contribution with a conditional promise to contribute them

shall be accounted for as a refundable advance until the conditions have been substantially met or explicitly waived by the donor.

Some entities transfer cash or other assets with both donor-imposed restrictions and stipulations that impose a condition on which a gift depends. If a restriction and a condition exist, the transfer shall be accounted for as a refundable advance until the condition on which it depends is substantially met.

[Content amended as shown and moved from paragraph 958-605-25-13]

> Promises to Give

> > Conditional Promise to Give

958-605-25-11 {add glossary link}Conditional promises to give

{add glossary link}, which

depend on the occurrence of a specified future and uncertain event to bind the promisor

contain donor-imposed conditions that represent a barrier that must be overcome as well as a right of release from obligation, shall be recognized when the

condition or conditions on which they depend are substantially met, that is, when the conditional promise becomes unconditional. Imposing a condition creates a barrier that must be overcome before the recipient

of the transferred assets has an unconditional right to retain those promised

is entitled to the assets

promised. For example, a

transfer of cash with a

promise to contribute that cash if a like amount of new gifts are raised from others within 30 days and a provision that the cash

will not be

transferredreturned

if the gifts are not raised

imposes

mpose a condition on which

entitlement to a promised gift depends.

958-605-25-12 Paragraph superseded by Accounting Standards Update No. 2018-08. A conditional promise to give is considered unconditional if the possibility that the condition will not be met is remote. See paragraph 958-605-55-16 for examples of conditions that are remote of occurrence.

958-605-25-13 A transfer of assets with a conditional promise to contribute them shall be accounted for as a refundable advance until the conditions have been substantially met or explicitly waived by the donor. Some entities transfer cash or other assets with both donor-imposed restrictions and stipulations that impose a condition on which a gift depends. If a restriction and a condition exist, the transfer shall be accounted for as a refundable advance until the condition on which it depends is substantially met.

[Content amended and moved to paragraph 958-605-25-5F] A transfer of assets after a conditional promise to give is made and before the conditions are met is the same as a transfer of assets

that is a conditional contribution (see paragraph 958-605-25-5F) with a conditional promise to contribute those assets.

A change in the original conditions of the agreement between promisor and promisee shall not be implied without an explicit waiver (see paragraph 958-605-35-2).

> > Determining Whether a Promise Is Conditional or Unconditional

958-605-25-14 Paragraph superseded by Accounting Standards Update No. 2018-08. Determining whether a promise is conditional or unconditional can be difficult if it contains donor stipulations that do not clearly state whether the right to receive payment or delivery of the promised assets depends on meeting those stipulations. It may be difficult to determine whether those stipulations are conditions or restrictions. In cases of ambiguous donor stipulations, a promise containing stipulations that are not clearly unconditional shall be presumed to be a conditional promise.

[Content amended and moved to paragraph 958-605-25-5E]

958-605-25-15 Absence of a specified time for transfer of cash or other assets, by itself, does not necessarily lead to a determination that a promise to give is ambiguous. If the parties fail to express the time or place of performance and performance is unconditional, performance within a reasonable time after making a promise is an appropriate expectation; similarly, if a promise is conditional, performance within a reasonable time after fulfilling the condition is an appropriate expectation. Promises to give that are silent about payment terms but otherwise are clearly unconditional shall be accounted for as unconditional promises to give.

Other Presentation Matters

Contributions Received

958-605-45-4 A restriction on an NFP's use of the assets contributed results either from a donor's explicit

stipulation or from circumstances surrounding the receipt of the contribution that make clear the donor's implicit restriction on use.

Donor restricted contributions whose restrictions are met in the same reporting period may be reported as support within net assets without donor restrictions provided that an NFP has a similar policy for reporting investment gains and income (see paragraph 958-220-45-24), reports consistently from period to period, and discloses its accounting policy.

[Content amended and moved to paragraph 958-605-45-4A]

> Simultaneous Release Option

958-605-45-4A An NFP may elect a policy to report donor-restrictedDonor restricted

contributions whose restrictions some are met in the same reporting period

as the revenue is recognized may be reported

as support within net assets without donor restrictions provided that

an

the NFP has a similar policy for reporting investment gains and income (see paragraph 958-220-45-24), reports consistently from period to period, and discloses its accounting policy.

[Content amended as shown and moved from paragraph 958-605-45-4]

958-605-45-4B An NFP may elect the policy described in paragraph 958-605-45-4A for donor-restricted contributions that were initially conditional contributions (the condition has been met) without also having to elect it for other donor restricted contributions or investment gains and income provided that the NFP reports consistently from period to period and discloses its accounting policy.

5. Add paragraphs 958-605-55-1A, 958-605-55-3A, 958-605-55-13A and its related heading, 958-605-55-14A through 55-14I and their related headings, 958-605-55-17A through 55-17F and their related headings, and 958-605-55-70A through 55-70T and their related headings, amend paragraphs 958-605-55-2A, 958-605-55-4, 958-605-55-7, 958-605-55-14 and its related heading, 958-605-5515 through 55-17, 958-605-55-21, and 958-605-55-51, and supersede paragraphs 958-605-55-3, 958-605-55-8, and 958-605-55-82 and its related heading, with a link to transition paragraph 958-10-65-2, as follows:

Implementation Guidance and Illustrations

General

> Implementation Guidance

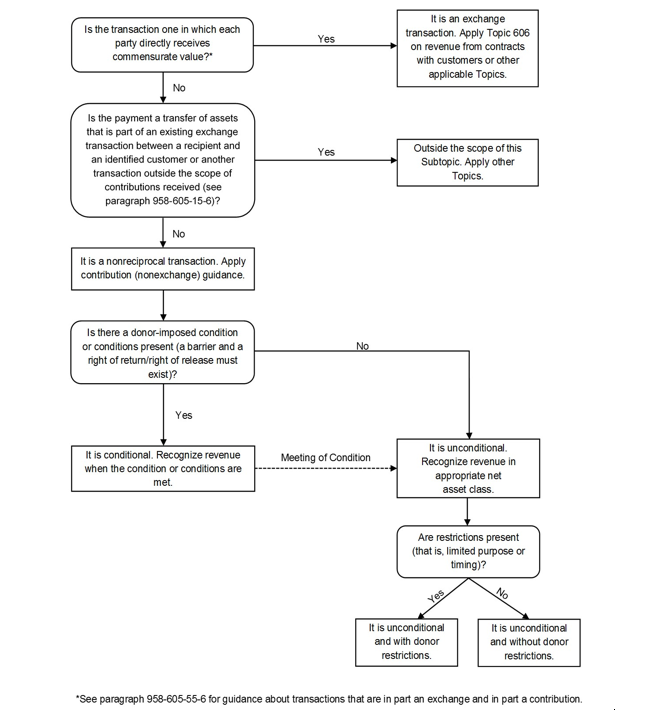

958-605-55-1A The following diagram illustrates the process for determining whether a transfer of assets to a recipient is a contribution, an exchange transaction, or another type of transaction and whether a contribution is conditional. The diagram also illustrates whether there is an associated donor restriction with a contribution.

[For ease of readability, the new diagram is not underlined.]

958-605-55-2 The accounting and reporting of grants, membership dues, and sponsorships is determined by the underlying substance of the transaction. Those terms are broadly used to refer not only to contributions but also to assets transferred in exchange transactions. A grant, sponsorship, or membership may be entirely a contribution, entirely an exchange, or a combination of the two; therefore, care must be taken in evaluating each grant, sponsorship, or membership agreement. In addition, those resource transfers may also have the characteristics of agency transactions.

958-605-55-2A The implementation guidance is organized as follows:

a. Distinguishing contributions from exchange transactions (see paragraphs

958-605-55-3

958-605-55-3A through

55-7 55-8

)

b. Distinguishing the contribution portion of membership dues (see paragraphs 958-605-55-9 through 55-12)

c. Distinguishing contributions from agency transactions (see paragraph 958-605-55-13).

> > Distinguishing Contributions from Exchange Transactions

958-605-55-3 Paragraph superseded by Accounting Standards Update No. 201808. Some transfers of assets that are exchange transactions may appear to be contributions if the services or other assets given in exchange are perceived to be a sacrifice of little value and the exchanges are compatible with the recipient's mission.

958-605-55-3A The guidance in this Subtopic about distinguishing between contributions and exchange transactions applies to both a resource provider (for example, a corporate foundation, a corporation, or a not-for-profit entity [NFP]) and a recipient.

958-605-55-4 Foundations, business entities, and other types of entities may provide resources to

not-for-profit entities (NFPs)

NFPs or business entities under programs referred to as grants, awards, or sponsorships. Those asset transfers are contributions if the resource providers

do not receive

commensurateno value in exchange for the assets transferred or if the value received by the resource providers is incidental to the potential public benefit from using the assets transferred. A grant made by a resource provider to

an a not-for-profit entity (NFP)

NFP would likely be a contribution if the activity specified by the grant is to be planned and carried out by the NFP and the NFP has the right to the benefits of carrying out the activity. If, however, the grant is made by a resource provider that provides materials to be tested in the activity and that retains the right to any patents or other results of the activity, the grant would likely be an exchange transaction. A careful assessment of the characteristics of the transaction, from the perspectives of both the resource provider and the recipient, is necessary to determine whether a contribution has occurred.

958-605-55-5 For example, a resource provider may sponsor research and development activities at a research university and retain proprietary rights or other privileges, such as patents, copyrights, or advance and exclusive knowledge of the research outcomes. The research outcomes may be intangible, uncertain, or difficult to measure, and may be perceived by the university as a sacrifice of little or no value; however, their value often is commensurate with the value that a resource provider expects in exchange. Similarly, a resource provider may sponsor research and development activities and specify the protocol of the testing so the research outcomes are particularly valuable to the resource provider. Those transactions are not contributions if their potential public benefits are secondary to the potential proprietary benefits to the resource providers.

958-605-55-6 Moreover, a single transaction may be in part an exchange and in part a contribution. For example, if a donor transfers a building to an entity at a price significantly lower than its fair value and no unstated rights or privileges are involved, the transaction is in part an exchange of assets and in part a contribution to be accounted for as required by the Contributions Received Subsections of this Subtopic. See paragraphs 958-720-45-18 through 45-19 for premiums provided to donors and Example 4 (paragraphs 958-220-55-11 through 55-15) for direct benefits provided to donors at special events.

958-605-55-7 Examples

Example 1 (see paragraph 958-30-55-2) and

1 (see paragraph 958-605-55-14)

paragraphs 958-605-55-13A through 55-14I illustrate the need to assess the relevant facts and circumstances to distinguish between the receipt of resources in an exchange and the receipt of resources in a contribution.

958-605-55-8 Paragraph superseded by Accounting Standards Update No. 2018-08. The following table contains a list of indicators that may be helpful in determining whether individual asset transfers are contributions, exchange transactions, or a combination of both. Depending on the facts and circumstances, some indicators may be more significant than others; however, no single indicator is determinative of the classification of a particular transaction. Indicators of a contribution tend to describe transactions in which the value, if any, returned to the resource provider is incidental to potential public benefits. Indicators of an exchange tend to describe transactions in which the potential public benefits are secondary to the potential proprietary benefits to the resource provider.

Indicators Useful in Distinguishing Contributions from Exchange Transactions

|

Recipient not-for-profit entity's (NFP's) intent in soliciting the asset (a) |

Recipient NFP asserts that it is soliciting the asset as a contribution. |

Recipient NFP asserts that it is seeking resources in exchange for specified benefits. |

Resource provider's expressed intent about the purpose of the asset to be provided to recipient NFP |

Resource provider asserts that it is making a donation to support the NFP's programs. |

Resource provider asserts that it is transferring resources in exchange for specified benefits. |

|

The time or place of delivery of the asset to be provided by the recipient NFP to third party recipients is at the discretion of the NFP. |

The method of delivery of the asset to be provided by the recipient NFP to third party recipients is specified by the resource provider. |

Method of determining amount of payment |

The resource provider determines the amount of the payment. |

Payment by the resource provider equals the value of the assets to be provided by the recipient NFP, or the assets' cost plus markup; the total payment is based on the quantity of assets to be provided. |

Penalties assessed if NFP fails to make timely delivery of assets |

Penalties are limited to the delivery of assets already produced and the return of the unspent amount. (The NFP is not penalized for nonperformance.) |

Provisions for economic penalties exist beyond the amount of payment. (The NFP is penalized for nonperformance.) |

Delivery of assets to be provided by the recipient NFP |

Assets are delivered to individuals or organizations other than the resource provider. |

Assets are to be delivered to the resource provider or to individuals or organizations closely connected to the resource provider. |

(a) This table refers to assets. Assets may include services. The terms assets and services are used interchangeably in this table.

> Illustrations

> > Distinguishing Contributions from Exchange Transactions

958-605-55-13A Examples 1 through 5 illustrate the guidance in Section 958-605-15 for determining whether a transaction is an exchange or a contribution. The analysis in each Example is not intended to represent the only manner in which the guidance could be applied, and the Examples are not intended to apply to only a specific illustration. Although some aspects of the Examples may be present in actual fact patterns, all relevant facts and circumstances of a particular fact pattern should be evaluated when applying the guidance in this Subtopic. The guidance in these Examples about distinguishing between contributions and exchange transactions applies to both a resource provider (for example, a corporate foundation, a corporation, or an NFP) and a recipient.

> > > > >

Example 1: Receipt of Resources in Exchange

958-605-55-14 This Example illustrates the guidance in paragraphs 958-605-15-5 through 15-6.

Not-for-Profit Entity A (NFP A) is a large research university with a cancer research center. NFP A regularly conducts research to discover more effective methods of treating cancer and often receives contributions to support its efforts. NFP A receives resources from a pharmaceutical entity to finance the costs of a clinical trial of an experimental cancer drug the

pharmaceutical entity developed. The pharmaceutical entity specifies the protocol of the testing, including the number of participants to be tested, the dosages to be administered, and the frequency and nature of follow-up examinations. The pharmaceutical entity requires a detailed report of the test outcome within two months of the test's conclusion.

Additionally, the rights to the results of the study belong to the pharmaceutical entity. Because the results of the clinical trial have particular commercial value for the pharmaceutical entity, receipt of the resources is not a contribution received by NFP A, nor is the disbursement of the resources a contribution made by the pharmaceutical entity.

[Content amended and moved to paragraph 958-605-55-14A]

958-605-55-14A Because the results of the clinical trial have particular commercial value for the pharmaceutical entity, the pharmaceutical entity is receiving commensurate value as the resource provider. Therefore, the receipt of the resources is not a contribution received by NFP A, nor is the disbursement of the resources a contribution made by the pharmaceutical entity. See paragraph 958-605-15-5A. [Content amended as shown and moved from paragraph 958-605-55-14]

> > > Example 2: Payment Relating to an Existing Exchange Transaction—University

958-605-55-14B Student L is enrolled at University A. Student L's total tuition charged for the semester is $30,000. Student L received a grant in the amount of $2,000 to use toward the tuition fee, which is paid directly by the grantor to University A.

958-605-55-14C The grant was awarded to Student L, not to University A. University A entered into an exchange transaction with Student L and accounts for the $30,000 of revenue in accordance with the guidance in the appropriate Subtopic. The $2,000 grant does not create additional revenue but, rather, serves as a partial payment against the $30,000 due to University A. Student L is an identified customer of University A who is receiving the benefit from the grant transaction. See paragraph 958-605-15-6(e).

> > > Example 3: Payment Relating to an Existing Exchange Transaction—Hospital

958-605-55-14D Patient R is a patient at Hospital B. The total amount due for services rendered is $10,000. Patient R has Medicare, and it covers $8,000 of the services, which is paid directly by the government to Hospital B. Hospital B bills Patient R for $2,000.

958-605-55-14E Medicare is a form of insurance. Hospital B has a contract with a customer (Patient R) and determines that the $10,000 should be accounted for as an exchange transaction in accordance with the guidance in the appropriate Topic. The Medicare payment of $8,000 and Patient R's payment of $2,000 serve as a payment source for services rendered in the amount of $10,000 owed to Hospital B. The payment to Hospital B relates to an existing exchange transaction between Hospital B and an identified customer (Patient R). See paragraph 958-605-15-6(e).

> > > Example 4: Procurement Arrangement

958-605-55-14F The local government provided funding to NFP C to perform a research study on the benefits of a longer school year. The agreement requires NFP C to plan the study, perform the research, and summarize and submit the research to the local government. The local government retains all rights to the study.

958-605-55-14G NFP C concludes that this is a procurement arrangement in which commensurate value is being exchanged between two parties and that it should follow the relevant guidance for exchange transactions. NFP C is to perform a research study for the local government and turn over a summary of the study's findings to the local government. The local government retains the rights to the study. See paragraph 958-605-15-5A(c).

> > > Example 5: Research Grant

958-605-55-14H University D applied for and was awarded a grant from the federal government. University D must follow the rules and regulations established by the Office of Management and Budget of the federal government and the federal awarding agency. University D is required to incur qualifying expenses to be entitled to the assets. Any unspent money during the grant period is forfeited, and University D is required to return any advanced funding that does not have related qualifying expenses. University D also is required to submit a summary of research findings to the federal government, but University D retains the rights to the findings and has permission to publish the findings if it desires.

958-605-55-14I University D concludes that this grant is not a transaction in which there is commensurate value being exchanged. The federal government, as the resource provider, does not receive direct commensurate value in exchange for the assets provided to University D because University D retains all rights to the research and findings. University D and the public receive the primary benefit of any findings, and the federal government receives an indirect benefit because the research and findings serve the general public. Thus, University D determines that this grant should be accounted for under the contribution guidance in this Subtopic. See paragraph 958-605-15-5A(a).

Contributions Received

> Implementation Guidance

> > Distinguishing between Donor-Imposed Conditions and Donor-Imposed Restrictions

958-605-55-15 Distinguishing between a condition stipulated by a donor and a restriction on the use of a

contribution imposed by a donor may require the exercise of judgment.

A donor-imposed condition depends on whether the agreement includes a barrier that must be overcome before a recipient is entitled to the assets transferred or promised. The agreement also must give either the contributor a right of return of the assets it has transferred or the promisor a right of release from its obligation to transfer assets. Conditional transfers are not contributions yet; they may become contributions upon the occurrence of one or more future and uncertain events. Because of the uncertainty about whether they will be met, conditions imposed by resource providers may cast doubt on whether the resource provider's intent was to make a contribution, to make a conditional contribution, or to make no contribution. As a result of this uncertainty, donor-imposed conditions

Donor-imposed conditions should be substantially met by the entity before the receipt of assets (including contributions receivable) is recognized as a contribution. In contrast to donor-imposed conditions, donor-imposed restrictions limit the use of the contribution, but they do not

change the transaction's fundamental nature from that of a

affect whether the recipient is entitled to the contribution.

958-605-55-16 If donor stipulations do not clearly state whether the right to receive

or retain payment or take delivery depends on meeting those stipulations, or if those stipulations are ambiguous, distinguishing a

conditional promise to give from an

unconditional promise to give may be difficult.

First, review the facts and circumstances surrounding the gift and communicate with the donor.

If the ambiguity cannot be resolved

by reviewing the facts and circumstances surrounding the contribution and communicating with the donoras a result of those efforts

, presume that a promise containing

{add glossary link}stipulations

{add glossary link} that are not clearly unconditional is a conditional

{add glossary link}promise to give

{add glossary link}. However, if the

stipulation is not related to the purpose of the agreement (generally stipulations that are administrative or trivial), that stipulation is not indicative of a barrierpossibility that the condition will not be met is remote, a conditional promise to give is considered unconditional.

(for For

example, a

{remove glossary link}stipulation{remove glossary link} that an annual report must be provided by the donee to receive subsequent annual payments on a multiyear promise is not a

barriercondition

if the

possibility of not meeting that

administrative requirement is

remote

not related to the purpose of the agreement).

958-605-55-17 A challenge (matching) grant is a common form of a conditional promise to give. For example, a resource provider promises to contribute $1 for each $1 of contributions received by a not-for-profit entity (NFP), up to $100,000, over the next 6 months. As contributions are received from other resource providers, the conditions would be met and the promise would become unconditional. For example, if $10,000 is received in the first month from donors, $10,000 of the conditional promise would become unconditional and should be recognized as contribution revenue.

> > Determining Whether a Contribution Is Conditional

958-605-55-17A A donor-imposed condition must have both:

- One or more barriers that must be overcome before a recipient is entitled to the assets transferred or promised.

- A right of return to the contributor for assets transferred (or for a reduction, settlement, or cancellation of liabilities) or a right of release of the promisor from its obligation to transfer assets (or to reduce, settle, or cancel liabilities).

See paragraphs 958-605-55-70A through 55-70T for examples.

958-605-55-17B It is possible that some agreements that do not contain any barriers could contain either a right of return of assets transferred or a right of release from obligation. For example, some foundations include a right-of-return or a right-of-release-from-obligation clause in their agreements as a matter of policy and standard wording but impose no barriers that must be achieved before a recipient is entitled to the resources. The resources would be considered unconditional, and revenue would be recognized immediately.

958-605-55-17C Some agreements include multiple requirements that must be overcome before an entity is entitled to transferred assets or a future transfer of assets. An entity must consider facts and circumstances and use judgment to determine which stipulations, if any, of an agreement are deemed to be a barrier or barriers that must be achieved before an entity is entitled to assets.

> > > Measurable Performance-Related Barriers or Other Measurable Barriers

958-605-55-17D As described in paragraph 958-605-25-5D, a measurable performance-related barrier or other measurable barrier may be indicative of a donor-imposed condition. Examples of measurable performance-related barriers or other measurable barriers could include:

a. Specified level of service. An entity is given assets, and the resource provider stipulates that the assets must be used to provide a specific level of service (for example, 1,000 meals per week for a soup kitchen). The barrier that must be overcome before the recipient is entitled to the resources is the specified level of service that must be achieved.

b. Specific output or outcome. An entity is given assets, entitlement to which is contingent upon producing a specific output or achieving a measurable outcome stemming from the entity's activities (for example, students achieving a minimum standardized test score, a decline in drop-out rates following an entity's educational efforts, and community residents exhibiting a decline in symptoms of malnutrition following an entity's efforts in providing meals).

c. Matching. A resource provider specifies the ratio or amount of a matching contribution. The recipient is not entitled to receive the promised assets until it has met the required match (the barrier or hurdle that must be overcome).

d. Outside event. Agreements may include requirements that are imposed on, and would need to be overcome by, other parties, including the resource provider. A resource provider specifies that a certain outside event needs to occur for the recipient to be entitled to receive the assets (for example, a resource provider promises to contribute a certain amount of assets if the resource provider's net worth reaches a specified level).

> > > Limited Discretion by the Recipient on the Conduct of an Activity

958-605-55-17E As described in paragraph 958-605-25-5D, limited discretion may be indicative of a donor-imposed condition. Limited discretion of the recipient on the conduct of an activity is more specific than a donor-imposed restriction. Restrictions limit the use of a contribution to a specific activity or time but do not necessarily place limitations on how the activity is performed. This indicator focuses on limitations concerning specific requirements about how an activity must be conducted for a recipient to be entitled to the resources. For example, an agreement might specify that the recipient should incur qualifying expenses in compliance with established rules and regulations. This is in contrast to a restriction, which typically places limits only on a specific activity that is being funded and does not affect the extent to which a recipient is entitled to the resources (for example, a requirement that a contribution be used to fund one of an organization's programs).

> > > Stipulations That Are Related to the Purpose of the Agreement

958-605-55-17F An indicator noting that a stipulation is related to the purpose of the agreement could be helpful in the context of considering the agreement collectively with the other indicators. If a stipulation is unrelated to the purpose of the agreement (for example, trivial or administrative stipulations), the stipulation would not be indicative of a barrier. If administrative tasks are required that are unrelated to the purpose of the agreement, there most likely would be other requirements that would be more indicative of a barrier that must be overcome before the recipient is entitled to the resources (for example, a specific event or activity to occur). Producing an annual report is a common requirement in contribution agreements; however, the annual report typically is not related to the underlying purpose of the agreement. Generally, a report is administrative in nature and is intended to provide a resource provider with information to confirm that the transferred assets were used in accordance with the purpose of the agreement and is not intended to affect the extent to which the recipient is entitled to the contribution.

> > Promises to Give

958-605-55-20 Promises to give services generally involve personal services that, if not explicitly conditional, are often implicitly conditioned upon the future and uncertain availability of specific individuals whose services have been promised.

958-605-55-21 Certain promises become unconditional in stages because they are dependent on several or a series of conditions—milestones—rather than on a single

future and uncertain event

condition and are recognized in increments as each of the conditions is met. Similarly, other promises are conditioned on promisees' incurring certain qualifying expenses (or costs). Those promises become unconditional and are recognized to the extent that the expenses are incurred. A portion of those

{add glossary link} contributions {add glossary link} shall

should be recognized as revenue as each of those stages is met.

>Illustrations

> > Example 6: Contribution of an Interest in an Estate

958-605-55-49 This Example illustrates the application of the recognition and measurement principles of paragraphs 958-605-25-2 and 958-605-30-2.

958-605-55-50 In 19X0, Individual notifies Church F that she has remembered the church in her will and provides a written copy of the will. In 19X5, Individual dies. In 19X6, Individual's last will and testament enters probate and the probate court declares the will valid. The executor informs Church F that the will has been declared valid and that it will receive 10 percent of Individual's estate, after satisfying the estate's liabilities and certain specific bequests. The executor provides an estimate of the estate's assets and liabilities and the expected amount and time for payment of Church F's interest in the estate.

958-605-55-51 The 19X0 communication between Individual and Church F specified an intention to give. The ability to modify a will at any time prior to death is well established; thus in 19X0 Church F did not receive a promise to give and did not recognize a contribution received. When the probate court declares the will valid, Church F would recognize a receivable and revenue for an unconditional promise to give at the fair value of its interest in the estate (see paragraphs 958-310-35-6, 958-605-30-5, and 958-605-30-6). If the promise to give contained in the valid will was instead

conditional based on a barrier that must be overcome for Church F to be entitled to the assets conditioned on a future and uncertain event

, Church F would recognize the contribution when the condition was substantially met. A conditional promise in a valid will would be disclosed in notes to financial statements (see paragraph 958-310-50-4).

> > Determining Whether a Contribution Is Conditional

958-605-55-70A Examples 13 through 21 (paragraphs 958-605-55-70C through 55-70T) illustrate how an entity might apply certain aspects of the guidance in this Subtopic in determining whether a contribution is conditional (all fact patterns are considered to be contributions or conditional contributions within the scope of this Subtopic). The analysis in each Example is not intended to represent the only manner in which the guidance could be applied, and the Examples are not intended to apply to only a specific illustration. Although some aspects of the Examples may be present in actual fact patterns, all relevant facts and circumstances of a particular fact pattern would need to be evaluated when applying the guidance in this Subtopic (for guidance on release from restrictions, see Section 958-605-45). Some examples are presented from the perspective of a resource provider (for example, an individual, a business corporation, a foundation, or an other NFP), and other examples are presented from the perspective of a resource recipient. The guidance in this Subtopic on determining whether a contribution is conditional applies to both contributions made by a resource provider and contributions received by a recipient.

> > > Qualifying Expenses

958-605-55-70B Many agreements include a requirement that assets must be used for allowable and reasonable qualifying expenses (or costs) that are based on specific requirements of an agreement about the conduct of an activity (for example, in compliance with principles issued by the Office of Management and Budget or other similarly restrictive grant documents) that results in limited discretion by a recipient on the conduct of an activity and, thus, is indicative of a donor-imposed condition. These agreements often are paid on a cost-reimbursement basis that requires a recipient to incur specific qualifying expenses to be entitled to the promised resources. The specific requirements about allowable qualifying expenses are often accompanied by very close cost reporting and monitoring by the resource provider.

> > > Example 13: Contribution by Foundation A

958-605-55-70C Foundation A gives NFP D a grant in the amount of $400,000 to provide specific career training to disabled veterans. The grant requires NFP D to provide training to at least 8,000 disabled veterans during the next fiscal year (2,000 during each quarter), with specific minimum targets that must be met each quarter. Foundation A specifies a right of release from the obligation in the agreement that it will only give NFP D $100,000 each quarter if NFP D demonstrates that those services have been provided to at least 2,000 disabled veterans during the quarter.

958-605-55-70D Foundation A determines that it should account for this grant as conditional. The agreement contains a right of release from obligation because the resource provider will only transfer assets if NFP D provides training to at least 8,000 disabled veterans during the year (with a minimum requirement of 2,000 disabled veterans per quarter) as specified in the agreement. Foundation A requires NFP D to achieve a specific level of service that would be considered a measurable performance-related barrier (in the form of milestones by specifying 2,000 disabled veterans per quarter). In this Example, NFP D's entitlement to the transferred assets is contingent upon serving at least 2,000 disabled veterans. The likelihood of serving at least 2,000 disabled veterans for the quarter is not a consideration from the perspective of either Foundation A or NFP D when assessing whether the contribution contains a barrier and is deemed conditional.

> > > Example 14: Contribution That Includes Qualifying Expenses

958-605-55-70E NFP B is a hospital that has a research program. NFP B receives a $300,000 grant from the federal awarding agency to fund thyroid cancer research. The terms of the grant specify that NFP B must incur certain qualifying expenses (or costs) in compliance with rules and regulations established by the Office of Management and Budget and the federal awarding agency. The grant is paid on a cost-reimbursement basis by NFP B initiating drawdowns of the grant assets. Any unused assets are forfeited, and any unallowed costs that have been drawn down by NFP B are required to be refunded.

958-605-55-70F NFP B determines that this grant is conditional. The grant agreement limits NFP's discretion as a result of the specific requirements on how NFP B may spend the assets (incurring certain qualifying expenses in accordance with the Office of Management and Budget rules and regulations). The grant also includes a release from the promisor's obligation for unused assets. The requirement to spend the assets on qualifying expenses is a barrier to entitlement because the requirement limits NFP B's discretion about how to use the assets, and the assets would need to be spent on specific items on the basis of the requirements of the agreement (for example, adherence to cost principles) before NFP B is entitled to the assets. This is in contrast to a restriction that typically places limits only on a specific activity that is being funded. NFP B records revenue during the grant period when the barriers have been overcome as it incurs qualifying expenses. The likelihood of incurring qualifying expenses is not a consideration when assessing whether the contribution is deemed conditional.

> > > Example 15: Contribution for a Research Grant

958-605-55-70G NFP E is a public charity that performs research on various diseases and allergies, including gluten-related allergies, as part of its overall mission. It receives a $100,000 grant from a foundation to perform research on gluten-related allergies over the next year. The grant agreement includes a right of return as part of the foundation's standard wording and a requirement that at the end of the grant period a report must be filed with the foundation that explains how the assets were spent.

958-605-55-70H NFP E determines that the grant is not a conditional contribution. The purpose of research on gluten-related allergies results in donor-restricted revenue because the purpose of the grant (working on gluten-free allergies) is narrower than the overall mission of the entity. There are no requirements in the agreement that would indicate that a barrier exists, which must be overcome before the recipient is entitled to the resources. NFP E also determines that the reporting requirement alone is not a barrier because it is an administrative requirement and not related to the purpose of the agreement, which is the actual research. This is an example in which a grant including a right of return could not be considered conditional because the return clause is not coupled with a barrier to be overcome, as determined by NFP E using judgment to assess the indicators of a barrier.

> > > Example 16: Contribution to a Hospital

958-605-55-70I NFP DD is a hospital that received an upfront cash contribution from an individual to perform research on Alzheimer's disease during NFP DD's next fiscal year. The agreement does not include a right of return or a barrier that must be overcome to be entitled to the funds.

958-605-55-70J NFP DD determines that this contribution is not conditional because it does not include a right of return (or similar language) of the assets that have been transferred upfront. NFP DD concludes that it should recognize the revenue upon receipt of the assets from the individual as donor-restricted because it is required to use the assets for Alzheimer's research, which is narrower than NFP DD's overall mission, during the next fiscal year.

> > > Example 17: Contribution from a Foundation

958-605-55-70K Foundation B receives a grant proposal from an animal rescue facility, NFP F, which requests a 2-year grant in the amount of $500,000 upfront to be used to expand its operations. The agreement indicates that NFP F must expand its facility by at least 5,000 square feet to accommodate additional animals by the end of the 2 years. The grant contains a right of return if the minimum expansion target is not achieved.

958-605-55-70L Foundation B determines that this grant is conditional. The grant includes a measurable barrier (5,000 additional square feet) that must be achieved by NFP F to be entitled to the assets and a right of return for unused assets or unmet requirements.

> > > Example 18: Contribution to a University

958-605-55-70M NFP G is a university that is conducting a capital campaign to build a new building to house its school of mathematics and to make capital improvements to existing buildings on campus, including a new heating system and an upgraded telephone and computer network. NFP G receives an upfront grant in the amount of $10,000 from a foundation as part of its capital campaign. The agreement contains a right of return requiring that the assets be reimbursed to the resource provider if the assets are not used for the purposes outlined in the capital campaign solicitation materials. The resource provider does not include any specifications in the agreement about how the building should be constructed or on how other improvements should be made.

958-605-55-70N NFP G determines that this grant is not conditional because the agreement places limits only on the specific activity that is being funded (for example, the assets can be used toward the new building or toward other capital improvements such as the heating system and an upgraded telephone and computer network within existing buildings on campus). The resource provider does not include any specifications about how the building should be constructed, and the agreement only indicates that NFP G must use the grant for the purpose outlined in the capital campaign materials. NFP G recognizes this grant as donorrestricted revenue because it must be used for capital purposes, which is narrower than NFP G's overall mission. This Example illustrates a fact pattern in which a grant can include a right of return and would be deemed a contribution that does not contain a donor-imposed condition because the return clause is not coupled with a barrier to be overcome, as determined by NFP G using judgment to assess the indicators of a barrier.

> > > Example 19: Contribution to a Museum

958-605-55-70O NFP I is a museum that receives a grant from an individual donor to build a new wing on the existing museum building. The agreement contains a $1 million multiyear promise to give the money to be used for the new wing on the building. The agreement also includes specific building requirements, including square footage and that the new wing must be environmentally friendly with Leadership in Energy and Environmental Design certification. The first installment of the gift will not be paid until NFP I submits architectural designs that meet the building requirements. Additional installments of the grant will be paid in specified increments upon achieving other milestones identified in the grant agreement. If a particular milestone is not achieved, the donor is released from its obligation to make installment payments.

958-605-55-70P NFP I determines that this agreement is conditional because NFP I is not entitled to the assets until a milestone is met (for example, an architectural plan including square footage and Leadership in Energy and Environmental Design certification). In this example, a milestone is deemed a measurable performance barrier because NFP I's entitlement to the transferred assets is contingent upon the completion of a milestone. In addition, the agreement includes a release of the resource provider's obligation to transfer assets if the stipulations are not met. NFP I recognizes the revenue as the barriers are overcome, which is upon meeting the specific requirements as NFP I builds the new wing. The likelihood of meeting a milestone is not a consideration when assessing whether the contribution is deemed conditional.

> > > Example 20: Contribution to a Homeless Shelter

958-605-55-70Q NFP J operates as a homeless shelter that provides individuals with temporary accommodations, meals, and counseling. NFP J receives an upfront grant of $75,000 from the city for its meals program. The grant requires NFP J to use the assets to provide at least 5,000 meals to the homeless. The grant contains a right of return for meals not served.

958-605-55-70R NFP J determines that this grant is conditional because it contains a measurable performance-related barrier (to provide 5,000 meals) and a right of return. NFP J recognizes assets received in advance of satisfying the conditions as a refundable advance liability and will then recognize $75,000 as donor-restricted revenue when at least 5,000 meals are served because the purpose of the grant is narrower than the overall purpose of NFP J. The likelihood of providing the meals is not a consideration when assessing whether the contribution is deemed conditional.

> > > Example 21: Contribution to a Recreational Organization

958-605-55-70S NFP H is a recreational organization that provides various sports programs to children that live in the community. NFP H receives an upfront grant in the amount of $40,000 from a foundation to be used toward its tennis program. Consistent with NFP H's grant proposal, the agreement includes specific guidelines for which NFP H could use the assets (for example, to hire 10 tennis instructors or to provide a summer camp for 9 weeks) but does not specify that NFP H's entitlement to the $40,000 is dependent upon NFP H meeting any of the specific indicated guidelines in the agreement. The grant contains a right of return for funds not spent on the tennis program.

958-605-55-70T NFP H determines that this grant is not conditional because it does not contain a barrier to overcome to be entitled to the transferred assets. Although the grant agreement contains guidelines for how NFP H could spend the $40,000, the agreement does not specify that entitlement to the transferred assets are dependent upon meeting any of the guidelines. Because the guidelines in the grant agreement were not required to be met to be entitled to the funding, the agreement does not contain a barrier to overcome. NFP H should recognize the revenue upon receipt of the assets as donor restricted because it is required to use the assets for the tennis program, which is narrower than NFP H's overall mission.

Transfers of Assets to a Not-for-Profit Entity or Charitable Trust That Raises or Holds Contributions for Others

>Illustrations

> > Example 3: Recipient Entity Is an Intermediary

958-605-55-82 Paragraph superseded by Accounting Standards Update No. 2018-08. This Example illustrates the guidance in paragraph 958-605-25-23. Hospital C provides health care services to patients that are entitled to Medicaid assistance under a joint federal and state program. The program sets forth various administrative and technical requirements covering provider participation, payment mechanisms, and individual eligibility and benefit provisions. Medicaid payments made to Hospital C on behalf of the program beneficiaries are third-party payments for patient services rendered. Hospital C provides patient care for a fee—an exchange transaction—and acts as an intermediary between the government provider of assistance and the eligible beneficiary. The Medicaid payments are not contributions to Hospital C.