3. Supersede paragraphs 926-20-25-6 through 25-7 and their related heading, and amend paragraph 926-20-25-8 and its related heading, with a link to transition paragraph 926-20-65-2, as follows:

Entertainment—Films—Other Assets—Film Costs

Recognition

General

> Film Costs Capitalization

926-20-25-1 An entity shall report film costs as a separate asset on its balance sheet.

> Episodic Television Series

926-20-25-6 Paragraph superseded by Accounting Standards Update No. 2019-02. For an episodic television series, ultimate revenue (see discussion of ultimate revenue in paragraphs 926-20-35-4 through 35-8) can include estimates from the initial market and secondary markets. Until an entity can establish estimates of secondary market revenue in accordance with paragraph 926-20-35-5(b), capitalized costs for each episode produced shall not exceed an amount equal to the amount of revenue contracted for that episode. An entity shall expense as incurred film costs in excess of this limitation on an episode-by-episode basis, and an entity shall not restore such amounts as film cost assets in subsequent periods. For more information, see Example 3 (paragraph 926-20-55-9).

926-20-25-7 Paragraph superseded by Accounting Standards Update No. 2019-02.Once an entity can establish estimates of secondary market revenue in accordance with paragraph 926-20-35-5(b), the entity shall capitalize subsequent film costs. When an entity is in this situation, the uncertainties surrounding whether a series will be successful are sufficiently minimized and, therefore, the probability of the recoverability of any additional film costs above contracted-for-revenue is high enough such that an entity shall not immediately expense costs in excess of contracted-for-revenue.

> Significant Changes to a Film

926-20-25-8 The costs incurred for

significant changes

significant changes to a film shall be added to film costs and subsequently charged to expense when an entity recognizes the related revenue.

926-20-25-9 Mere insertion or addition of preexisting film footage, addition of dubbing or subtitles (which by definition is done to existing footage), removal of offensive language, reformatting of a film to fit a broadcaster's screen dimensions, and adjustments to allow for the insertion of commercials are all examples of changes to a film that are not significant.

4. Amend paragraphs 926-20-35-1 through 35-2 and their related heading, 926-20-35-4, 926-20-35-12, and 926-20-35-13 through 35-17 and the related heading, supersede paragraphs 926-20-35-9 through 35-11 and their related heading, and add paragraphs 926-20-35-3A through 35-3C and the related heading, 926-20-35-12A through 35-12B, and 926-20-35-19 and its related heading, with a link to transition paragraph 926-20-65-2, as follows:

Subsequent Measurement

> Film Costs Amortization—Individual-Film-Forecast-Computation Method

926-20-35-1 For a film that is predominantly monetized on its own, anAn

entity shall amortize

film costs using the individual-film-forecast-computation method, which amortizes such costs in the same ratio that current period actual revenue (numerator) bears to estimated remaining unrecognized ultimate revenue as of the beginning of the current fiscal year (denominator). In this way, in the absence of changes in estimates, film costs are amortized in a manner that yields a constant rate of profit over the ultimate period, as described in paragraph 926-20-35-5(a), for each film before

exploitation costs, manufacturing costs, and other period expenses. Unamortized film costs as of the beginning of the current fiscal year are multiplied by the individual-film-forecast-computation method fraction. That is, an entity shall begin amortization of capitalized film costs when a film is released and it begins to recognize revenue from that film. For more information, see Example 1 (paragraph 926-20-55-1).

For a film that is predominantly monetized on its own but also monetized with other films and/or license agreements, an entity shall make a reasonably reliable estimate of the value attributable to the film's exploitation while monetized with other films and/or license agreements for inclusion in its individual-film-forecast computation. For purposes of applying the individual-film-forecast-computation method to episodic television series, multiple seasons of an episodic television series are considered to be a single product. For more information, see Example 4 (paragraph 926-20-55-12).

926-20-35-2 For a film that is in a film group,

In the absence of revenue from third parties that is directly related to the exhibition or exploitation of a film

, an entity shall make a reasonably reliable estimate of the portion of unamortized film costs that is representative of the use of the film

in that exhibition or exploitation

. An entity shall expense such amounts as it exhibits or exploits the film. (For example,

a cable

an entity

with a direct-to-consumer streaming platform that does not accept advertising on its

cable channel

platform may produce a film and

only show it on

that

channel

its platform. In this example, the cable entity receives subscription fees from third parties that are not directly related to a particular film.)

Consistent with the underlying premise of the individual-film-forecast-computation method, all revenue shall bear a representative amount of the amortization of film costs during the ultimate period.

926-20-35-3 As a result of uncertainties in the estimating process, actual results may vary from estimates. An entity shall review and revise estimates of ultimate revenue as of each reporting date to reflect the most current available information. If estimates are revised, an entity shall determine a new denominator that includes only the ultimate revenue from the beginning of the fiscal year of change (that is, ultimate revenue changes are treated prospectively as of the beginning of the fiscal year of change). The numerator (revenue for the current fiscal year) is unaffected by the change. An entity shall apply the revised fraction to the net carrying amount of unamortized film costs as of the beginning of the fiscal year, and the difference between expenses determined using the new estimates and any amounts previously expensed during that fiscal year shall be charged or credited to the income statement in the period (for example, the quarter) during which the estimates are revised. For more information, see Example 2 (paragraph 926-20-55-5).

926-20-35-3A An entity shall review and revise estimates of the remaining use of the film for film costs amortized in accordance with paragraph 926-20-35-2 as of each reporting date to reflect the most current available information. Changes to estimates of the remaining use of a film shall be accounted for prospectively.

> Predominant Monetization Strategy

926-20-35-3B An entity shall determine whether a film is part of a film group when capitalization of film costs begins by assessing whether it is expected to be predominantly monetized on its own or predominantly monetized with other films and/or license agreements.

926-20-35-3C If there is a significant change to the monetization strategy of a film compared with the monetization strategy determined when capitalization of film costs began, an entity shall reassess the predominant monetization strategy for that film. The reassessment of the predominant monetization strategy shall include an assessment of the monetization strategy throughout the entire life of the film rather than an assessment from the time of the significant change in monetization strategy. Two examples of a significant change to the monetization strategy of a film are adding a previously unplanned significant distribution channel and forgoing a previously planned significant distribution channel. For purposes of determining whether there is a significant change to the monetization strategy, results of the monetization strategy that are different from the expected results shall not be considered a significant change to the monetization strategy.

> Ultimate Revenue

926-20-35-4 Ultimate revenue to be included in the denominator of the individual-film-forecast-computation method fraction shall include estimates of revenue that is expected to be recognized by an entity from the exploitation, exhibition, and sale of a film in all markets and territories, subject to the limitations set forth in

the following

paragraph

926-20-35-5 and paragraph 926-20-35-11

.

926-20-35-5 Ultimate revenue shall be limited by the following:

- For films other than episodic television series, ultimate revenue shall include estimates over a period not to exceed 10 years following the date of the film's initial release. For episodic television series, ultimate revenue shall include estimates of revenue over a period not to exceed 10 years from the date of delivery of the first episode or, if still in production, 5 years from the date of delivery of the most recent episode, if later. For previously released films acquired as part of a film library, ultimate revenue shall include estimates over a period not to exceed 20 years from the date of acquisition. For the purposes of this Topic, an entity shall categorize as part of a film library only those individual films whose initial release dates were at least three years prior to the acquisition date.

- Ultimate revenue shall include estimates of revenue from a market or territory only if persuasive evidence exists that such revenue will occur, or if an entity can demonstrate a history of recognizing such revenue in that market or territory. Ultimate revenue shall include estimates of revenue from newly developing territories only if an existing arrangement provides persuasive evidence that an entity will realize such amounts.

- Ultimate revenue shall include estimates of revenue from licensing arrangements with third parties to market film-related products only if persuasive evidence exists that such revenue from that arrangement will occur for that particular film (such as a signed contract to receive a nonrefundable minimum guarantee or a nonrefundable advance) or if an entity can demonstrate a history of recognizing such revenue from that form of arrangement.

- Ultimate revenue shall include estimates of the portion of the wholesale or retail revenue from an entity's sale of peripheral items (such as toys and apparel) that is attributable to the exploitation of themes, characters, or other contents related to a particular film only if the entity can demonstrate a history of recognizing such revenue from that form of exploitation in similar kinds of films. For example, an entity may conclude that the portion of revenue from the sale of peripheral items that it shall include in ultimate revenue is an estimate of what would be recognized by the entity if rights for such form of exploitation had been granted under licensing arrangements with third parties. Ultimate revenue shall not, however, include estimates of the entire amount of wholesale or retail revenue from an entity's sale of peripheral items.

- Ultimate revenue shall not include estimates of revenue from unproven or undeveloped technologies.

- Ultimate revenue shall not include estimates of wholesale promotion or advertising reimbursements to be received from third parties. Such amounts shall be offset against exploitation costs.

- Ultimate revenue shall not include estimates of amounts related to the sale of film rights for periods after those identified in (a).

> Episodic Television Series

926-20-35-9 Paragraph superseded by Accounting Standards Update No. 2019-02.Multiple seasons of an episodic television series that meets the conditions of paragraph 926-20-35-11 to include estimated secondary market revenue in ultimate revenue is considered to be a single product, with multiple seasons of the series combined for purposes of applying the individual-film-forecast-computation method. For more information, see Example 4 (paragraph 926-20-55-12).

926-20-35-10 Paragraph superseded by Accounting Standards Update No. 2019-02.The following paragraph and paragraph 926-20-35-5 address estimates of ultimate revenues for an episodic television series.

926-20-35-11 Paragraph superseded by Accounting Standards Update No. 2019-02.Ultimate revenue for an episodic television series also shall include estimates of secondary market revenue (that is, revenue from markets other than the initial market) for produced episodes only if an entity can demonstrate through its experience or industry norms that the number of episodes already produced, plus those for which a firm commitment exists and the entity expects to deliver, can be licensed successfully in the secondary market.

> Film Costs Valuation

Impairment

926-20-35-12 Unamortized film costs shall be tested for impairment whenever events or changes in circumstances indicate that the fair value of

the film

a film predominantly monetized on its own (see paragraph 926-20-35-12A) or a film group (see paragraph 926-20-35-12B) may be less than its unamortized costs.

The following are examples of events or changes in circumstances that indicate that an entity shall assess whether the fair value of a film (whether completed or not) is less than its unamortized film costs:

An adverse change in the expected performance of a film prior to release

Actual costs substantially in excess of budgeted costs

Substantial delays in completion or release schedules

Changes in release plans, such as a reduction in the initial release pattern

Insufficient funding or resources to complete the film and to market it effectively

Actual performance subsequent to release failing to meet that which had been expected prior to release.

[Content amended and moved to paragraph 926-20-35-12A]

926-20-35-12A The following are examples of events or changes in circumstances that indicate that an entity shall assess whether the fair value of a film (whether completed or not) is less than its unamortized film costs:

a. An adverse change in the expected performance of a film prior to release

b. Actual costs substantially in excess of budgeted costs

c. Substantial delays in completion or release schedules

d. Changes in release plans, such as a reduction in the initial release pattern

e. Insufficient funding or resources to complete the film and to market it effectively

f. Actual performance subsequent to release failing to meet

that which had been expected prior to release

.

expectations set before release due to factors such as the following:1. A significant adverse change in technological, regulatory, legal, economic, or social factors that could affect the public's perception of a film or the availability of a film for future showings

2. A significant decrease in the amount of ultimate revenue expected to be recognized.

g. A change in the predominant monetization strategy of a film resulting in the film being predominantly monetized with other films and/or license agreements. [Content amended as shown and moved from paragraph 926-20-35-12]

926-20-35-12B The following are examples of events or changes in circumstances for a film group that indicate that an entity shall assess whether the fair value of a film group is less than its unamortized film costs:

- A significant adverse change in technological, regulatory, legal, economic, or social factors that could affect the fair value of the film group

- A significant decrease in the number of subscribers or forecasted subscribers, or the loss of a major distributor

- A current-period operating or cash flow loss combined with a history of operating or cash flow losses or a projection of continuing losses associated with the use or exploitation of a film group.

926-20-35-13 If an event or change in circumstances indicates that an entity shall assess whether the fair value of a film (or film group) is less than its unamortized film costs, the entity shall determine the fair value of the film (or film group) (the determination of which is affected by estimated future exploitation costs still to be incurred) and write off to the income statement the amount by which the unamortized capitalized costs exceed the film's (or film group's) fair value. Exploitation costs incurred after such a write-off shall be accounted for in accordance with the provisions of paragraphs 926-720-25-2 through 25-3. An entity shall treat the reduced amount of capitalized film costs that have been written down to fair value (subject to paragraph 926-20-35-19 for films in a film group) at the close of an annual fiscal period as the cost for subsequent accounting purposes, and an entity shall not subsequently restore any amounts previously written off.

926-20-35-14 A discounted cash

flows

flow model is

often

may be used to estimate fair value. If applicable, future cash flows based on the terms of any existing contractual arrangements, including cash flows over existing license periods without consideration of the limitations set forth in

paragraphs

paragraph 926-20-35-5

and 926-20-35-11

, shall be included.

926-20-35-15 An entity shall consider the following factors, among others, in estimating future cash inflows for a film:

- If previously released, the film's performance in prior markets

- The public's perception of the film's story, cast, director, or producer

- Historical results of similar films

- Historical results of the cast, director, or producer on prior films

- Running time of the film.

In determining a film's (or film group's) fair value, it is also necessary to consider those cash outflows necessary to generate the film's (or film group's) cash inflows.

Therefore, an entity shall incorporate, if applicable, its estimates of future costs to complete a film, future exploitation and

participation costs, or other necessary cash outflows in its determination of fair value when using a discounted cash

flows

flow model.

926-20-35-16 When using the traditional discounted cash flow approach to estimate the fair value of a film

(or film group), the relevant future cash inflows and outflows shall represent the entity's estimate of the most likely cash flows. When determining the fair value of a film

(or film group) using the expected cash

flows

flow approach, all possible relevant future cash inflows and outflows shall be probability-weighted by period and the estimated mean or average by period shall be used.

926-20-35-17 When determining the fair value of a film (or film group) using a traditional discounted cash flow approach, the discount rate(s) shall not be an entity's incremental borrowing rate(s), liability settlement rate(s), or weighted average cost of capital because those rates typically do not reflect the risks associated with a particular film (or film group). The discount rate(s) shall consider the time value of money and the expectations about possible variations in the amount or timing of the most likely cash flows and an element to reflect the price market participants would seek for bearing the uncertainty inherent in such an asset, as well as other factors, sometimes unidentifiable, including illiquidity and market imperfections. When determining the fair value of a film (or film group) using the expected cash flow approach, the discount rate(s) also would consider the time value of money. Because they are reflected in the expected cash flows, there would be no adjustment for possible variations in the amounts or timing of those cash flows. If not reflected in risk-adjusted expected cash flows, an additional element to reflect the price market participants would seek for bearing the uncertainty inherent in such an asset as well as other factors, sometimes unidentifiable, including illiquidity and market imperfections, shall be added to the discount rate(s).

> > Allocating Impairment Losses to a Film Group

926-20-35-19 An impairment loss attributable to a film group shall reduce only the carrying amounts of a film or license agreement included in that film group. The loss shall be allocated to the films and license agreements within the film group on a pro rata basis using the relative carrying amounts of those assets. However, if an entity can estimate the fair value of individual films and license agreements in the film group without undue cost and effort, it shall not reduce the carrying amount of those films below their fair value.

5. Supersede paragraph 926-20-40-4 and its related heading and add paragraph 926-20-40-5, with a link to transition paragraph 926-20-65-2, as follows:

Derecognition

> Episodic Television Series

926-20-40-4 Paragraph superseded by Accounting Standards Update No. 2019-02.An entity shall expense all capitalized costs (including set costs) for each episode of an episodic television series as it recognizes the related revenue for each episode.

926-20-40-5 An entity shall write off remaining unamortized film costs when a film is substantively abandoned.

6. Supersede paragraph 926-20-45-1 and add paragraph 926-20-45-2, with a link to transition paragraph 926-20-65-2, as follows:

Other Presentation Matters

> Film Costs

926-20-45-1 Paragraph superseded by Accounting Standards Update No. 2019-02.If an entity presents a classified balance sheet, it shall classify film costs as noncurrent on the face of the balance sheet.

926-20-45-2 Film costs shall be presented separately from the rights acquired under a license agreement for program materials within the scope of Subtopic 920-350 on entertainment—broadcasters either on the balance sheet or in the notes to financial statements.

7. Supersede paragraphs 926-20-50-1 and 926-20-50-3 through 50-4, add paragraphs 926-20-50-1A and 926-20-50-4A through 50-4C, and amend paragraph 926-20-50-2, with a link to transition paragraph 926-20-65-2, as follows:

Disclosure

> Film Costs

926-20-50-1 Paragraph superseded by Accounting Standards Update No. 2019-02. Regardless of whether it presents a classified or unclassified balance sheet, an entity shall disclose in the notes to financial statements the portion of the costs of its completed films that are expected to be amortized during the upcoming operating cycle. An operating cycle is presumed to be 12 months. An entity shall disclose its operating cycle if it is other than 12 months.

926-20-50-1A An entity shall disclose its methods of accounting for film costs, including, but not limited to, the following:

- The method(s) used in computing amortization

- For impairment, a description of the unit(s) of account used for impairment testing and the method(s) used for determining fair value.

926-20-50-2 An entity shall disclose the components of

{remove glossary link}film costs{remove glossary link} (including released, completed and not released, in production, or in development or preproduction) separately for

theatrical films and direct-to-television product

films predominantly monetized on their own and films predominantly monetized with other films and/or license agreements.

926-20-50-3 Paragraph superseded by Accounting Standards Update No. 2019-02. An entity shall disclose the percentage of unamortized film costs for released films, excluding acquired film libraries, that it expects to amortize within three years from the date of the balance sheet. If that percentage is less than 80 percent, an entity shall provide additional information, including the period required to reach an amortization level of 80 percent.

926-20-50-4 Paragraph superseded by Accounting Standards Update No. 2019-02. An entity shall disclose its methods of accounting for film costs.

926-20-50-4A An entity shall disclose the following information in the financial statements or in the notes to financial statements for each period for which a statement of financial performance is presented:

- The aggregate amortization expense for each period, separately for films predominantly monetized on their own and films predominantly monetized with other films and/or license agreements

- The caption in the income statement where the amortization is recorded.

926-20-50-4B For the most recent annual period for which a statement of financial position is presented, an entity shall disclose the following in the notes to financial statements, separately for films predominantly monetized on their own and for films predominantly monetized with other films and/or license agreements:

- For completed and not released films, the portion of the costs of completed films that an entity expects to amortize during the upcoming operating cycle. An operating cycle is presumed to be 12 months. An entity shall disclose its operating cycle if it is other than 12 months.

- For released films, the portion of the costs of released films recognized at the date of the most recent statement of financial position that an entity expects to amortize within each of the next three operating cycles.

926-20-50-4C For impairment amounts recognized for films or film groups, an entity shall disclose the following information in the notes to financial statements that include the period in which the impairment is recognized:

- A general description of the facts and circumstances leading to the impairment

- The aggregate amount of impairment losses

- The caption in the income statement where the impairment losses are recorded

- If applicable, the segment(s) under Topic 280 where the impairment losses are recorded.

8. Supersede paragraphs 926-20-55-9 through 55-11 and their related heading, and amend paragraphs 926-20-55-12 through 55-15, with a link to transition paragraph 926-20-65-2, as follows:

Implementation Guidance and Illustrations

> Illustrations

> > Example 3: Episodic Television Production Costs

926-20-55-9 Paragraph superseded by Accounting Standards Update No. 2019-02.This Example provides an illustration of accounting for costs of episodic television production prior to the establishment of secondary market revenue estimates (in accordance with paragraphs 926-20-25-6 through 25-7 and 926-20-40-4).

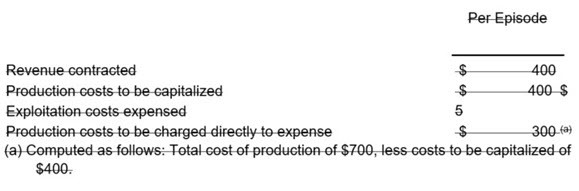

926-20-55-10 Paragraph superseded by Accounting Standards Update No. 2019-02.This Example has the following assumptions:

An episodic television series is in its first year of production.

Secondary market revenue estimable: none.

Cost of production, per episode after the first episode: $700 (assume that most of the set costs were accounted for as part of the first episode, which is not illustrated in this example).

Exploitation costs, per episode: $5.

Estimated ultimate revenue per episode: contracted $ 400.

926-20-55-11 Paragraph superseded by Accounting Standards Update No. 2019-02.Secondary market revenue is not estimable per paragraph 926-20-35-11. Accordingly, capitalization of film costs is limited as follows.

> > Example 4: Episodic Television Series—Individual-Film-Forecast-Computation Method

926-20-55-12 This Example provides an illustration of the individual-film-forecast method of amortization for an episodic television series

with multiple seasons (in accordance with

paragraph 926-20-35-1 paragraph 926-20-35-9).

926-20-55-13 This Example has the following assumptions:

a. An entity produces and distributes an episodic television series.

Five

Two seasons of the series are ultimately produced.

b. The entity's fiscal year end corresponds directly with the completion of each production season.

c.

Subparagraph superseded by Accounting Standards Update No. 2019-02.The beginning of Season 4 is when secondary market revenue estimates are initially established.

d. Costs of production are the following:

1.

Subparagraph superseded by Accounting Standards Update No.2019-02.Seasons 1 to 3: $36,000 (fully expensed prior to Season 4)

2.

Season 4

Season 1: $16,000

3.

Season 5

Season 2: $18,000.

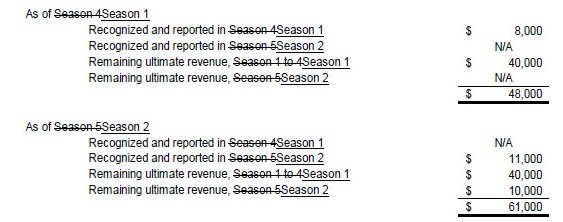

e. Recognized and remaining ultimate revenues are the following.

f. Ultimate participation costs are as follows.

926-20-55-14 Amortization of film costs in accordance with

paragraph 926-20-35-9

paragraph 926-20-35-1 is determined as follows for

Seasons 4 and 5

Seasons 1 and 2.

(a) Recognized and reported revenue during the current season.

(b) Remaining ultimate revenue at the beginning of the current season.

(c) Remaining unamortized film costs at the beginning of

Season 4

Season 1 ($0 from Seasons 1 to 3 plus the cost of production of Season 4)

.

(a) Recognized and reported revenue during the current season.

(b) Remaining ultimate revenue at the beginning of the current season.

(c) Remaining unamortized film costs at the beginning of

Season 5

Season 2 ($13,333 unamortized as of the end of

Season 4

Season 1 plus the $18,000 cost of production of

Season 5

Season 2).

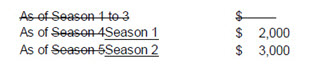

926-20-55-15 Accrual of participation costs is determined as follows.

(a) Recognized and reported revenue during the current season.

(b) Remaining ultimate revenue at the beginning of the current season.

(c) Remaining unaccrued participation costs at the beginning of

Season 4

Season 1.

(a) Recognized and reported revenue during the current season.

(b) Remaining ultimate revenue at the beginning of the current season.

(c) Remaining unaccrued participation costs at the beginning of

Season 5

Season 2 (ultimate cost of $3,000, less prior cumulative accrual of $333).

9. Add paragraph 926-20-65-2 and its related heading as follows:

> Transition Related to Accounting Standards Update No. 2019-02, Entertainment—Films—Other Assets—Film Costs (Subtopic 926-20) and Entertainment—Broadcasters—Intangibles—Goodwill and Other (Subtopic 920-350): Improvements to Accounting for Costs of Films and License Agreements for Program Materials

926-20-65-2 The following represents the transition and effective date information related to Accounting Standards Update No. 2019-02, Entertainment—Films—Other Assets—Film Costs (Subtopic 926-20) and Entertainment—Broadcasters—Intangibles—Goodwill and Other (Subtopic 920-350): Improvements to Accounting for Costs of Films and License Agreements for Program Materials:

- For public business entities, the pending content that links to this paragraph shall be effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2019.

- For all other entities, the pending content that links to this paragraph shall be effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2020.

- Early application of the pending content that links to this paragraph is permitted, including early adoption in any interim period, for:

- Public business entities for periods for which financial statements have not yet been issued

- All other entities for periods for which financial statements have not yet been made available for issuance.

- An entity shall apply the pending content that links to this paragraph prospectively at the beginning of the interim period that includes the adoption date.

- For purposes of the transition guidance in (d), an entity shall determine the predominant monetization strategy for all its existing films on the basis of the predominant monetization strategy for the remaining life of the film.

- An entity that applies the pending content that links to this paragraph shall disclose the following in the interim and annual periods of the year of adoption:

- The nature of and reason for the change in accounting principle

- The transition method

- A qualitative description of the financial statement line items affected by the change.