This paper has been prepared by the staff of the IFRS Foundation and the FASB for discussion at a public meeting of the FASB | IASB Joint Transition Resource Group for Revenue Recognition. It does not purport to represent the views of any individual members of either board or staff. Comments on the application of U.S. GAAP or IFRS do not purport to set out acceptable or unacceptable application of U.S. GAAP or IFRS.

Background and Purpose

1. Some stakeholders informed the staff that there are questions about the guidance in Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers, and IFRS 15 Revenue from Contracts with Customers (collectively referred to as the "new revenue standard"), for customer options that provide a material right.

2. Entities regularly grant options for additional goods and services to customers in the ordinary course of business. Some options are given as part of an entity's marketing efforts (that is, efforts to obtain future contracts with customers) while others are granted to customers (often implicitly) as part of a present contract and give those customers a right to acquire additional goods or services at a discount. Marketing and promotional offers are options that exist independently of a present contract with a customer and, therefore, do not constitute performance obligations in that contract.

3. Customer options come in many forms, including sales incentives, customer award (loyalty) credits (or points), contract renewal options, or other discounts on future goods or services. The following are some examples of options that exist in practice:

(a) A loyalty program that allows an entity's customers to accumulate points for every dollar spent. Those points may then be used to obtain free goods or services when enough points have been earned through future purchases.

(b) A voucher for a discount on future purchases made within a specified time period. The voucher is received only after a customer makes an initial purchase.

(c) A renewal option that allows an entity's customers to renew a contract at the end of the contract term by paying a renewal amount that is less than what the entity would charge its new customers for similar services.

(d) A contract that requires an entity's customers to pay a nonrefundable upfront fee (that does not relate to a promised good or service), but also includes an option that allows customers to renew the contract without paying an additional fee. The renewal rate may be fixed at contract inception or agreed upon at a later date.

4. At its October 31, 2014 meeting, the FASB-IASB Joint Transition Resource Group for Revenue Recognition (the "TRG") discussed the types of factors that should be considered when evaluating whether a customer option to acquire additional goods or services provides a material right (TRG Agenda ref 6). Most TRG members agreed with the staff that the evaluation should consider relevant transactions with the customer (that is, current, past, and future transactions) and should consider both quantitative and qualitative factors, including whether the right accumulates (for example, loyalty points).

5. Because the discussion indicated that stakeholders can understand and apply the applicable guidance in the new revenue standard in a manner that the staff believes is consistent with the standard, the staff did not recommend that the Boards take any further action.

6. Subsequent to the October 2014 TRG meeting, some stakeholders raised other questions about the accounting for a customer option that provides a material right. This paper summarizes the questions that were reported to the staff. The staff plan to ask the members of the TRG for their views on this topic.

Accounting Guidance

7. The relevant accounting guidance has been included in Appendix A of this paper.

Implementation Issues

8. This section of the paper includes questions that have been brought to the staff's attention about the accounting for customer options that provide a material right. Where applicable, the staff included examples to facilitate a discussion among members of the TRG.

Issue 1: How should an entity account for a customer's exercise of a material right?

9. The staff is aware of the following three views:

(a) View A—The exercise of a material right should be accounted for as a continuation of the contract because the current contract contemplates the additional goods or services subject to the material right. That is, an entity should account for the exercise as a change in the transaction price of a contract in accordance with paragraphs 606-10-32-42 through 32-45 [87– 90].

At the time a customer exercises a material right, an entity should update the transaction price of the contract to include any consideration to which the entity expects to be entitled as a result of the exercise. The additional consideration should be allocated to the performance obligation underlying the material right and should be recognized as the performance obligation underlying the material right is satisfied.

(b) View B—The exercise of a material right should be accounted for as a contract modification. That is, the additional consideration received and/or the additional goods or services provided when a customer exercises a material right represent a change in the scope and/or price of a contract. An entity should apply the modification guidance in paragraphs 606-10-25-10 through 25-13 [18–21].

(c) View C—The exercise of a material right should be accounted for as variable consideration. Any potential additional consideration related to the exercise of the material right should be accounted in accordance with the variable consideration guidance in paragraphs 606-10-32-5 through 32-9 [50–54] and paragraphs 606-10-32-11 through 32-13 [56–58].

Example

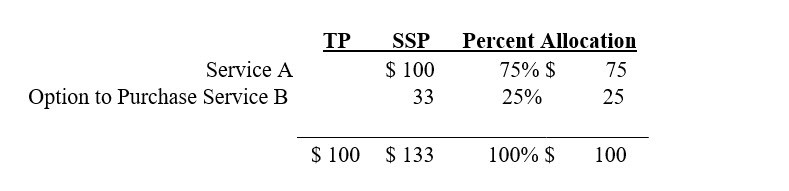

10. Entity enters into a contract with Customer to provide two years of Service A for $100. The arrangement also includes an option for Customer to purchase two years of Service B for $300. The standalone selling prices of Services A and B are $100 and $400, respectively. Entity concludes that the option to purchase Service B at a discount provides Customer with a material right. Entity's estimate of the standalone selling price of the option is $33.

11. Entity allocates the $100 transaction price to each performance obligation as follows:

12. Upon executing the contract, Customer pays $100 and Entity begins transferring Service A to Customer. The $75 allocated to Service A will be recognized over the two-year service period. The $25 allocated to the option to purchase Service B is deferred until Service B is transferred to Customer or the option expires.

13. Six months after executing the contract, Customer exercises its option to purchase two years of Service B for $300.

View A

14. Entity accounts for Customer's exercise of its option to purchase Service B as a continuation of the contract. The transaction price is updated to reflect the consideration received in exchange for Service B. The amount allocated to Service A, less any amounts previously recognized as revenue (for example, Entity would have recognized revenue of $18.75 for Service A when the option was exercised six months into the two-year contractual term), is recognized as revenue over the remainder of the two-year period over which Service A is transferred. The $300 of consideration related to service B is added to the amount previously allocated to the option to purchase Service B (that is, a total of $325) and is recognized as revenue over the two-year period over which Service B is transferred. In this example, none of the transaction price allocated to the material right had been recognized as revenue at the date the option was exercised by Customer.

15. Proponents of View A think that the exercise of a customer option is not a contract modification because it is not a change in the scope or price of a contract. Rather, proponents of View A think the exercise of a customer option is an exercise of an existing provision in the contract. Proponents of View A think that any additional consideration received or additional goods or services provided upon the exercise of a customer option were contemplated as part of the original contract, as evidenced by a portion of the transaction price being allocated to the customer option as a separate performance obligation.

View B

16. Entity accounts for Customer's exercise of its option to purchase Service B as a contract modification. Entity evaluates the contract modification guidance in paragraph 606-10-25-12 [20] and determines that the contract modification should not be accounted for as a separate contract because the price of the contract did not increase by an amount of consideration that reflects Entity's standalone selling price of Service B.

17. Entity must then evaluate the guidance in paragraph 606-10-25-13 [21] to determine how it should account for the modification. Depending on its evaluation of the guidance in paragraph 606-10-25-13 [21], Entity

may

be required to recognize a cumulative catch-up adjustment to revenue on the date of the modification. A cumulative catch-up adjustment would not be recognized under View A or, under paragraph 606-10-25-13(a) [21(a)] if the entity concludes that the remaining goods or services to be provided subsequent to the modification are distinct from those transferred to the customer prior to the modification. However, a cumulative catchup adjustment would be required if Entity accounts for the modification in accordance with paragraphs 606-10-25-13(b) or (c) [21(b) or (c)].

18. Proponents of View B think that any additional consideration or additional goods or services provided upon the exercise of a customer option represent a change in the price and scope of a contract and should be accounted for as a modification of the contract. Proponents of View B think the original goods or services are those promised in the contract, including any material right(s). They view the option, when exercised, as a change in the scope of the contract because the good or service was not contracted for in the original contract. Proponents of View B think the exercise of an option that did not provide the customer with a material right could in some cases be considered a contract modification (for example, adding a new service to an existing services contract) and do not think that conclusion should differ just because the option does, or does not, provide the customer with a material right.

View C

19. Entity treats the potential $300 additional consideration as variable consideration. That is, when it is probable that including the $300 in the transaction price would not result in a significant reversal of cumulative revenue recognized under the contract, Entity would include the amount in the transaction price and reallocate consideration between Service A and Service B on the basis of their original standalone selling prices.

20. Proponents of View C acknowledge that paragraph BC186 states that the transaction price should exclude consideration from the future exercise of options for additional goods or services or from future change orders. However, proponents of View C think that paragraph BC186 did not contemplate situations in which a customer may have the right to opt out of future transactions. For example, Customer may enter into a contract with Entity to purchase widgets. The terms of the contract are such that Customer receives a free widget from Entity upfront and will receive an additional 100 widgets each month for one year at a price that represents the standalone selling price of the widgets. Customer is not obligated to purchase the 100 widgets each month. That is, Customer may opt out of buying the widgets at any time. However, in this example, Customer is economically inclined to purchase widgets because it manufactures a product that is highly dependent on widgets. Proponents of View C think that Entity will be entitled to some amount of consideration from Customer and, therefore, should include some amount of Customer's future purchases in the transaction price of the contract if it is probable that the amount would not result in a significant reversal of cumulative revenue recognized under the contract. That is, proponents of View C think that Customer's monthly widget purchases are a form of variable consideration.

21. Opponents of View C do not think that Customer's monthly widget purchases are a form of variable considerations. Rather, opponents of View C think that paragraph BC186 is clear that the transaction price should exclude consideration from the future exercise of options. Opponents of View C think that, in the example in the paragraph above, Customer's ability to opt out of the monthly widgets renders any purchases of those widgets an option to which the guidance in paragraph BC186 would apply to those situations and would prohibit Entity from including the monthly widget sales to Customer in the transaction price of the contract.

Staff Analysis

22. The staff do not think View C is supported by the guidance in the new revenue standard because the discussion in paragraph BC186 seems to expressly preclude that view. However, the staff think that the guidance in the standard could be read to support either View A or View B as reasonable interpretations.

23. The staff observe that the nature of material rights can vary significantly from one entity to next. The staff think an entity will need to apply judgment to determine a practical approach to accounting for material rights, including deferring revenue when the right is granted and recognizing revenue as the future goods or services are transferred to the customer. An entity might also consider the practical expedient in paragraph 606-10-10-4[4] that permits an entity to apply the standard to a portfolio of similar contracts, rather than on an individual contract basis.

Issue 2: How should an entity evaluate whether a customer option that provides a material right includes a significant financing component?

24. The staff note that paragraph 606-10-32-15 [60] makes clear that an entity must consider the effects of the time value of money when determining the transaction price. This evaluation would include consideration of whether a significant financing component exists as a result of a material right (that is, the evaluation would be the same as for any other performance obligation). However, consistent with the evaluation of whether a significant financing component exists in any other contract (that is, one that does not provide a material right to the customer), an entity would consider the guidance in paragraphs 606-10-32-17 through 32-18 [62-63].

25. Paragraph 606-10-32-17(a) [62(a)] states that a contract would not have a significant financing component if a customer pays for a good or service in advance, and the timing of the transfer of those goods or services is at the discretion of the entity. Therefore, if the timing of when the customer will exercise its option is at the customer's discretion, no significant financing component would exist. Similarly, as a practical expedient, paragraph 606-10-32-18 [63] states that an entity need not adjust the promised amount of consideration for the effects of a significant financing component if the entity expects, at contract inception, that the period between when the entity transfers a promised good or service to a customer and when the customer pays for that good or service will be one year or less.

26. Absent applicability of the guidance in paragraphs 606-10-32-17(a) and 606-10-32-18 [62(a) and 63], a significant financing component may exist as a result of providing a material right for which an entity, in effect, has received advanced payment. Determining whether providing a material right results in a significant financing component will require the use of judgment and will depend on the specific facts and circumstances underlying the material right. Factors to be considered when evaluating whether a significant financing component exists will be discussed at the March 30, 2015 TRG meeting (TRG Agenda ref 30).

Issue 3: Over what period should an entity recognize a nonrefundable upfront fee?

Example

27. Entity charges a $50 one-time activation fee and agrees to provide Customer with services on a month-to-month basis at a price of $100 per month. Customer is under no obligation to continue to purchase the monthly service and Entity has not committed to any pricing levels for the service in future months. Since the activity of signing up Customer for service does not result in the transfer of a good or service, it does not represent an additional promised service. Rather, the activation fee is an advance payment for Entity's services and should, therefore, be deferred and recognized as the future service is provided. Entity's average customer life is two years.

Staff Analysis

28. The staff notes that the period over which the activation fee will be recognized depends on whether the activation fee provides the customer with a material right with respect to renewing Entity's services. As previously discussed at the October 2014 TRG meeting, when determining whether a nonrefundable upfront fee provides a material right, Entity would consider both quantitative and qualitative factors. For example, Entity would consider whether the renewal price that Customer will pay (that is, $100 per month) compared with the price that a new customer would pay for the same service (that is, $150, consisting of a $50 activation fee and $100 monthly service) provides Customer with a material right. Entity also would consider the availability and pricing of service alternatives (for example, whether Customer could obtain substantially equivalent services from another provider without paying the activation fee). Entity's average customer life also might be an indication of whether the activation fee provides a material right. That is, an average customer life that extends well beyond the one month contractual period might be an indication that the activation fee incentivizes Entity's customers to continue services because those customers would not incur an activation fee that they may otherwise incur if they switch service providers.

29. If Entity concludes that the activation fee provides a material right, the fee would be recognized over the service periods during which Customer is expected to benefit from not having to pay an activation fee upon renewal of service. Determining the expected period of benefit often will require judgment.

30. Conversely, if Entity concludes that the activation fee does not provide the customer with a material right, the activation fee is, in effect, an advance payment solely on the contracted services (for example, the one-month contract term). Consequently, Entity would recognize the transaction price (that is, $150 comprised of the service and activation fees) as revenue as those services are provided in accordance with paragraph 606-10-55-51 [B49].

Other stakeholder view

31. Under another interpretation communicated to the staff, Entity concludes that the activation fee of $50 does not provide the customer with a material right in the context of $2,450 in total consideration that would be paid by the customer over Entity's average customer relationship period ($100 per month x 24 months + $50 activation fee). Entity then recognizes the $50 activation fee over the one-month contractual service period. The staff do not think this is a reasonable interpretation of the guidance. Under this interpretation, Entity uses an implied contract term of 24 months to support a conclusion that the activation fee does not provide the customer with a material right, but uses only the fixed contract term of one month to recognize that activation fee. The staff do not think it is a reasonable application of the guidance to use two different contract terms for purposes of this evaluation.

Questions for the TRG Members

1. Do the TRG members agree with the staff's interpretations in this paper?

2. Are there any related potential issues that are not included in this paper?

Appendix A: Relevant Accounting Guidance

Contract modifications

32. Paragraph 606-10-25-10 [18] states that a contract modification is a change in the scope or price (or both) of a contract that is approved by the parties to the contract. Paragraphs 606-10-25-11 through 25-13 [19–21] provide guidance on the accounting for various contract modifications.

Determining the Transaction Price

33. Paragraph 606-10-32-2 [47] states that the transaction price is the amount of consideration to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer, excluding amounts collected on behalf of third parties (for example, some sales taxes). To determine the transaction price, an entity should consider the effects of variable consideration, constraining estimates of variable consideration, the existence of a significant financing component, noncash consideration, and consideration payable to the customer.

34. Paragraph BC186 explains that the transaction price should include only amounts (including variable amounts) to which the entity has rights under the present contract. For example, the transaction price does not include estimates of consideration from the future exercise of options for additional goods or services or from future change orders. Until the customer exercises the option or agrees to the change order, the entity does not have a right to consideration.

Variable Consideration

35. If the consideration promised in a contract includes a variable amount, an entity is required to estimate the amount of consideration to which the entity will be entitled in exchange for transferring the promised goods or services to a customer.

36. Paragraph 606-10-32-6 [51] states that an amount of consideration can vary because of discounts, rebates, refunds, credits, price concessions, incentives, performance bonuses, penalties, or other similar items. Paragraph BC191 explains that consideration can be variable even in cases in which the stated price in the contract is fixed. This is because the entity may be entitled to the consideration only upon the occurrence or nonoccurrence of a future event. Consider, for example, a fixed-price service contract in which the customer pays upfront and the terms of the contract provide the customer with a full refund of the amount paid if the customer is dissatisfied with the service at any time. In those cases, the consideration is variable because the entity might be entitled to all of the consideration or none of the consideration if the customer exercises its right to a refund.

Existence of a Significant Financing Component

37. In determining the transaction price, paragraph 606-10-32-15 [60] requires an entity to adjust the promised amount of consideration for the effects of the time value of money if the timing of payments agreed to by the parties to the contract (either explicitly or implicitly) provides the customer or the entity with a significant benefit of financing the transfer of goods or services to the customer. In those circumstances, the contract contains a significant financing component. A significant financing component may exist regardless of whether the promise of financing is explicitly stated in the contract or implied by the payment terms agreed to by the parties to the contract.

38. Paragraph 606-10-32-17 [62] states that a contract with a customer would not have a significant financing component if any of the following factors exist:

(a) The customer paid for the goods or services in advance, and the timing of the transfer of those goods or services is at the discretion of the customer.

(b) A substantial amount of the consideration promised by the customer is variable, and the amount or timing of that consideration varies on the basis of the occurrence or nonoccurrence of a future event that is not substantially within the control of the customer or the entity (for example, if the consideration is a sales-based royalty).

(c) The difference between the promised consideration and the cash selling price of the good or service (as described in paragraph 606-10-32-16 [61]) arises for reasons other than the provision of finance to either the customer or the entity, and the difference between those amounts is proportional to the reason for the difference. For example, the payment terms might provide the entity or the customer with protection from the other party failing to adequately complete some or all of its obligations under the contract.

39. As a practical expedient, paragraph 606-10-32-18 [63] states that an entity need not adjust the promised amount of consideration for the effects of a significant financing component if the entity expects, at contract inception, that the period between when the entity transfers a promised good or service to a customer and when the customer pays for that good or service will be one year or less.

Allocation of Variable Consideration

40. Paragraph 606-10-32-39 [84] states that variable consideration that is promised in a contract may be attributable to the entire contract or to a specific part of the contract, such as either of the following:

(a) One or more, but not all, performance obligations in the contract (for example, a bonus may be contingent on an entity transferring a promised good or service within a specified period of time)

(b) One or more, but not all, distinct goods or services promised in a series of distinct goods or services that forms part of a single performance obligation in accordance with paragraph 606-10-25-14(b) [22(b)] (for example, the consideration promised for the second year of a two-year cleaning service contract will increase on the basis of movements in a specified inflation index).

41. Paragraph 606-10-32-40 [85] requires that an entity allocate a variable amount (and subsequent changes to that amount) entirely to a performance obligation or to a distinct good or service that forms part of a single performance obligation in accordance with paragraph 606-10-25-14(b) [22(b)] if both of the following criteria are met:

(a) The terms of a variable payment relate specifically to the entity's efforts to satisfy the performance obligation or transfer the distinct good or service (or to a specific outcome from satisfying the performance obligation or transferring the distinct good or service).

(b) Allocating the variable amount of consideration entirely to the performance obligation or the distinct good or service is consistent with the allocation objective in paragraph 606-10-32-28 [73] when considering all of the performance obligations and payment terms in the contract.

Changes in the Transaction Price

42. Paragraph 606-10-32-42 [87] acknowledges that after contract inception, the transaction price can change for various reasons, including the resolution of uncertain events or other changes in circumstances that change the amount of consideration to which an entity expects to be entitled in exchange for the promised goods or services.

43. Paragraph 606-10-32-43 [88] requires an entity to allocate any subsequent changes in the transaction price to the performance obligations in the contract on the same basis as at contract inception. Consequently, an entity shall not reallocate the transaction price to reflect changes in standalone selling prices after contract inception.

44. Paragraph 606-10-32-44 [89] states that an entity shall allocate a change in the transaction price entirely to one or more, but not all, performance obligations or distinct goods or services promised in a series that forms part of a single performance obligation in accordance with paragraph 606-10-25-14(b) [22(b)] only if the criteria in paragraph 606-10-32-40 [85] on allocating variable consideration are met.

45. Paragraph 606-10-32-45 [90] requires an entity to account for a change in the transaction price that arises as a result of a contract modification in accordance with paragraphs 606-10-25-10 through 25-13 [18–21]. However, for a change in the transaction price that occurs after a contract modification, an entity shall apply paragraphs 606-10-32-42 through 32-44 [87–89] to allocate the change in the transaction price in whichever of the following ways is applicable:

(a) An entity shall allocate the change in the transaction price to the performance obligations identified in the contract before the modification if, and to the extent that, the change in the transaction price is attributable to an amount of variable consideration promised before the modification and the modification is accounted for in accordance with paragraph 606-10-25-13(a) [21(a)].

(b) In all other cases in which the modification was not accounted for as a separate contract in accordance with paragraph 606-10-25-12 [20], an entity shall allocate the change in the transaction price to the performance obligations in the modified contract (that is, the performance obligations that were unsatisfied or partially unsatisfied immediately after the modification).

Customer Options for Additional Goods or Services

46. If an entity determines that a customer option provides a customer with a material right and, therefore, gives rise to a performance obligation, paragraph 606-10-55-44 [B42] requires an entity to allocate the transaction price to performance obligations on a relative standalone selling price basis. If the standalone selling price for a customer's option is not directly observable, an entity is required to estimate it.

Nonrefundable Upfront Fees (and Some Related Costs)

47. The determination of whether an option provides a material right may affect the timing of revenue recognition for a nonrefundable upfront fee. Paragraph 606-10-55-51 [B49] states that an entity that charges its customers a nonrefundable upfront fee at or near contract inception must first assess whether the fee relates to the transfer of a promised good or service. A nonrefundable upfront fee that does not relate to a promised good or service is considered an advance payment for future goods and services. The period over which the fee is recognized may extend beyond the initial contractual period if the entity grants the customer the option to renew the contract and that option provides the customer with a material right as described in paragraph 606-10-55-42 [B40].

___________ The IASB is the independent standard-setting body of the IFRS Foundation, a not-for-profit corporation promoting the adoption of IFRSs. For more information visit www.ifrs.org

The Financial Accounting Standards Board (FASB) is an independent standard-setting body of the Financial Accounting Foundation, a not-for-profit corporation. The FASB is responsible for establishing Generally Accepted Accounting Principles (GAAP), standards of financial accounting that govern the preparation of financial reports by public and private companies and not-for-profit organizations in the United States and other jurisdictions. For more information visit www.fasb.org

1 IFRS 15 references are included in "[XX]" throughout this paper.

Copyright #year# by Financial Accounting Foundation, Norwalk, Connecticut.