STAFF PAPER | April 18, 2016 |

Project | Transition Resource Group for Revenue Recognition |

Paper topic | Considering Class of Customer When Evaluating Whether a Customer Option Gives Rise to a Material Right |

CONTACT(S) | Mark Barton | | +1 203 956 3467 |

This paper has been prepared for discussion at a public meeting of the Transition Resource Group for Revenue Recognition. It does not purport to represent the views of any individual members of the board or staff. Comments on the application of U.S. GAAP do not purport to set out acceptable or unacceptable application of U.S. GAAP. Stakeholders are strongly encouraged to listen to feedback about this staff paper from TRG members and Board members during the TRG meeting and to read the meeting summary, which will be prepared by the staff after the meeting. |

Purpose

1. Some stakeholders informed the staff that there are questions about the guidance in Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers (Topic 606) (the new revenue standard), for evaluating whether a customer option to acquire additional goods or services gives rise to a material right. Specifically, those stakeholders question how the class of customer is considered in that evaluation.

2. This paper summarizes the potential implementation issue that was reported to the staff. The staff will seek input from members of the Transition Resource Group for Revenue Recognition (TRG) on the potential implementation issue.

Background

3. Customer options to acquire additional goods or services for free or at a discount come in many forms, including sales incentives, customer award credits (or points), contract renewal options, or other discounts on future goods or services. The new revenue standard requires an entity to evaluate whether a customer option to acquire goods or services gives rise to a material right and, thus, a performance obligation.

4. At its October 31, 2014 meeting, the TRG discussed the types of factors that should be considered when evaluating whether a customer option gives rise to a material right (

TRG Agenda Ref No. 6). The TRG discussed several examples to illustrate those factors, including a loyalty program, a discount voucher, a nonrefundable upfront fee and a "buy three and get one free" program. Most TRG members agreed that the evaluation of whether a customer option provides a material right should consider relevant transactions with the customer (that is, past, current, and future transactions) and should consider both quantitative and qualitative factors, including whether the right accumulates.

5. Subsequent to the October 2014 TRG meeting, some stakeholders raised questions about the accounting for a customer option that provides a material right. Accordingly, at its March 30, 2015 meeting, the TRG discussed how an entity should account for a customer's exercise of a material right, how an entity should evaluate whether a customer option that provides a material right includes a significant financing component, and over what period an entity should recognize a nonrefundable upfront fee (

TRG Agenda Ref No. 32). The issues discussed at the March 2015 TRG meeting are unrelated to the potential implementation issue addressed in this paper and are referenced for informational purposes only.

Accounting Guidance

6. The relevant accounting guidance has been included in Appendix A of this paper.

Implementation question: How is the class of customer considered when evaluating whether a customer option gives rise to a material right?

7. Some stakeholders have informed the staff that there are differing views about how the class of customer is considered when evaluating whether a customer option gives rise to a material right. This section of the paper includes the staff's views on how the class of customer is considered. However, an entity will need to apply judgment based on its own facts and circumstances to determine whether a customer option gives rise to a material right.

8. Paragraph 606-10-55-42 explains that a customer option to acquire additional goods or services gives rise to a performance obligation only if the option provides a material right to the customer that it would not receive without entering into the contract (for example, a discount that is incremental to the range of discounts typically given for those goods or services to that class of customer in that geographical area or market). Paragraph 55-42 further explains that a customer option that provides a material right to a customer, in effect, represents an advanced payment by the customer for future goods or services.

9. Paragraph 606-10-55-43 states that if a customer has the option to acquire an additional good or service at a price that would reflect the standalone selling price for that good or service, that option does not provide the customer with a material right even if the option can be exercised only by entering into a previous contract. Rather, the entity has made a marketing offer that it should account for when the customer exercises the option to purchase the additional goods or services. Stated differently, paragraph 55-43 is intended to make clear that a customer option to acquire additional goods or services would not give rise to a material right if a customer could execute a separate contract to obtain the same goods or services at the same price.

10. Paragraph 606-10-32-33 states that when estimating a standalone selling price, an entity should consider all available information, including information about the customer or class of customer.

11. Paragraph BC386 explains that the purpose of the guidance in paragraphs 606-10-55-42 through 55-43 is to distinguish between:

a. an option that the customer pays for as part of an existing contract (that is, a customer pays in advance for future goods or services), and

b. a marketing or promotional offer that the customer did not pay for and, although made at the time of entering into a contract, is not part of the contract (that is, an effort by an entity to obtain future contracts with a customer).

12. Stated differently, the guidance in paragraphs 606-10-55-42 through 55-43 is intended to make clear that customer options that would exist independently of an existing contract with a customer do not constitute performance obligations in that existing contract.

13. For some contracts, determining whether or not a contract includes an option that provides a material right will be clear. However, in other cases the determination will require significant judgment. Similar judgment is required under current GAAP. For example, under current GAAP some entities might need to apply significant judgment to determine whether a discount offered on future goods or services is significant and incremental to the range of discounts reflected in the pricing of other elements in a contract and to the range of discounts typically given in comparable transactions.

14. An entity also will need to consider any disclosures required under the new revenue standard related to its determination of whether a customer option gives rise to a material right. For example, the new revenue standard requires an entity to disclose certain information about significant judgments made in applying the guidance in the new revenue standard. It also requires an entity to disclose certain information about its performance obligations and how the transaction price has been allocated to those performance obligations, including disclosures related to how an entity estimated the standalone selling prices of its performance obligations.

15. The following examples illustrate the staff's views on how the class of customer is considered when evaluating whether a customer option gives rise to a material right.

Example 1 – Preferred customer pricing

16. Professional Consultants LLP (PCon) is one of the largest consulting firms in the world. PCon hires only the best and brightest professionals in the industry and typically charges its customers $1,000 per hour for consulting services. Goody Corporation (Goody) owns and operates a chain of bakeries across the United States. Goody currently has a long-term master services agreement with a consulting firm that will expire in the next year. Goody has requested that its current consulting firm and several other firms, including PCon, submit proposals for a new long-term master services agreement.

17. PCon knows that Goody and its current consulting firm entered into several contracts under the existing master services agreement for projects that required a significant number of consulting hours. PCon submits a proposal to provide Goody with an unspecified amount of consulting services under a master services agreement for $800 per hour even though PCon has provided consulting services to Goody in the past at a rate of $1,000 per hour. None of PCon's prior contracts with Goody included a material right (that is, there are no prior contracts between PCon and Goody that would have created an expectation for Goody to receive favorable pricing in the future or that would have created an expectation for PCon to provide favorable pricing in the future).

18. After considering all proposals, Goody decides to enter into a long-term master services agreement with PCon. The agreement does not specify the scope of service to be provided by PCon, but specifies that the price per hour for any consulting services provided under the master services agreement will remain at $800 throughout the duration of the agreement (that is, each time Goody enters into a contract with PCon for a consulting project, the scope of services are separately negotiated, but the agreed upon hourly rate of $800 is used to determine the price). Goody subsequently enters into a contract with PCon to perform consulting services for a specific project over the next 6 months under the terms in the master services agreement (that is, PCon will provide consulting services for $800 per hour).

Staff Analysis

19. Although PCon agrees to charge Goody a rate that is less than what it typically would charge a customer (or had charged Goody in the past), the staff's view is that the contract between PCon and Goody does not include a material right. This is because the hourly rate that is offered to Goody in each contract exists independently (for example, the hourly rate that Goody would be charged if it enters into a contract for a second specific project would be the same even if it had not entered into the first contract). Rather, the pricing offered by PCon in this example is a marketing offer made in an effort to obtain future contracts with Goody.

20. In this example, PCon does not need to consider Goody's class of customer because the price at which PCon will provide consulting services to Goody (that is, $800 per hour) is not dependent on any existing or prior contracts with Goody. The staff included this example to illustrate a fact pattern in which future services are offered at a "discount," but in which it is clear that the "discount" does not give rise to a material right.

Example 2 – Significant discount on future purchase

21. Ziggy's Electronics (Ziggy) owns and operates several retail electronics stores in New York City. Ziggy currently provides customers who purchase a 50 inch television with a coupon for 50% off the purchase of one new Supersonic stereo system. Ziggy typically sells a 50 inch television and the stereo system for $1,000 each. The coupon is redeemable only at one of Ziggy's stores and must be redeemed within 1 year of purchasing the television. Ziggy has never offered a discount of this magnitude to a customer that does not purchase a television (or an item of similar value).

22. Janet recently graduated from college and moved to New York City. Janet is in need of a television for her new apartment and decides to purchase a 50 inch television from Ziggy. At the time Janet purchases the television, she receives a coupon for a 50% discount on the Supersonic stereo system, but chooses not to redeem the coupon at the same time she purchases the television.

Staff Analysis

23. When evaluating whether the contract between Ziggy and Janet includes a material right, Ziggy evaluates whether Janet's option to purchase a Supersonic stereo system at a 50% discount exists independently of the existing contract with Janet (that is, the contract to purchase a television).

24. Assume Martha is Janet's next-door neighbor. Martha is not in the market for a new television because she recently purchased a television online from one of Ziggy's competitors. However, Martha visits the local Ziggy store where Janet purchased her television. The sales associate standing at the front of the store handed every person that walked through the door a coupon for 5% off the purchase of a Supersonic stereo system (which cannot be combined with any other offer).

25. In evaluating whether the discount offered to Janet exists independently of Janet's existing contract to purchase a television, Ziggy should compare the discount offered to Janet (that is, 50%) with the discount typically offered to customers similar to Martha (that is, Ziggy should compare the discount offered to Janet with the discount typically offered to a similar customer that receives the discount independent of a prior contract with Ziggy).

26. Because the objective of the guidance in paragraphs 606-10-55-42 through 55-43 is to determine whether a customer option exists independently of an existing contract with a customer, it would not be appropriate for Ziggy to compare the discount offered to Janet with a discount offered to another customer that purchased a television and received a 50% off coupon for the stereo. Doing so would not help Ziggy determine whether Janet would have received the discount on the stereo system without entering into the contract to purchase the television.

27. The discounts offered to Janet and typically offered to customers like Martha (that is, customers who are offered a discount independent of a prior contract with Ziggy) are not comparable. Rather, Janet is receiving an incremental discount that she would not have received had she not entered into a contract to purchase a television. In the staff's view, the incremental discount offered to Janet in connection with her purchase of a television is a material right.

Example 3 – Volume discounts

28. Sprocket Corporation (Sprocket) manufactures component parts that have various uses to multiple customers. Assume for purposes of this fact pattern that the parts are interchangeable and not customized for any particular customer. Sprocket enters into a long-term master services agreement to provide unspecified volumes of parts to Jetson Corporation (Jetson). The price of the parts in a subsequent year is dependent on the volume of purchases Jetson makes in the current year. Sprocket charges Jetson $1.00 per part in Year 1 and the contract stipulates that if Jetson's purchase volume in Year 1 exceeds 100,000 parts, the price per part will decrease to $0.90 in Year 2. The terms of Sprocket's contract with Jetson, including the reduced price in Year 2 if the purchasing threshold in Year 1 is met, are similar to the terms offered to many of its customers. Early in Year 1, Jetson enters into a contract with Sprocket to purchase 8,000 parts. Jetson is required to pay $1.00 for each of those 8,000 parts.

Staff Analysis

29. When evaluating whether the contract between Sprocket and Jetson includes a material right, Sprocket first evaluates whether Jetson's option to receive a $0.10 per part discount in Year 2 exists independently of the existing contract (that is, the contract(s) to purchase parts in Year 1) with Jetson.

30. To make this evaluation, Sprocket compares the discount offered to Jetson with the discount typically offered to a similar high-volume customer that receives a discount independent of a prior contract with Sprocket.

31. Assume Astro Corporation (Astro) is an existing customer that places a single order with Sprocket for 105,000 parts. Astro has purchased parts from Sprocket in the past, but none of its prior contracts with Sprocket created an expectation to purchase parts in the future at a specified price (and did not create an expectation for Sprocket to sell parts in the future at a specified price).

32. In evaluating whether the discount offered to Jetson exists independently of the existing contract, Sprocket should compare the price per part offered to Jetson in Year 2 (that is, $0.90) with the price charged to customers similar to Astro (that is, Sprocket should compare the price offered to Jetson in Year 2 with the price typically offered to a similar high-volume customer that is offered a price independent of a prior contract with Sprocket).

33. Because the objective of the guidance in paragraphs 606-10-55-42 through 55-43 is to determine whether a customer option exists independently of an existing contract with a customer, it would not be appropriate for Sprocket to compare the price offered to Jetson in Year 2 with offers to other customers that receive pricing that is contingent on the volume of purchases in a prior year. Doing so would not help Sprocket determine whether Jetson would have been offered the price in Year 2 had it not entered into the contract(s) to purchase parts with Sprocket in Year 1.

34. If the price that Sprocket offered to Jetson in Year 2 and the price typically offered to customers like Astro (that is, a similar high-volume customer that is offered a price independent of a prior contract with Sprocket) are comparable, this might indicate that the price offered to Jetson exists independently of the existing contract (that is, the price offered to Jetson does not include a discount that is incremental to the discount typically offered to a similar high-volume customer). If the price Sprocket charged Jetson and Astro are not comparable, this might indicate that a portion of the price Jetson pays for parts in Year 1 is a prepayment for the parts purchased in Year 2.

35. In the staff's view, significant judgment will be required to determine whether the prices charged to Jetson and customers such as Astro are comparable, whether Jetson and Astro are comparable customers, and whether any difference in price is significant. The staff is not in a position to reach broad conclusions about these types of fact patterns because there are many variations of contracts and variations in facts and circumstances that can impact the conclusion in each fact pattern.

36. If Sprocket concludes that the contract with Jetson includes a material right, it would need to use significant judgment to account for that material right (for example, to estimate the amount of the transaction price that should be allocated to the material right and the period in (or over) which the performance obligation associated with material right should be recognized as revenue).

37. The staff reminds stakeholders that the new revenue standard includes a practical expedient in paragraph 606-10-10-4 that permits an entity to apply the guidance to a portfolio of contracts or performance obligations in certain circumstances. This practical expedient might simplify the accounting for contracts that include material rights.

38. The staff also reminds stakeholders that the new revenue standard includes disclosure requirements about the judgments, and changes in the judgments, made in applying the guidance that significantly affect the determination of the amount and timing of revenue from contracts with customers.

Example 4 – Tier status

39. Dream Airlines (Dream) offers a "tier status" program that identifies its customers as Bronze, Silver or Platinum customers based on historical travel volume. Customers in those tiers have the option to receive status benefits (that is, goods or services offered at a discounted price) when the customer purchases a future ticket within a specified period (that is, when the customer enters into a future contract with Dream). However, not all of the benefits require the customer to make a future ticket purchase (for example, benefits might include an annual $250 gift card to a luxury store or tickets to a tennis match).

40. Customers in the Bronze tier have the option to receive a range of status benefits, including checked bags and priority check-in for no incremental fee beyond the price of the ticket. Customers in the higher tiers have the option to receive additional status benefits, including upgrades to business class seating (if available and at Dream's discretion), airport lounge access, and a companion ticket (for certain flights) for no incremental fee beyond the price of a ticket. Customers in a higher tier are more likely to receive upgrades to business class seating for no incremental fee when requested than customers in a lower tier. Dream typically charges a customer without tier status an incremental fee (that is, a fee in addition to the price charged for the ticket) to check a bag, to upgrade to business class seating, and to access the airport lounge.

41. Throughout the year, Dream evaluates a customer's purchasing history against the status program criteria to determine the tier for which the customer qualifies. Status tiers must be achieved by the end of the year. If a status tier is not met, the progress toward achieving a tier restarts in the following year. Customers who have a larger volume of ticket purchases earn a higher status for the remainder of the current year and all of the next year. Some customers maintain status for many consecutive years and others fall and in out of status from one year to the next.

42. Dream also offers a loyalty mile program that allows its customers to accumulate miles over an extended period of time (that is, the loyalty mile program does not reset on an annual basis like the tier status program). Loyalty miles can be redeemed for merchandise, vouchers for free hotel rooms, or free airline tickets. Many of the items that can be redeemed for loyalty miles do not require a customer to purchase an additional airline ticket. Dream has concluded that its loyalty miles program provides its customers with a material right. The loyalty miles program has been excluded from the staff's analysis below about whether Dream's tier status program provides the customer with a material right.

Staff Analysis

43. When evaluating whether a contract (that is, a ticket purchase) with a customer in its tier status program includes a material right, Dream evaluates whether a customer's option to receive free or discounted goods or services in the future exists independently of the existing contract (that is, independent of the ticket sale for the current flight).

44. To make this evaluation, Dream compares the price it charges a customer in a certain tier for the flight and the other status benefits (for example, an upgrade to business class seating for which there was no incremental fee) to the price a similar customer who does not have a prior contract with Dream that created an expectation to receive status benefits for a period of time (or that would have created an expectation for Dream to provide status benefits in the future for a specified period of time) would pay for the same goods and services (for example, the price a customer that is not in the tier status program would pay for a flight and a last minute upgrade to business class seating).

45. Assume George is a retired accountant who spends his time traveling the world. George is a loyal Dream customer and has achieved Platinum status. Lola is a retired attorney who, like George, is a frequent traveler. However, Lola is a loyal customer of Luxury Airlines (Luxury), one of Dream's competitors. Lola has achieved Platinum status in Luxury's tier status program, which has similar requirements and status benefits as the Dream program. Lola has never purchased a ticket for a Dream flight.

46. In evaluating whether the status benefits (that is, goods or services offered at a discounted price) offered to George exist independently of the existing contract, Dream could compare the status benefits provided to George with those it would provide Lola and other similar customers (that is, Dream could compare the status benefits it offers George with the status benefits it would offer a similar customer who is offered the benefits independent of a prior contract with Dream). For example, Dream could consider whether and how frequently it matches the status benefits that a customer like Lola receives on another airline. Dream should consider whether it would offer Lola (or a similar customer) those status benefits only during a short trial period during which Lola must purchase tickets or lose status on Dream or whether Dream would be willing to give Lola those status benefits for a longer period of time in an effort to encourage Lola to make future purchases.

47. Comparing the status benefits Dream offers to George with those offered to Lola is one of several ways that Dream could evaluate whether the status benefits offered to George exist independently of the existing contract with George. For example, Dream also could consider whether it would continue to offer George status benefits for the subsequent year even if he failed to travel enough in the current year to maintain his tier status, whether it would charge George a fee to maintain his status, or whether it would take away George's status benefits. Dream also could consider whether and how frequently it would offer status benefits to a customer who demonstrates that he or she is a frequent traveler through other means (for example, Dream might offer status benefits to a customer who has status at a luxury hotel chain in an effort to obtain future contracts with that customer, despite the customer not previously making a purchase with Dream).

48. If the status benefits offered to George and those that would be provided to customers like Lola (that is, a customer who is offered benefits independent of a prior contract with Dream) are comparable, this might indicate that the status benefits offered to George exist independently of the existing contact. If the status benefits offered to George and customers like Lola are not comparable, this may indicate that a portion of the price George paid for tickets in the prior year is a prepayment for the status benefits he is offered in the subsequent year. Dream's evaluation of its contract with George may be reflective of whether its contracts with other Platinum members include a material right (that is, it may not be necessary for Dream to perform the evaluation on a contract-by-contract basis).

49. Because the objective of the guidance in paragraphs 606-10-55-42 through 55-43 is to determine whether a customer option exists independently of an existing contract with a customer, it would not be appropriate for Dream to compare the status benefits offered to George with benefits offered to customers that are offered similar benefits that may be the result of prior contracts with Dream (that is, Dream should not compare George with other Platinum members). Doing so would not help Dream determine whether George would have been offered the status benefits had he not entered into the prior contracts with Dream (that is, whether the option to receive future status benefits is an option that accumulated based on prior ticket purchases).

50. In the staff's view, significant judgment will be required to determine whether the status benefits offered to George and customers like Lola are comparable, whether George and Lola are comparable customers, and whether any difference in benefits are significant. The staff is not in a position to reach broad conclusions about these types of fact patterns because there are many variations of contracts and variations in facts and circumstances that can impact the conclusion in each fact pattern.

51. The staff's analysis includes some considerations that are relevant to evaluating whether the contracts in this example include a material right. Other considerations will be relevant in other fact patterns. In addition, the relative importance that an entity places on each relevant consideration will vary from one consideration to the next on the basis of the facts and circumstances.

52. If Dream concludes that the contract with George includes a material right, it would need to use significant judgment to account for that material right (for example, to estimate the amount of the transaction price that should be allocated to the material right and the period in (or over) which the performance obligation associated with material right should be recognized as revenue).

53. As with Example 3 in this paper, the staff reminds stakeholders that the new revenue standard includes: (a) a practical expedient in paragraph 606-10-10-4 that permits an entity an entity to apply the guidance to a portfolio of contracts or performance obligations in certain circumstances and (b) disclosure requirements about significant judgments.

Question for the TRG Members |

1. Do the TRG members agree with the staff's views in this paper? |

Appendix A: Relevant Accounting Guidance

>Allocating the Transaction Price to Performance Obligations

> > Allocation Based on Standalone Selling Prices

606-10-32-31 To allocate the transaction price to each performance obligation on a relative standalone selling price basis, an entity shall determine the standalone selling price at contract inception of the distinct good or service underlying each performance obligation in the contract and allocate the transaction price in proportion to those standalone selling prices.

606-10-32-32 The standalone selling price is the price at which an entity would sell a promised good or service separately to a customer. The best evidence of a standalone selling price is the observable price of a good or service when the entity sells that good or service separately in similar circumstances and to similar customers. A contractually stated price or a list price for a good or service may be (but shall not be presumed to be) the standalone selling price of that good or service.

606-10-32-33 If a standalone selling price is not directly observable, an entity shall estimate the standalone selling price at an amount that would result in the allocation of the transaction price meeting the allocation objective in paragraph 606-10-32-28. When estimating a standalone selling price, an entity shall consider all information (including market conditions, entity-specific factors, and information about the customer or class of customer) that is reasonably available to the entity. In doing so, an entity shall maximize the use of observable inputs and apply estimation methods consistently in similar circumstances.

>Implementation Guidance

> > Customer Options for Additional Goods or Services

606-10-55-41 Customer options to acquire additional goods or services for free or at a discount come in many forms, including sales incentives, customer award credits (or points), contract renewal options, or other discounts on future goods or services.

606-10-55-42 If, in a contract, an entity grants a customer the option to acquire additional goods or services, that option gives rise to a performance obligation in the contract only if the option provides a material right to the customer that it would not receive without entering into that contract (for example, a discount that is incremental to the range of discounts typically given for those goods or services to that class of customer in that geographical area or market). If the option provides a material right to the customer, the customer in effect pays the entity in advance for future goods or services, and the entity recognizes revenue when those future goods or services are transferred or when the option expires.

606-10-55-43 If a customer has the option to acquire an additional good or service at a price that would reflect the standalone selling price for that good or service, that option does not provide the customer with a material right even if the option can be exercised only by entering into a previous contract. In those cases, the entity has made a marketing offer that it should account for in accordance with the guidance in this Topic only when the customer exercises the option to purchase the additional goods or services.

606-10-55-44 Paragraph 606-10-32-29 requires an entity to allocate the transaction price to performance obligations on a relative standalone selling price basis. If the standalone selling price for a customer's option to acquire additional goods or services is not directly observable, an entity should estimate it. That estimate should reflect the discount that the customer would obtain when exercising the option, adjusted for both of the following:

a. Any discount that the customer could receive without exercising the option

b. The likelihood that the option will be exercised.

606-10-55-45 If a customer has a material right to acquire future goods or services and those goods or services are similar to the original goods or services in the contract and are provided in accordance with the terms of the original contract, then an entity may, as a practical alternative to estimating the standalone selling price of the option, allocate the transaction price to the optional goods or services by reference to the goods or services expected to be provided and the corresponding expected consideration. Typically, those types of options are for contract renewals.

>Illustrations

> > Customer Options for Additional Goods or Services

606-10-55-335 Examples 49–52 illustrate the guidance in paragraphs 606-10-55-41 through 55-45 on customer options for additional goods or services. Example 50 illustrates the guidance in paragraphs 606-10-25-19 through 25-21 on identifying performance obligations. Example 52 illustrates a customer loyalty program. That Example may not apply to all customer loyalty arrangements because the terms and conditions may differ. In particular, when there are more than two parties to the arrangement, an entity should consider all facts and circumstances to determine the customer in the transaction that gives rise to the award credits.

> > > Example 49—Option That Provides the Customer with a Material Right (Discount Voucher)

606-10-55-336 An entity enters into a contract for the sale of Product A for $100. As part of the contract, the entity gives the customer a 40 percent discount voucher for any future purchases up to $100 in the next 30 days. The entity intends to offer a 10 percent discount on all sales during the next 30 days as part of a seasonal promotion. The 10 percent discount cannot be used in addition to the 40 percent discount voucher.

606-10-55-337 Because all customers will receive a 10 percent discount on purchases during the next 30 days, the only discount that provides the customer with a material right is the discount that is incremental to that 10 percent (that is, the additional 30 percent discount). The entity accounts for the promise to provide the incremental discount as a performance obligation in the contract for the sale of Product A.

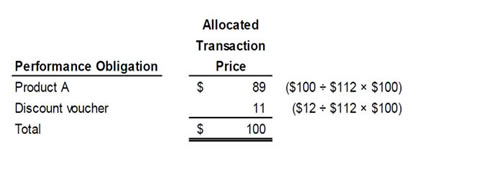

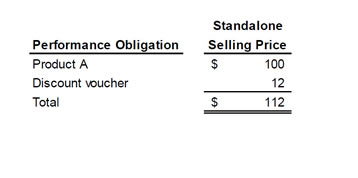

606-10-55-338 To estimate the standalone selling price of the discount voucher in accordance with paragraph 606-10-55-44, the entity estimates an 80 percent likelihood that a customer will redeem the voucher and that a customer will, on average, purchase $50 of additional products. Consequently, the entity's estimated standalone selling price of the discount voucher is $12 ($50 average purchase price of additional products × 30 percent incremental discount × 80 percent likelihood of exercising the option). The standalone selling prices of Product A and the discount voucher and the resulting allocation of the $100 transaction price are as follows:

606-10-55-339 The entity allocates $89 to Product A and recognizes revenue for Product A when control transfers. The entity allocates $11 to the discount voucher and recognizes revenue for the voucher when the customer redeems it for goods or services or when it expires.

> > > Example 50—Option That Does Not Provide the Customer with a Material Right (Additional Goods or Services)

606-10-55-340 An entity in the telecommunications industry enters into a contract with a customer to provide a handset and monthly network service for two years. The network service includes up to 1,000 call minutes and 1,500 text messages each month for a fixed monthly fee. The contract specifies the price for any additional call minutes or texts that the customer may choose to purchase in any month. The prices for those services are equal to their standalone selling prices.

606-10-55-341 The entity determines that the promises to provide the handset and network service are each separate performance obligations. This is because the customer can benefit from the handset and network service either on their own or together with other resources that are readily available to the customer in accordance with the criterion in paragraph 606-10-25-19(a). In addition, the handset and network service are separately identifiable in accordance with the criterion in paragraph 606-10-25-19(b) (on the basis of the factors in paragraph 606-10-25-21).

606-10-55-342 The entity determines that the option to purchase the additional call minutes and texts does not provide a material right that the customer would not receive without entering into the contract (see paragraph 606-10-55-43). This is because the prices of the additional call minutes and texts reflect the standalone selling prices for those services. Because the option for additional call minutes and texts does not grant the customer a material right, the entity concludes it is not a performance obligation in the contract. Consequently, the entity does not allocate any of the transaction price to the option for additional call minutes or texts. The entity will recognize revenue for the additional call minutes or texts if and when the entity provides those services.

> > > Example 51—Option That Provides the Customer with a Material Right (Renewal Option)

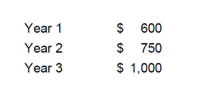

606-10-55-343 An entity enters into 100 separate contracts with customers to provide 1 year of maintenance services for $1,000 per contract. The terms of the contracts specify that at the end of the year, each customer has the option to renew the maintenance contract for a second year by paying an additional $1,000. Customers who renew for a second year also are granted the option to renew for a third year for $1,000. The entity charges significantly higher prices for maintenance services to customers that do not sign up for the maintenance services initially (that is, when the products are new). That is, the entity charges $3,000 in Year 2 and $5,000 in Year 3 for annual maintenance services if a customer does not initially purchase the service or allows the service to lapse.

606-10-55-344 The entity concludes that the renewal option provides a material right to the customer that it would not receive without entering into the contract because the price for maintenance services are significantly higher if the customer elects to purchase the services only in Year 2 or 3. Part of each customer's payment of $1,000 in the first year is, in effect, a nonrefundable prepayment of the services to be provided in a subsequent year. Consequently, the entity concludes that the promise to provide the option is a performance obligation.

606-10-55-345 The renewal option is for a continuation of maintenance services, and those services are provided in accordance with the terms of the existing contract. Instead of determining the standalone selling prices for the renewal options directly, the entity allocates the transaction price by determining the consideration that it expects to receive in exchange for all the services that it expects to provide in accordance with paragraph 606-10-55-45.

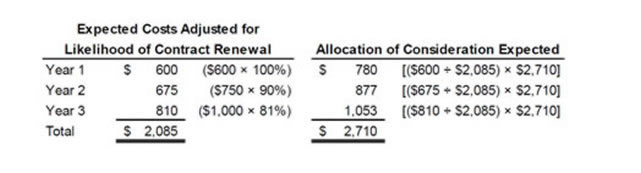

606-10-55-346 The entity expects 90 customers to renew at the end of Year 1 (90 percent of contracts sold) and 81 customers to renew at the end of Year 2 (90 percent of the 90 customers that renewed at the end of Year 1 will also renew at the end of Year 2, that is 81 percent of contracts sold).

606-10-55-347 At contract inception, the entity determines the expected consideration for each contract is $2,710 [$1,000 + (90 percent × $1,000) + (81 percent × $1,000)]. The entity also determines that recognizing revenue on the basis of costs incurred relative to the total expected costs depicts the transfer of services to the customer. Estimated costs for a three-year contract are as follows:

606-10-55-348 Accordingly, the pattern of revenue recognition expected at contract inception for each contract is as follows:

View image

View image

606-10-55-349 Consequently, at contract inception, the entity allocates to the option to renew at the end of Year 1 $22,000 of the consideration received to date [cash of $100,000 – revenue to be recognized in Year 1 of $78,000 ($780 × 100)].

606-10-55-350 Assuming there is no change in the entity's expectations and the 90 customers renew as expected, at the end of the first year, the entity has collected cash of $190,000 [(100 × $1,000) + (90 × $1,000)], has recognized revenue of $78,000 ($780 × 100), and has recognized a contract liability of $112,000.

606-10-55-351 Consequently, upon renewal at the end of the first year, the entity allocates $24,300 to the option to renew at the end of Year 2 [cumulative cash of $190,000 – cumulative revenue recognized in Year 1 and to be recognized in Year 2 of $165,700 ($78,000 + $877 × 100)].

606-10-55-352 If the actual number of contract renewals was different than what the entity expected, the entity would update the transaction price and the revenue recognized accordingly.

> > > Example 52—Customer Loyalty Program

606-10-55-353 An entity has a customer loyalty program that rewards a customer with 1 customer loyalty point for every $10 of purchases. Each point is redeemable for a $1 discount on any future purchases of the entity's products. During a reporting period, customers purchase products for $100,000 and earn 10,000 points that are redeemable for future purchases. The consideration is fixed, and the standalone selling price of the purchased products is $100,000. The entity expects 9,500 points to be redeemed. The entity estimates a standalone selling price of $0.95 per point (totalling $9,500) on the basis of the likelihood of redemption in accordance with paragraph 606-10-55-44.

606-10-55-354 The points provide a material right to customers that they would not receive without entering into a contract. Consequently, the entity concludes that the promise to provide points to the customer is a performance obligation. The entity allocates the transaction price ($100,000) to the product and the points on a relative standalone selling price basis as follows:

View image

View image

606-10-55-355 At the end of the first reporting period, 4,500 points have been redeemed, and the entity continues to expect 9,500 points to be redeemed in total. The entity recognizes revenue for the loyalty points of $4,110 [(4,500 points ÷ 9,500 points) × $8,676] and recognizes a contract liability of $4,566 ($8,676 – $ 4,110) for the unredeemed points at the end of the first reporting period.

606-10-55-356 At the end of the second reporting period, 8,500 points have been redeemed cumulatively. The entity updates its estimate of the points that will be redeemed and now expects that 9,700 points will be redeemed. The entity recognizes revenue for the loyalty points of $3,493 {[(8,500 total points redeemed ÷ 9,700 total points expected to be redeemed) × $8,676 initial allocation] – $4,110 recognized in the first reporting period}. The contract liability balance is $1,073 ($8,676 initial allocation – $7,603 of cumulative revenue recognized).

> > Nonrefundable Upfront Fees

606-10-55-357 Example 53 illustrates the guidance in paragraphs 606-10-55-50 through 55-53 on nonrefundable upfront fees.

> > > Example 53—Nonrefundable Upfront Fee

606-10-55-358 An entity enters into a contract with a customer for one year of transaction processing services. The entity's contracts have standard terms that are the same for all customers. The contract requires the customer to pay an upfront fee to set up the customer on the entity's systems and processes. The fee is a nominal amount and is nonrefundable. The customer can renew the contract each year without paying an additional fee.

606-10-55-359 The entity's setup activities do not transfer a good or service to the customer and, therefore, do not give rise to a performance obligation.

606-10-55-360 The entity concludes that the renewal option does not provide a material right to the customer that it would not receive without entering into that contract (see paragraph 606-10-55-42). The upfront fee is, in effect, an advance payment for the future transaction processing services. Consequently, the entity determines the transaction price, which includes the nonrefundable upfront fee, and recognizes revenue for the transaction processing services as those services are provided in accordance with paragraph 606-1055-51.

Estimating Standalone Selling Prices (Paragraphs 606-10-32-31 through 32-35)

BC269. The Boards observed that many entities may already have robust processes for determining standalone selling prices on the basis of reasonably available data points and the effects of market considerations and entity-specific factors. However, other entities may need to develop processes for estimating selling prices of goods or services that are typically not sold separately. The Boards decided that when developing those processes, an entity should consider all reasonably available information on the basis of the specific facts and circumstances. That information might include the following:

a. Reasonably available data points (for example, a standalone selling price of the good or service, the costs incurred to manufacture or provide the good or service, related profit margins, published price listings, third-party or industry pricing, and the pricing of other goods or services in the same contract)

b. Market conditions (for example, supply and demand for the good or service in the market, competition, restrictions, and trends)

c. Entity-specific factors (for example, business pricing strategy and practices)

d. Information about the customer or class of customer (for example, type of customer, geographical region, and distribution channel).

Customer Options for Additional Goods or Services (Paragraphs 606-10-55-41 through 55-45)

BC386. In some contracts, customers are given an option to purchase additional goods or services. The Boards considered when those options should be accounted for as a performance obligation. During those discussions, the Boards observed that it can be difficult to distinguish between the following:

a. An option that the customer pays for (often implicitly) as part of an existing contract, which would be a performance obligation to which part of the transaction price is allocated

b. A marketing or promotional offer that the customer did not pay for and, although made at the time of entering into a contract, is not part of the contract, and that would not be a performance obligation in that contract.

BC387. Similar difficulties in distinguishing between an option and an offer have arisen in U.S. GAAP for the software industry. Previous U.S. GAAP revenue recognition guidance for the software industry specified that an offer of a discount on future purchases of goods or services was presumed to be a separate option in the contract, if that discount was significant and also incremental both to the range of discounts reflected in the pricing of other elements in that contract and to the range of discounts typically given in comparable transactions. Those notions of “significant” and “incremental” form the basis for the principle of a material right that is used to differentiate between an option and a marketing or promotional offer. However, the Boards observed that even if the offered discount is not incremental to other discounts in the contract, it nonetheless could, in some cases, give rise to a material right to the customer. Consequently, the Boards decided not to carry forward that part of the previous revenue recognition guidance from U.S. GAAP into Topic 606.

The Financial Accounting Standards Board (FASB) is an independent standard-setting body of the Financial Accounting Foundation, a not-for-profit corporation. The FASB is responsible for establishing Generally Accepted Accounting Principles (GAAP), standards of financial accounting that govern the preparation of financial reports by public and private companies and not-for-profit organizations in the United States and other jurisdictions. For more information visit www.fasb.org