This paper has been prepared for discussion at a public meeting of the FASB | IASB Joint Transition Resource Group for Revenue Recognition. It does not purport to represent the views of any individual members of either board or staff. Comments on the application of U.S. GAAP or IFRS do not purport to set out acceptable or unacceptable application of U.S. GAAP or IFRS.

Purpose

1. Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers, and IFRS 15 Revenue from Contracts with Customers (collectively referred to as the "new revenue standard"), includes guidance on the recognition, measurement, and presentation of consideration payable to a customer. The following implementation questions raised by stakeholders associated with that guidance were discussed at Joint Transition Resource Group for Revenue Recognition (TRG) meetings on January 26, 2015 and on March 30, 2015:

Question 1: Which payments to a customer are in the scope of the guidance on consideration payable to a customer?

Question 2: Who are considered an entity's customers when applying the guidance on consideration payable to a customer?

Question 3: How does the guidance on timing of recognition of consideration payable to a customer reconcile with the variable consideration guidance?

2. TRG members generally coalesced around views on Questions 1 and 2. However, because the discussion on this topic was held separately by TRG members in Norwalk and London due to technology issues and there was not consensus among TRG members on Question 3, the staff think it would be beneficial for the TRG members to discuss the topic jointly.

Accounting Guidance & Background

3. See TRG paper 28 for relevant accounting guidance and background.

Question 1: Which payments to a customer are in the scope of the guidance on consideration payable to a customer?

4. TRG members discussed the following views (see TRG paper 28 for details of each view):

(a) View A: Entities should assess all consideration payable to a customer.

(b) View B: Entities should assess consideration payable to a customer only within the context of that contract with a customer (or combined contracts).

(c) View C: Entities should assess consideration payable to a customer only within a contract with a customer (or combined contracts) and to a customer in the distribution chain of that contract with a customer.

5. Considering the discussions in both London and Norwalk, TRG members had mixed views between Views A and B. No TRG members agreed with View C. Several TRG members thought that strict application of Views A and B, as articulated in the TRG paper, may result in financial reporting outcomes that do not reflect the core principle of the revenue standard to "recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods and services."

However, TRG members noted that a reasonable application of Views A and B could be accomplished with processes and internal controls to identify payments to customers that could be related to a revenue contract. As a result, TRG members observed that a reasonable application of either Views A or B should result in similar financial reporting outcomes.

6. In regards to application of View A, some TRG members were concerned that the articulation of View A would require an entity to separately assess and document each payment made to a customer. They did not think that was a reasonable application of the new revenue standard and observed that it could be significantly more costly than existing practice under GAAP and not practical in some cases. The staff observes that many entities already have processes and internal controls to comply with consideration payable guidance under existing GAAP.

7. In regards to application of View B, some TRG members expressed concern that a strict application of View B may not identify a payment to a customer that is linked to a revenue contract. For example, payments to customers that significantly exceed the fair value of the goods or services received from the customer or payments to an end customer within the distribution chain that are intended to move the entity's products through the distribution chain might not be combined under the contract combination guidance in the new revenue standard if those contracts are not entered into at or near the same time. However, many TRG members thought that a reasonable application of the modification guidance in the new revenue standard when applying View B would identify such payments because the two transactions would be economically linked.

Question 2: Who are considered an entity's customers when applying the guidance on consideration payable to a customer?

8. At the March 30, 2015 TRG meeting two views were discussed:

(a) View A: An entity's customers are limited to those in the distribution chain.

(b) View B: An entity's customers include those in the distribution chain and might include a customer's customers that extend beyond those in the distribution chain.

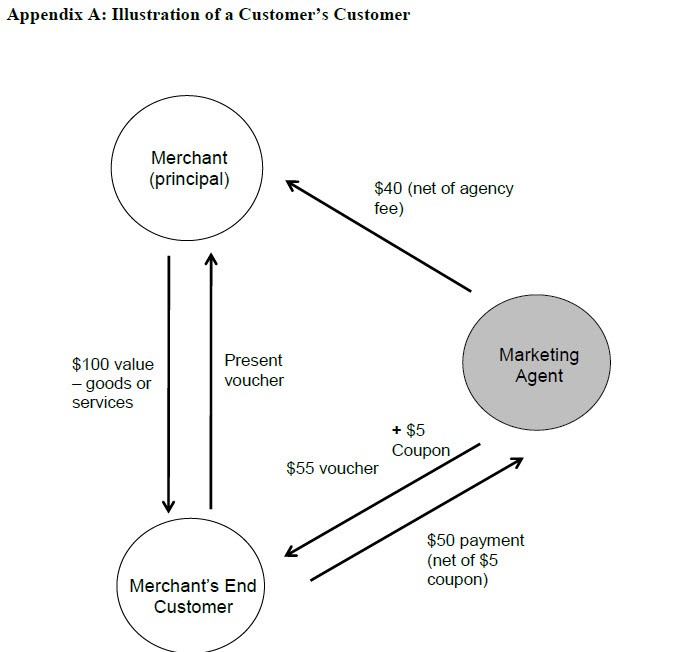

9. Considering the discussions in both London and Norwalk, most TRG members supported View B. TRG members observed that an entity that is acting as an agent (that is, arranging for another party to provide goods or services) might view both the principal (that is, the entity's customer) and the end customer (that is, the principal's end customer) as its customers in an arrangement, depending on the facts and circumstances. For example, in some arrangements, an entity that is an agent determines its only customer is the principal. In other arrangements, an entity that is an agent thinks its customers include the principal and the principal's end customer. A transaction for which this question is applicable is illustrated in Appendix A. In addition to identifying the entity's customer(s), the entity would need to include all those in the distribution chain of its identified customers. TRG members noted that there is some diversity in practice today about whether an entity that is an agent thinks its customer is only the principal and View B would be consistent with that diversity in practice.

10. TRG members agreed that under either View A or View B, a payment to a customer's customer would be considered a payment to a customer if the entity has a contractual agreement with its customer to provide consideration to that customer's customer.

Question 3: How does the guidance on timing of recognition of consideration payable to a customer reconcile with the variable consideration guidance?

11. The new revenue standard requires an entity to consider the terms of the contract and its customary business practices to determine the transaction price, which is the amount of consideration to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer. As part of determining the transaction price, an entity considers the effects of variable consideration, including constraining estimates of variable consideration; the existence of a significant financing component; noncash consideration; and consideration payable to a customer.

12. The guidance on consideration payable to a customer states that such amounts should be recognized as a reduction of revenue at the later of when the related revenue is recognized or the entity pays or promises to pay such consideration (promises could be implied by customary business practices).

This is referred to as the "later of guidance"for the remainder of this memo. Some think that the later of guidance could be viewed, in some cases, as inconsistent with guidance on estimating variable consideration. They note that if an entity intends to provide the customer with a price concession when entering into the contract, it should consider that price concession when estimating variable consideration (subject to the constraint on variable consideration) as part of the transaction price. In that circumstance, even though the price concession is economically similar to consideration payable to a customer, an entity would not wait until it has communicated the price concession to recognize a reduction in revenue.

13. At the March 30, 2015 TRG meeting, the following two views regarding the potential inconsistency were discussed:

(a) View A: The guidance on variable consideration and the later of guidance for consideration payable to a customer can be reconciled because not all consideration payable to a customer is variable consideration.

(b) View B: The guidance on variable consideration and the later of guidance for consideration payable to a customer is not consistent.

View A

14. Proponents of this view

believe the guidance on variable consideration and the later of guidance for consideration payable to a customer can be reconciled. They do not think the guidance conflicts, because not all consideration payable to a customer is variable consideration. Those proponents think that in accordance with paragraph 606-10-32-7 [52], some payments would not be considered variable consideration if, when entering into the contract, they are not explicitly stated in the contract, the customer does not have a valid expectation that the entity will offer a price concession, or other facts and circumstances do not indicate that the entity intends to offer a price concession. Payments to customers that the entity has a past practice of providing would likely be expected at contract inception and, thus, would reduce the transaction price before the payment is communicated to customers. Consideration payable to a customer that is not variable consideration would follow the later of guidance and reduce revenue at the later of the date when goods or services are transferred to the customer or when the entity pays or promises to pay the customer in accordance with paragraph 606-10-32-27 [72].

15. However, proponents of this view acknowledge that this view would be a change to existing GAAP, because unlike existing GAAP, the later of guidance in the new revenue standard does not apply to all consideration payable to a customer. They point to Case A of Example 23 (paragraphs 606-10-55-208 [IE116] through 55-212 [IE120] in the new revenue standard). In that example, based on past practices and to encourage sales through the distribution chain, the entity anticipates at contract inception that it will grant a price concession to the customer, and, as a result, the consideration is variable. That price concession is economically similar to consideration payable to a customer. In that example, the entity reduces the amount of revenue recognized for the expected price concession (even though the price concession has not been communicated to the customer), because the entity has an intention (based on its past experience) when entering into the contract to offer a price concession.

16. Some proponents of this view also point out that even if the guidance was inconsistent with the later of guidance in paragraph 606-10-32-27 [72], it would be infrequently applied. They think that an entity would use the later of guidance only when it has no history and no expectation of providing incentives. Proponents believe that for most incentives, an entity will have already provided the same or similar incentives for the same or similar products; therefore, either the customer will have a valid expectation to receive, or the entity will intend to provide, a similar incentive for similar transactions in the future. Thus, the entity would reduce the transaction price for those expected amounts when estimating the transaction price. However, other stakeholders disagree and think that incentive programs are sufficiently varied such that past incentive programs may not create a valid customer expectation or demonstrate the entity's intent. As such, those stakeholders think the later of guidance would be frequently applied. Those stakeholders acknowledge that determining whether the later of guidance should be applied will require significant judgement in some cases.

17. Opponents of View A believe variable consideration should have a broad scope and think that View A inappropriately reduces the scope of what qualifies as variable consideration. Those with this view do not think that paragraph 606-10-32-7 [52] defines the scope of what is considered variable consideration.

View B

18. Proponents of this view think the guidance on variable consideration and the guidance on recognizing consideration payable are inconsistent. Specifically, they assert that the variable consideration guidance would require recognition of consideration payable to a customer (a reduction to revenue) when revenue is recognized, as opposed to waiting until the entity promises to the customer to pay. That is, if an entity has an expectation of providing a price concession it would reflect that in the transaction price as variable consideration. Proponents note that the principle in the new revenue standard for determining the transaction price is to reflect the "amount of consideration to which an entity expects to be entitled;"therefore, they think the later of guidance is inconsistent with relying on an entity's expectations rather than potentially waiting to reduce revenue until a promise for consideration is made to the customer.

19. Proponents of this view think that an entity should reduce the transaction price for amounts the entity intends to pay to customers when entering into the contract, including instances where the entity may not have a past practice of providing consideration to a customer. Proponents of View B think reducing the transaction price based on an entity's intentions best aligns with the overall principle to reflect the amounts to which the entity expects to be entitled. Other proponents state whether or not customer incentives are deemed to be variable should not impact timing of recognition, as both fixed and variable amounts ultimately impact the amount to which the entity expects to be entitled.

Question for the TRG Members

1. What are your views about the implementation issues discussed in this paper?

1. Under View B in question 2, in addition to viewing the merchant as its customer, the marketing agent might also view the merchant’s end customer as its own customer. Therefore, under that view, the marketing agent reduces the transaction price for amounts paid to both the merchant and the end customer, even though the end customer is not within the distribution chain.

___________ The IASB is the independent standard-setting body of the IFRS Foundation, a not-for-profit corporation promoting the adoption of IFRSs. For more information visit www.ifrs.org

The Financial Accounting Standards Board (FASB) is an independent standard-setting body of the Financial Accounting Foundation, a not-for-profit corporation. The FASB is responsible for establishing Generally Accepted Accounting Principles (GAAP), standards of financial accounting that govern the preparation of financial reports by public and private companies and not-for-profit organizations in the United States and other jurisdictions. For more information visit www.fasb.org

1 Paragraph 606-10-10-2[2]

2 Paragraph 606-10-32-27 [52]

3 This view is consistent with the staff’s view provided in Memo No. 28 for the March 2015 TRG meeting.

Copyright #year# by Financial Accounting Foundation, Norwalk, Connecticut.

View image

View image