This paper has been prepared for discussion at a public meeting of the FASB | IASB Joint Transition Resource Group for Revenue Recognition. It does not purport to represent the views of any individual members of either board or staff. Comments on the application of U.S. GAAP or IFRS do not purport to set out acceptable or unacceptable application of U.S. GAAP or IFRS.

Purpose

1. Some stakeholders informed the staff that there are questions about the guidance in Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers, and IFRS 15 Revenue from Contracts with Customers (collectively referred to as the 'new revenue standard'), regarding how to determine the measure of progress when a single performance obligation satisfied over time contains multiple promised goods or services.

2. This paper summarizes potential challenges pointed out to the staff. The staff will seek input from members of the FASB-IASB Joint Transition Resource Group for Revenue Recognition (TRG) on these challenges.

Background

3. A single performance obligation could contain multiple promised goods or services. This might be the case when the individual goods or services are not distinct and, in accordance with paragraph 606-10-25-22 [30], those goods or services are combined with other goods or services until a distinct bundle of goods or services is identified. This might also be the case if a non-distinct good or service is combined with a distinct good or service. The goods or services that are not distinct on their own are bundled into what will be referred to throughout this paper as a "combined performance obligation."

4. Step 5 of the new revenue standard, Recognize Revenue When (or As) the Entity Satisfies a Performance Obligation, requires an entity to apply a single method of measuring progress for each performance obligation. The objective of the measure of progress is to depict the entity's performance in satisfying a performance obligation. Stakeholders indicated that it can be difficult to determine the appropriate method that meets this objective when there is a combined performance obligation. That is, unless all of the individual promises are performed in a similar pattern over the same time period, some stakeholders think that a single measure of progress might not accurately depict the economics of the arrangement. Typically, this is the case when the entity's transfer of the goods or services that make up a combined performance obligation will be transferred over different periods of time.

5. For example, assume an entity grants a 10-year license that is not distinct from a 1- year service arrangement. If the entity’s promise in granting the license is satisfied over time and the service arrangement is satisfied over time, the entity would fulfil each of the promises in the combined performance obligation over significantly different performance periods. This is because the customer has the right to access the entity’s intellectual property for 10 years and the customer will receive the services over 1 year. Additionally, the measure of progress that depicts the entity’s performance if each promise was a separate performance obligation could be different (for example, a time-based method for the license versus a labor-based input method for the service).

6. Stakeholders have also indicated that there are operational difficulties related to requiring a single measure of progress in some cases. This could be the case when the consideration for a single performance obligation includes multiple payment streams consisting of fixed and variable consideration, such as an upfront fee and additional fees based on, for example, the number of transactions the entity processes.

7. Under current GAAP, there is no clear guidance on how to account for a combined unit of account, and determining the appropriate attribution in these situations can be challenging. For example, challenges arise when deliverables cannot be separated into their own units of account due to the lack of standalone value pursuant to Subtopic 605-25, Multiple-Element Arrangements. The staff understands there is diversity in practice in accounting for these arrangements under current U.S. GAAP, and the following are some of the views that exist in current practice:

(a) Final Deliverable Model: Some stakeholders think there is a rebuttable presumption that the revenue recognition model for the final deliverable should be followed. Under this model, revenue would be recognized over the performance period of the last deliverable.

(b) Predominant Deliverable Model: Some stakeholders think that, in some facts and circumstances, the presumption of the final deliverable can be overcome and that revenue recognition should follow the revenue guidance applicable to the predominant item in the combined unit of account.

(c) "Slower-of" Methodology: Some stakeholders apply a methodology that recognizes revenue based upon the slower of the combined deliverables or cash received. For example, if Service A was 50 percent complete and Service B was 25 percent complete, revenue would be limited to the lesser of 25 percent of the total revenue or cash received.

(d) Multiple Attribution: Some stakeholders think that in some circumstances a multiple attribution approach most appropriately reflects the economics of the arrangement. That is, revenue is recognized in different patterns for different deliverables or payment streams in the single unit of account. In some circumstances, this provides a recognition pattern as if the deliverables were separate units of account. The basis for this approach is the EITF 08-1 working group discussions at which members indicated that this approach could be appropriate and is typically more common in service arrangements.

8. Under current practice, multiple attribution also takes place when there are multiple payment streams. Some examples include, but are not limited to, the following:

(a) Contingent performance bonuses: Subtopic 605-28, Milestone Method, provides guidance applicable to research or development arrangements for determining when it is appropriate to recognize milestone payments in their entirety in the period the milestone is achieved. Entities that have elected to apply the milestone method potentially have arrangements with multiple attribution. For example, the arrangement may include an upfront fee that is recognized ratably over the performance period and the milestone payments that would be recognized when the milestone is achieved.

(b) Reimbursement of out-of-pocket expenses: The staff understands that many entities recognize out-of-pocket expenses that are presented on a gross basis (that is, the amounts billed to the customer as revenue and the amounts incurred as expense) when the entity incurs the expenses and has the right to bill the expenses. This is the case even if the remainder of the fees in the arrangement are recognized in a different pattern. For example, the other fees might consist of a fixed fee that is recognized ratably over the service period, and the revenue associated with the out-of-pocket expenses is recognized when the costs are incurred and billed.

(c) Upfront fees: Some arrangements, such as transaction processing services, include nonrefundable upfront fees and subsequent per transaction pricing. The staff understands that, under current GAAP, the upfront fee often is recognized ratably over the performance period, while the per-transaction fees are typically recognized in the amount the entity has the right to invoice for the transaction processing, regardless of whether the transactions are processed ratably. As such, the upfront fee and per transaction fees are sometimes recognized in different patterns. However, the Securities and Exchange Commission (SEC) Staff Accounting Bulletin Topic 13, Revenue Recognition, provides recognition guidance specific to upfront fees when there is only a single deliverable in the arrangement that results in this accounting. This guidance requires the upfront fee to be recognized over the period the customer is expected to benefit from the payment on a systematic basis. In contrast, the new revenue standard considers the upfront fee to be part of the overall transaction price and does not provide separate recognition guidance for upfront fees. (Note: Under Subtopic 605-25, when an arrangement includes multiple deliverables, any upfront fee is simply part of the consideration for the arrangement and is allocated on the same basis as the other consideration in the contract to the separate deliverables)

9. Under current IFRS, there is no clear guidance or practice on utilizing multiple measures of progress. In fact, there is very little guidance in International Accounting Standard (IAS) 18 Revenue, on separating a contract into multiple units of account, and, therefore, the staff understand there is less focus on the unit of account for recognizing revenue. IAS 11 Construction Contracts and IAS 18 provide guidance on recognition and state that an entity use the method that reliably measures the work completed to date or services performed, and, therefore, there is diversity in how an entity determines the pattern of revenue recognition.

Issue 1 – Can multiple measures of progress be utilized to depict an entity's performance in completing a combined performance obligation?

10. Step 5 requires an entity to select a method to measure progress toward completion of a performance obligation satisfied over time. Paragraph 606-10-25-32 [40] states that an entity should apply a single measure of progress for each performance obligation, and paragraph BC161 explains the Boards reasoned that utilizing more than one method to measure its performance would effectively bypass the guidance on identifying performance obligations. This is in contrast to existing GAAP/IFRS in which there is little authoritative guidance related to the attribution in combined units of account or service arrangements and GAAP/IFRS does not explicitly state that multiple attribution is unacceptable.

11. The staff think that the new revenue standard is clear that using multiple methods of measuring progress for the same performance obligation would not be appropriate. For example, utilizing different measures of progress for different non-distinct goods or services in the combined performance obligation or allocating a portion of the transaction price and recognizing revenue for a non-distinct good or service (or allocating fixed consideration to a distinct good or service that forms part of a single performance obligation) would be inappropriate. More specifically, ignoring the unit of account prescribed in the new revenue standard and recognizing revenue in a manner that overrides the separation and allocation guidance would not be appropriate.

12. Based upon BC161, the staff also think that a single method of measuring progress should not be broadly interpreted to mean an entity may apply multiple measures of progress so long as all measures employed are either output or input methods. Utilizing different types of input or output methods for different promises in a combined performance obligation would have the result of treating each promise as a separate performance obligation.

13. Most stakeholders think that the guidance is clear; however, they have expressed concern that it could be challenging in some cases to select a single measure of progress. In addition, some stakeholders think the resulting pattern of revenue recognition might not faithfully depict the economics of the arrangement. For example, these stakeholders think a single measure of progress may not depict the economics when a significant amount of revenue is deferred over a long period of time even though the entity has received cash related to performance for the non-distinct services. Another example includes long-term arrangements with multiple variable payment streams where the transaction price needs to be estimated subject to the constraint on variable consideration such as in hotel management. These stakeholders think a better depiction of the entity’s performance would be to select a revenue recognition pattern for the combined performance obligation that is consistent with the overall objective for measuring progress in paragraph 606-10-25-31 [39], even if this requires the use of multiple measures of progress. Others think that, similar to current practice, an entity should be able to recognize some fees related to a combined performance obligation, such as upfront fees, using a different measure of progress (for example, a time basis) to that used for the combined performance obligation. They believe that would best depict the entity’s overall performance.

Question 2 – How should an entity determine the measure of progress when a combined performance obligation satisfied over time contains multiple goods or services?

14. Paragraph 606-10-25-31 [39] states that the overall objective when measuring progress toward complete satisfaction of a performance obligation satisfied over time is to depict an entity's performance in satisfying its performance obligation. As noted in paragraph BC159, the Boards decided it would not be feasible to consider all possible methods and prescribe when an entity should use each method. Accordingly, an entity should use judgment when selecting an appropriate method of measuring progress toward complete satisfaction of a performance obligation. However, that does not mean that an entity has a "free choice."

15. It may require more judgment to determine the measure of progress in a combined performance obligation when there are multiple non-distinct promises that have different patterns of performance, but like other performance obligations satisfied over time, an entity must apply judgment in selecting the method that complies with the overall objective. If there is not a clear pattern that applies to all of the goods or services (for example, all services are time based over the same time period), the staff does not think that entities should default to a "final deliverable" or "predominant deliverable" methodology. Instead, an entity should consider the nature of the entity's overall promise for the combined performance obligation and performance required to completely satisfy the entire performance obligation. To make that assessment, the staff think it is important to consider the reasons why the entity decided that the goods or services are not distinct and have been bundled into a combined performance obligation.

16. If an entity thinks that the result of a single measure of progress for a combined performance obligation does not faithfully depict the economics of the arrangement, the staff think it could be an indicator that the entity has not identified the appropriate performance obligations (that is, there might be more than one performance obligation). That is not to say the entity definitively has identified the wrong performance obligation(s). The staff understand there will be cases under the new revenue standard (similar to current practice) in which the entity has properly identified the unit of account, and selecting a single measure of progress for the combined performance obligation will require significant judgement.

17. The staff have prepared a few scenarios to facilitate discussion among the TRG members. The staff think a discussion among the TRG members might help to educate stakeholders about how to approach this issue. For each scenario, the staff have included their views about how to think about the appropriate measure of progress. It is important for stakeholders to note when reading the scenarios and staff views that an entity will need to consider the specific facts and circumstances of a contract with a customer and sometimes apply significant judgment to identify an appropriate performance obligation and measure of progress that depicts an entity's "performance in transferring control of goods or services promised to a customer (that is, the satisfaction of an entity's performance obligation)."

Scenario 1

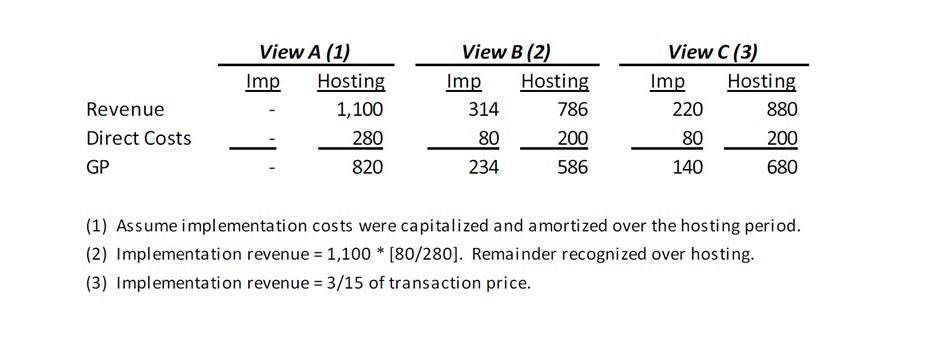

A cloud computing company provides software as a service solutions to its customers. The typical arrangement includes promises for access to hosted software for one year and upfront implementation services. The one year hosting period begins when the implementation is complete, and the customer cannot access or utilize the service until this time.

The implementation services are typically performed over a 3 month period. The vendor's solution is proprietary, and no other vendors are capable of performing the implementation. Furthermore, the customer cannot derive benefit from the implementation or the hosting service until the implementation is complete. For the purpose of this example, it is assumed that the entity concludes the implementation services are not capable of being distinct from the hosting. Assume the entity concludes there is no material right for future renewals.

Assume that the total transaction price is CU 1,100, and the direct costs that would be used in the cost to cost input method is CU80 for implementation and CU200 for the hosting service.

18. The staff's view and other views considered include:

(a) View A (Staff View) – Use a measure of progress that depicts the performance of the hosting services beginning when the hosting service commences. Under View A, the nature of the entity's overall promise (and, therefore, combined performance obligation) is to provide the hosting service, and no revenue would be recognized over the implementation period because that promise does not transfer a service to a customer. The entity would select a method that depicts the performance of the hosting services to measure progress toward completion. For example, a time-based method might be considered appropriate. The entity would need to consider whether or not it meets the criteria to capitalize the costs of implementation in accordance with paragraph 340-40-25-5 [95].

(b) View B – Use a measure of progress that depicts the performance of the implementation services. Under View B, a labor-based input method or another input method might be used to measure progress of the entire performance obligation. View B would likely result in more revenue recognized over the implementation period than the hosting period. This would be the case due to the fact that the implementation service is typically more cost/labor intensive than the hosting (that is, gross margins are typically higher for hosting).

(c) View C – Ratable recognition for the entire performance obligation. Under View C, a time based ratable approach would be used for the entire performance obligation beginning with implementation. This would likely result in a recognition pattern somewhere between View A and View B.

19. The following table summarizes how the revenue and cost would be recognized under each view throughout the performance of the implementation and hosting (Note: This table is not depicting allocation between two performance obligations because there is only one performance obligation in this contract. Rather, the table is depicting the transaction price that would be recognized related to the proportion of the task completed under each view):

20. The staff think that the nature of the entity's overall promise is the hosting service and the implementation service does not transfer a service to a customer. If the implementation does not transfer a service, then it would be disregarded from the performance obligation, similar to set up activities described in 606-10-25-17 [25].

21. The staff think this view is analogous to setup activities in an outsourcing arrangement as discussed in Example 53 (paragraphs 606-10-55-358 through 55-360 [IE272 through IE274]). In that example, setup activities are not considered to be part of the performance obligation because they do not transfer a good or service to a customer. Similarly paragraph 606-10-55-52 [B50] states that if nonrefundable fees relate to a good or service, the entity should evaluate whether to account for the good or service as a separate performance obligation. Paragraph 606-10-55-53 [B51] goes on to state the following:

An entity may charge a nonrefundable fee in part as compensation for costs incurred in setting up a contract (or other administrative tasks as described in paragraph 606-10-25-17 [25]). If those setup activities do not satisfy a performance obligation, the entity should disregard those activities (and related costs) when measuring progress in accordance with paragraph 606-10-55-21 [B19]. That is because the costs of setup activities do not depict the transfer of services to the customer. The entity should assess whether costs incurred in setting up a contract have resulted in an asset that should be recognized in accordance with paragraph 340-40-25-5 [95].

22. If those setup activities do not satisfy a performance obligation, the entity should disregard those activities (and related costs) when measuring progress in accordance with paragraph 606-10-55-21 [B19]. That is because the costs of setup activities do not depict the transfer of services to the customer. Similarly, in this scenario, the implementation service is not a separate performance obligation and does not satisfy a separate performance obligation. The staff also think costs incurred during implementation would likely be capitalized in accordance with paragraph 340-40-25-5 [95].

23. The staff think the conclusion that the implementation is not capable of being distinct supports the conclusion that the nature of the entity's overall promise is to provide hosting services. In fact, the staff think including the implementation service in the measure of progress is inconsistent with the conclusion that the implementation is not capable of being distinct in accordance with paragraph 606-10-25-19(a) [27(a)]. That is, concluding the implementation is not capable of being distinct means that the customer cannot benefit from that service (either on its own or together with other readily available resources), which also means control does not transfer. Said differently, because a service is transferred when the customer obtains control of that asset

and control includes the customer's ability to obtain substantially all the remaining benefits from the good or service,

performing only the service that the customer cannot benefit from would not transfer control. Since the implementation services are performed prior to the customer benefiting from the hosting service, it should be excluded from the measure of progress pursuant to paragraph 606-10-25-34 [42], which states that an entity shall exclude from the measure of progress any goods or services for which the entity does not transfer control to a customer.

24. This does not mean the staff think that anytime a good or service is not capable of being distinct it should be excluded entirely from the measure of progress or that all services in a combined performance obligation must commence prior to recognizing revenue. For example, assume an entity enters into a contract to provide Service A, Service B, and Service C. The services are bundled into a combined performance obligation because Service A commences first and is not capable of being distinct without Service B or C. Additionally, all three services are highly interrelated and not separately identifiable. Assume Service A commences in month 1, Service B commences in month 2 and Service C commences in month 3, all continue through the end of the contract period, and the entity concludes the combined performance obligation is satisfied over time. In this fact pattern, the customer would not be able to obtain any benefit until Service B commences (that is, the customer does not benefit from Service A on its own). The entity would need to consider the nature of the entity's overall promise to determine the appropriate measure of progress, but would not necessarily have to wait until Service C commenced to begin recognizing revenue. That is, the entity might be able to begin recognizing revenue when Service B commences.

Other Views Considered

25. View B and View C are based on the premise that control begins to transfer when the implementation services begin. The staff understands that some stakeholders think control transfers during implementation if one of the criteria in paragraph 606-10-25-27 [35] (that evaluates when control is transferred over time) has been met. For example, if the entity has an enforceable right to payment for performance completed throughout implementation and hosting, the entire performance obligation might meet the criterion in paragraph 606-10-25-27(c) [35(c)] to be recognized over time (Note: The customer does not begin to consume and receive benefit from the performance obligation, as described in paragraph 606-10-25- 27(a) [35(a)], until the customer can begin to access and use the hosted software.) The staff think it would be inappropriate to evaluate different promises in a combined performance obligation under different criteria in paragraph 606-10-25-27 [35] because the unit of account for this assessment is the performance obligation and not the individual promises. That is, concluding the implementation and hosting are transferred over time based on different criteria would effectively treat each item as separate performance obligations and would override the guidance on identifying performance obligations.

26. The staff think View B would not be appropriate even if the implementation is a service transferred to the customer. When considering the nature of the entity's overall promise and the reason why the two promises are combined, the staff think this method places more weight on the implementation services, rather than the hosting, because the staff think hosting is the nature of the entity's overall promise.

27. The staff does not think View C is appropriate because the customer only benefits during the hosting period (based on the reasons expressed in View A above). However, if the implementation was considered a service that is transferred to the customer, this view might strike a balance between the two services in the combined performance obligation and be more consistent with the nature of the entity's overall promise and combined output to the customer.

Scenario 2:

An entity promises to provide a software license and installation services that will substantially customize the software to add significant new functionality that enables the software to interface with other customized applications used by the customer.

The entity concludes that the software and services are not separately identifiable from the customized installation service and the criterion in paragraph 606-10-25-19(b) [27(b)] is not met. Therefore, the software and installation service is combined into a single performance obligation. The entity also concludes that the performance obligation is satisfied over time. If the license was distinct, it would be considered a point in time license.

28. The staff's view and other views considered include:

(a) View A (Staff View) – Use a measure of progress that depicts the performance of completing the customized software solution. Under View A, all of the revenue would be recognized over the period the customization services are performed.

(b) View B – Use an output method based on estimated value for each good or service delivered. Under View B, an output method based on the value of each good or service delivered would be estimated and recognized as each item is delivered. For example, the estimated value of the license would be recognized as delivered, and the value of each increment of service would be recognized as delivered.

(c) View C – Recognize revenue when the software is delivered. Some stakeholders indicated some entities might view the software license as the predominant item in the combined performance obligation and would recognize revenue as if that license was distinct and the only promise in the contract. Under View C, all of the revenue would be recognized upfront when the software license was delivered.

Staff View

29. While each promised good or service in the combined performance obligation is capable of being distinct, the license and installation service are inputs the entity uses to produce the combined output. As such, the nature of the combined performance obligation is developing the customized software over time. Therefore, the staff think that, because the creation of the customized software solution is the promise that is being performed over time, the measure of progress should be based on a method that reflects the entity's progress towards the completion of that service and, therefore, complete satisfaction of the combined performance obligation.

Other Views Considered

30. The staff do not think View B is appropriate. BC163 states the following regarding output methods:

Output methods recognize revenue on the basis of direct measurements of the value to the customer of the goods or services transferred to date (for example, surveys of performance completed to date, appraisals of results achieved, milestones reached, time elapsed, and units delivered or units produced). When applying an output method, value to the customer refers to an objective measure of the entity's performance in the contract. However, value to the customer is not intended to be assessed by reference to the market prices or standalone selling prices of the individual goods or services promised in the contract, nor is it intended to refer to the value that the customer perceives to be embodied in the goods or services. [Emphasis added.]

31. The staff understands that the emphasized statement was intended to prevent an entity from interpreting the term value as it relates to an output method as the ability to estimate the values of each non-distinct good or service combined into a single performance obligation and recognizing those relative values as each item is delivered. Paragraph 606-10-55-17 [B15] and BC163 are in the context of measuring progress toward satisfaction of the performance obligation with a focus on the proportion of the performance obligation completed. That is, the discussion in BC163 (and 606-10-55-17 [B15]) is about progress toward satisfying the performance obligation and, thus, has to do with how much or what proportion of the goods or services (quantities) have been delivered (but not the price). As such, paragraph BC163 clarifies that estimating and allocating the transaction price based on standalone selling prices or market values to a non-distinct good or service within the performance obligation is not an output method. This is because it would have the effect of treating each good or service as if it was a separate performance obligation. View B effectively results in a method that accounts for the license and services as two performance obligations.

32. The staff do not think View C is appropriate because it ignores the fact that the customer contracted for customized software and those customization services are being performed over time. Some stakeholders have suggested this view might be reasonable, at least in some cases, because of the discussion in paragraph BC407, which indicates entities might account for a combined performance obligation entirely as a license (which may be recognized at a point time, and likely would for licenses of software) if the license is the primary or dominant item in the combined performance obligation. In this scenario, the staff do not think it would be reasonable to conclude that the license is the primary or dominant component of the combined performance obligation. The staff think the nature of the entity's promise is to provide a customized software solution such that the base software license is not the dominant feature. The customization services appear to be significant to the promise to the customer as well.

Scenario 3

A franchisor enters into a 10-year license agreement with a new franchisee. The franchisor also promises to provide consulting services over the first year of the license agreement. The consulting services provide the franchisee with hours of service to help it set up operations to run its franchise.

For the purpose of this example, it is assumed that the franchisor concludes that the license and services should be combined into a single performance obligation because the license and services are highly interrelated (that is, each promise is capable of being distinct because the customer can derive some benefit from each item – from the franchise license on its own and the services together with the license granted upfront - but the promises are not distinct in the context of the contract). Furthermore, the entity concludes that the license is satisfied over time.

The transaction price consists of an upfront fee of CU 1 million for the license and CU 150,000 for a fixed number hours of consulting service that are performed in the first year.

33. The staff's view and other views considered include:

(a) View A (Staff View) – Use a measure of progress that best depicts the performance of the license. Under View A, the nature of the overall performance obligation is the franchisee's right to access the license and, therefore, the measure of progress would depict the transfer of the license. For example, using a time-based output method, the entire transaction price would be recognized ratably over the 10-year period. The entire transaction price of CU 1,150,000 would be recognized over the 10-year license agreement.

(b) View B – Use a measure of progress that depicts the performance of the services. Under View B, a measure of progress that best depicts the performance of the services would be used for the entire performance obligation. For example, a cost to cost input method might be used for the entire performance obligation. The entire transaction price would be recognized utilizing this method.

(c) View C – Recognize the license fee over the license period and recognize the consulting services as each hour of service is performed. This view would match the non-distinct promises with the contractual fees.

Staff View

34. Because the consulting services and license are interrelated and the consulting services actually enhance the benefit the franchisee will receive over the entire license period, the staff think the nature of the overall performance obligation is the franchisee's right to access the license. Even if the franchisor's level of effort is higher over the first year than any other individual year, given the relationship between the license and services, a time based method over the entire ten-year period would accurately depict the complete satisfaction of the performance obligation.

Other Views

35. Under View B, the incremental costs of the license would be insignificant compared to the direct costs of the consulting services, which would result in a recognition pattern that recognizes more revenue over the service period than the license period. As such, the staff does not think a measure of progress such as a cost to cost input method would appropriately depict the entity's performance. This method would put more weight on the services that are intended to enhance the benefit the customer derives from the license.

36. View C effectively treats the license and consulting services as separate performance obligations, which the staff think would effectively override the guidance in the new revenue standard about identifying performance obligations. Some stakeholders have indicated that some entities that have arrangements with combined licenses and services currently account for transactions in this manner. However, the staff think the new standard prohibits this treatment.

Questions for the TRG Members

1. Do the TRG members agree that it is clear that the new revenue standard does not allow multiple measures of progress for a single performance obligation?

2. Do the TRG members agree with the staff's views on determining the appropriate measure of progress when there is a combined performance obligation? Do you have other suggestions for an entity to consider when selecting a measure of progress for a combined performance obligation?

Appendix A – Accounting Guidance

1. The new revenue standard includes the following guidance on performance obligations satisfied over time:

606-10-25-27 [35] An entity transfers control of a good or service over time and, therefore, satisfies a performance obligation and recognizes revenue over time, if one of the following criteria is met:

a. The customer simultaneously receives and consumes the benefits provided by the entity's performance as the entity performs (see paragraphs 606-10-55-5 through 55-6 [B3 through B4]).

b. The entity's performance creates or enhances an asset (for example, work in process) that the customer controls as the asset is created or enhanced (see paragraph 606-10-55-7 [B5]).

c. The entity's performance does not create an asset with an alternative use to the entity (see paragraph 606-10-25-28 [36]), and the entity has an enforceable right to payment for performance completed to date (see paragraph 606-10-25-29 [37]).

2. The new revenue standard includes the following guidance on measuring progress toward complete satisfaction of a performance obligation over time:

606-10-25-31 [39] For each performance obligation satisfied over time in accordance with paragraphs 606-10-25-27 [35] through 25-29 [37], an entity shall recognize revenue over time by measuring the progress toward complete satisfaction of that performance obligation. The objective when measuring progress is to depict an entity's performance in transferring control of goods or services promised to a customer (that is, the satisfaction of an entity's performance obligation).

606-10-25-32 [40] An entity shall apply a single method of measuring progress for each performance obligation satisfied over time, and the entity shall apply that method consistently to similar performance obligations and in similar circumstances. At the end of each reporting period, an entity shall remeasure its progress toward complete satisfaction of a performance obligation satisfied over time.

606-10-25-33 [41] Appropriate methods of measuring progress include output methods and input methods. Paragraphs 606-10-55-16 [B14] through 55-21 [B19] provide guidance for using output methods and input methods to measure an entity's progress toward complete satisfaction of a performance obligation. In determining the appropriate method for measuring progress, an entity shall consider the nature of the good or service that the entity promised to transfer to the customer.

606-10-25-34 [42] When applying a method for measuring progress, an entity shall exclude from the measure of progress any goods or services for which the entity does not transfer control to a customer. Conversely, an entity shall include in the measure of progress any goods or services for which the entity does not transfer control to a customer when satisfying that performance obligation.

606-10-55-17 [B15] Output methods recognize revenue on the basis of direct measurements of the value to the customer of the goods or services transferred to date relative to the remaining goods or services promised under the contract. Output methods include methods such as surveys of performance completed to date, appraisals of results achieved, milestones reached, time elapsed, and units produced or units delivered. When an entity evaluates whether to apply an output method to measure its progress, the entity should consider whether the output selected would faithfully depict the entity's performance toward complete satisfaction of the performance obligation. An output method would not provide a faithful depiction of the entity's performance if the output selected would fail to measure some of the goods or services for which control has transferred to the customer. For example, output methods based on units produced or units delivered would not faithfully depict an entity's performance in satisfying a performance obligation if, at the end of the reporting period, the entity's performance has produced work in process or finished goods controlled by the customer that are not included in the measurement of the output.

606-10-55-20 [B18] Input methods recognize revenue on the basis of the entity's efforts or inputs to the satisfaction of a performance obligation (for example, resources consumed, labor hours expended, costs incurred, time elapsed, or machine hours used) relative to the total expected inputs to the satisfaction of that performance obligation. If the entity's efforts or inputs are expended evenly throughout the performance period, it may be appropriate for the entity to recognize revenue on a straight-line basis.

606-10-55-21 [B19] A shortcoming of input methods is that there may not be a direct relationship between an entity's inputs and the transfer of control of goods or services to a customer. Therefore, an entity should exclude from an input method the effects of any inputs that, in accordance with the objective of measuring progress in paragraph 606-10-25-31 [39], do not depict the entity's performance in transferring control of goods or services to the customer. For instance, when using a cost-based input method, an adjustment to the measure of progress may be required in the following circumstances:

a. When a cost incurred does not contribute to an entity's progress in satisfying the performance obligation. For example, an entity would not recognize revenue on the basis of costs incurred that are attributable to significant inefficiencies in the entity's performance that were not reflected in the price of the contract (for example, the costs of unexpected amounts of wasted materials, labor, or other resources that were incurred to satisfy the performance obligation).

b. When a cost incurred is not proportionate to the entity's progress in satisfying the performance obligation. In those circumstances, the best depiction of the entity's performance may be to adjust the input method to recognize revenue only to the extent of that cost incurred. For example, a faithful depiction of an entity's performance might be to recognize revenue at an amount equal to the cost of a good used to satisfy a performance obligation if the entity expects at contract inception that all of the following conditions would be met:

1. The good is not distinct.

2. The customer is expected to obtain control of the good significantly before receiving services related to the good.

3. The cost of the transferred good is significant relative to the total expected costs to completely satisfy the performance obligation.

4. The entity procures the good from a third party and is not significantly involved in designing and manufacturing the good (but the entity is acting as a principal in accordance with paragraphs 606-10-55-36 through 55-40 [B34 through B48]).

BC159. There are various methods that an entity might use to measure its progress toward complete satisfaction of a performance obligation. Because of the breadth of the scope of Topic 606 [IFRS 15], the Boards decided that it would not be feasible to consider all possible methods and prescribe when an entity should use each method. Accordingly, an entity should use judgment when selecting an appropriate method of measuring progress toward complete satisfaction of a performance obligation.

That does not mean that an entity has a "free choice." The guidance states that an entity should select a method of measuring progress that is consistent with the clearly stated objective of depicting the entity's performance—that is, the satisfaction of an entity's performance obligation in transferring control of goods or services to the customer.

BC160. To meet that objective of depicting the entity's performance, an entity would need to consider the nature of the promised goods or services and the nature of the entity's performance. For example, in a typical health club contract, the entity's promise is to stand ready for a period of time (that is, by making the health club available), rather than providing a service only when the customer requires it. In this case, the customer benefits from the entity's service of making the health club available. This is evidenced by the fact that the extent to which the customer uses the health club does not, in itself, affect the amount of the remaining goods or services to which the customer is entitled. In addition, the customer is obliged to pay the consideration regardless of whether it uses the health club. Consequently, in those cases, the entity would need to select a measure of progress based on its service of making goods or services available instead of when the customer uses the goods or services made available to them

BC161. The Boards decided that an entity should apply the selected method for measuring progress consistently for a particular performance obligation and also across contracts that have performance obligations with similar characteristics. An entity should not use different methods to measure its performance in satisfying the same or similar performance obligations, otherwise that entity's revenue would not be comparable in different reporting periods. The Boards also noted that if an entity were permitted to apply more than one method to measure its performance in fulfilling a performance obligation, it would effectively bypass the guidance on identifying performance obligations.

BC163. Output methods recognize revenue on the basis of direct measurements of the value to the customer of the goods or services transferred to date (for example, surveys of performance completed to date, appraisals of results achieved, milestones reached, time elapsed, and units delivered or units produced). When applying an output method, "value to the customer" refers to an objective measure of the entity's performance in the contract. However, value to the customer is not intended to be assessed by reference to the market prices or standalone selling prices of the individual goods or services promised in the contract, nor is it intended to refer to the value that the customer perceives to be embodied in the goods or services.

BC164. The Boards decided that, conceptually, an output measure is the most faithful depiction of an entity's performance because it directly measures the value of the goods or services transferred to the customer. However, the Boards observed that it would be appropriate for an entity to use an input method if that method would be less costly and would provide a reasonable proxy for measuring progress.

3. The new revenue standard provides the following guidance on when a good or service is distinct and, therefore, a separate performance obligation:

606-10-25-14 [22] At contract inception, an entity shall assess the goods or services promised in a contract with a customer and shall identify as a performance obligation each promise to transfer to the customer either:

a. A good or service (or bundle of goods or services) that is distinct

b. A series of distinct goods or services that are substantially the same and that have the same pattern of transfer to the customer.

606-10-25-19 [27] A good or service that is promised to a customer is distinct if both of the following criteria are met:

a. The customer can benefit from the good or service either on its own or together with other resources that are readily available to the customer (that is, the good or service is capable of being distinct).

b. The entity's promise to transfer the good or service to the customer is separately identifiable from other promises in the contract (that is, the good or service is distinct within the context of the contract).

4. When goods or services are not distinct, the new revenue standard provides the following guidance:

606-10-25-22 [30] If a promised good or service is not distinct, an entity shall combine that good or service with other promised goods or services until it identifies a bundle of goods or services that is distinct. In some cases, that would result in the entity accounting for all the goods or services promised in a contract as a single performance obligation.

5. The new revenue standard also includes the following guidance on nonrefundable upfront fees:

606-10-55-52 [B50] If the nonrefundable upfront fee relates to a good or service, the entity should evaluate whether to account for the good or service as a separate performance obligation in accordance with paragraphs 606-10-25-14 through 25-22 [22 through 30].

606-10-55-53 [B51] An entity may charge a nonrefundable fee in part as compensation for costs incurred in setting up a contract (or other administrative tasks as described in paragraph 606-10-25-17 [25]). If those setup activities do not satisfy a performance obligation, the entity should disregard those activities (and related costs) when measuring progress in accordance with paragraph 606-10-55-21 [B19]. That is because the costs of setup activities do not depict the transfer of services to the customer. The entity should assess whether costs incurred in setting up a contract have resulted in an asset that should be recognized in accordance with paragraph 340-40-25-5 [95].

6. The following guidance on costs to fulfil a contract relates to the guidance in the new revenue standard:

340-40-25-5 [95] An entity shall recognize an asset from the costs incurred to fulfil a contract only if those costs meet all of the following criteria:

a. The costs relate directly to a contract or to an anticipated contract that the entity can specifically identify (for example, costs relating to services to be provided under renewal of an existing contract or costs of designing an asset to be transferred under a specific contract that has not yet been approved).

b. The costs generate or enhance resources of the entity that will be used in satisfying (or in continuing to satisfy) performance obligations in the future.

c. The costs are expected to be recovered.

Appendix B – Example 53

> > Nonrefundable Upfront Fees

606-10-55-357 Example 53 illustrates the guidance in paragraphs 606-10-55-50 through 55-53 [B48 through B51] on nonrefundable upfront fees.

> > > Example 53—Nonrefundable Upfront Fee

606-10-55-358 An entity enters into a contract with a customer for one year of transaction processing services. The entity's contracts have standard terms that are the same for all customers. The contract requires the customer to pay an upfront fee to set up the customer on the entity's systems and processes. The fee is a nominal amount and is nonrefundable. The customer can renew the contract each year without paying an additional fee.

606-10-55-359 The entity's setup activities do not transfer a good or service to the customer and, therefore, do not give rise to a performance obligation.

606-10-55-360 The entity concludes that the renewal option does not provide a material right to the customer that it would not receive without entering into that contract (see paragraph 606-10-55-42 [B40]). The upfront fee is, in effect, an advance payment for the future transaction processing services. Consequently, the entity determines the transaction price, which includes the nonrefundable upfront fee, and recognizes revenue for the transaction processing services as those services are provided in accordance with paragraph 606-10-55-51 [B49].

___________ The IASB is the independent standard-setting body of the IFRS Foundation, a not-for-profit corporation promoting the adoption of IFRSs. For more information visit www.ifrs.org

The Financial Accounting Standards Board (FASB) is an independent standard-setting body of the Financial Accounting Foundation, a not-for-profit corporation. The FASB is responsible for establishing Generally Accepted Accounting Principles (GAAP), standards of financial accounting that govern the preparation of financial reports by public and private companies and not-for-profit organizations in the United States and other jurisdictions. For more information visit www.fasb.org

1 Paragraph 606-10-25-31 [39]

2 Paragraph 606-10-25-23 [31]

3 Paragraph 606-10-25-25 [33]

4 The FASB Board has proposed guidance in the Proposed Accounting Standards Update Revenue from Contracts with Customers (Topic 606): Identifying Performance Obligations and Licensing that amends paragraph 606-10-55-57 to clarify that an entity should consider the nature of its promise in granting a license that is combined with other goods or services into a single performance obligation.

Copyright #year# by Financial Accounting Foundation, Norwalk, Connecticut.

View image

View image