This paper has been prepared for discussion at a public meeting of the FASB | IASB Joint Transition Resource Group for Revenue Recognition. It does not purport to represent the views of any individual members of either board or staff. Comments on the application of U.S. GAAP or IFRS do not purport to set out acceptable or unacceptable application of U.S. GAAP or IFRS.

Purpose

1. Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers, and IFRS 15 Revenue from Contracts with Customers (collectively referred to as the “new revenue standard”), require that an entity estimate variable consideration using one of two methods: expected value or most likely amount. Stakeholders have questioned whether an entity is applying the portfolio practical expedient allowed by the new revenue standard when it considers evidence from other, similar contracts to develop an estimate of variable consideration using the expected value method. Stakeholders raised this question because the portfolio practical expedient can only be applied if the entity reasonably expects that the difference from applying the new revenue standard to a portfolio of contracts as compared to an individual contract would not result in a material effect on the financial statements. Stakeholders also have questioned whether the estimated transaction price using the expected value method can be for an amount that is not a possible outcome of the contract.

2. This paper summarizes the potential implementation issues that were reported to the staff. The staff will seek input from members of the FASB-IASB Joint Transition Resource Group for Revenue Recognition (TRG) on the potential implementation issues.

Accounting Guidance

3. See Appendix A for relevant accounting literature.

Question 1: Is an entity applying the portfolio practical expedient when it considers evidence from other, similar contracts to develop an estimate using the expected value method?

4. The staff understands that this question has been raised by stakeholders, in part, because of interpretations of Example 22, Right of Return, in the new revenue standard. The example states that the entity is applying the portfolio practical expedient, but it is unclear from the example how the application of the portfolio practical expedient affects the accounting.

5. To address the implementation question, the staff analyzed Example 22. The following stated facts from the example are relevant to this implementation issue (the complete example is included in Appendix A):

The entity enters into 100 contracts with customers, and each contract is for 1 product for $100 each (it is the same product in each contract). Unused products can be returned within 30 days for a refund and, therefore, the contracts include variable consideration.

The entity applies the portfolio practical expedient for the contracts in accordance with paragraph 606-10-10-4 [4].

The entity estimates the variable consideration using the expected value method and determines that 97 of the 100 products will not be returned.

The entity concludes that it is probable [highly probable] that a significant reversal in the cumulative amount of revenue recognized (that is, $9,700) will not occur as the uncertainty is resolved (that is, over the return period).

The entity recognizes the following journal entry (among others):

6. In this example, the entity selected the expected value method to estimate variable consideration because it would better predict the amount of consideration to which it will be entitled. The staff observes that there are two potential outcomes for each contract from the variability of product returns: the product either will be returned or will not be returned. That is, the revenue for each contract ultimately either will be $100 or will be $0. However, the entity concluded that the expected value is the appropriate method for estimating variable consideration, because the entity has a large number of contracts with similar characteristics. In order to estimate the expected value, the entity considers evidence from historical experience for this product and customer class and concludes that $97 is the expected value from each contract.

7. The example states that the entity applied the portfolio practical expedient in accordance with paragraph 606-10-10-4 [4]. The application of the portfolio practical expedient requires that the “entity reasonably expects that the effects on the financial statements of applying this guidance to the portfolio would not differ materially from applying this guidance to the individual contracts (or performance obligations) within that portfolio.” That is, when electing the portfolio practical expedient, the entity has concluded that there could be a difference in the accounting between the individual contract(s) and the portfolio of contracts. While the Boards indicated that they did not intend for entities to “quantitatively evaluate each outcome,” in applying the portfolio practical expedient, there would be a difference that could be assessed.

8. The example states that the contracts relate to the sale of a single product; therefore, the products are homogenous in nature. There is nothing in the example to indicate that there could be a difference between estimating variable consideration for returns for the individual contracts using the expected value method or the portfolio of contracts. That is, there is no reason that the entity needed to elect the portfolio practical expedient.

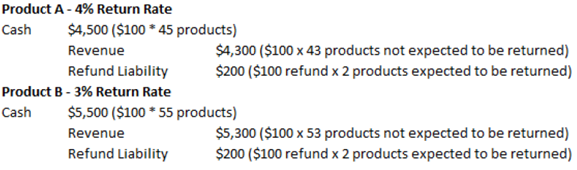

9. In contrast, consider the following change to the example that could result in a difference between the accounting for the individual contracts and the portfolio of contracts:

An entity enters into 100 contracts with customers. The 100 contracts are for 45 contracts for one unit of product A for $100 per unit and 55 contracts for one unit of product B for $100 per unit. Product A has a historical return rate of 4% and Product B has a historical return rate of 3%. However, the weighted-average return rate for Products A and B is about 3% because historically more of Product B has been sold than Product A.

10. Similar to the original example, the entity concludes that the expected value method best predicts the amount of consideration to which it will be entitled. In this case, the entity concludes that information about return rates for Product B are not relevant in estimating the return rate for Product A, and vice versa. To account for the individual contracts, the entity would make a separate estimate of variable consideration for Products A and B on the basis of its historical experience with returns for each product. The entity would recognize total revenue of $9,600, as follows (the return rate is applied to the number of products):

11. Alternatively, the entity could apply the portfolio practical expedient in paragraph 606-10-10-4 [4] if it reasonably expects that the difference between accounting for each individual contract ($9,600 of total revenue) would not vary materially from accounting for the portfolio of contracts ($9,700 of total revenue, which is based on applying an overall 3% return rate). The quantification of the difference is provided to illustrate application of the portfolio practical expedient. The new revenue standard does not require quantification; an entity is only required to conclude that there is a reasonable expectation that the effects on the financial statements from applying the guidance to a portfolio of contracts would not differ materially from applying this guidance to individual contracts within the portfolio.

12. The staff thinks that an entity can consider evidence from other, similar contracts to develop an estimate of variable consideration using the expected value method without applying the portfolio practical expedient. In order to make an estimate of variable consideration in a contract (and other estimates to account for a contract with a customer), an entity frequently will make judgments, in part, based on its historical experience with other, similar contracts. Considering historical experience does not necessarily mean the entity is applying the portfolio practical expedient. The staff observes that this view is further made clear by the guidance on estimating the standalone selling price of a good or service. Paragraph 606-10-32-34(a) [79(a)] states that a suitable method for estimating the standalone selling price of a good or service would include referring to prices of similar goods or services.

Question 2: Can the estimated transaction price under the expected value method be an amount that is not a possible outcome of an individual contract?

13. To illustrate stakeholders’ views on this question, consider the following example.

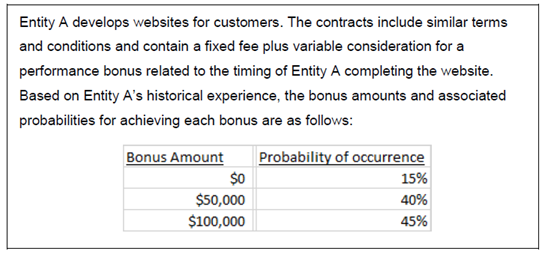

14. To estimate the variable consideration in a new contract with a customer, Entity A considers paragraph 606-10-32-8 [53] and concludes that the expected value method, as compared to the most likely amount method, would better predict the amount of consideration to which it will be entitled because the entity has a large number of contracts that have similar characteristics to the new contract. The expected value of the variable consideration is $65,000 ([$0 * 15%] + [$50,000 * 40%] + [$100,000 * 45%]). When considering the constraint on variable consideration, Entity A considered the factors that could increase the likelihood of a revenue reversal in paragraph 606-10-32-12 [57] and concluded that it has relevant historical experience with similar types of contracts and that the amount of consideration is not highly susceptible to factors outside of the entity’s influence. There are two views regarding the appropriate amount of variable consideration to include in the transaction price:

View A, variable consideration = $50,000, or

View B, variable consideration = $65,000.

View A: The transaction price should be constrained to the highest amount that is both a possible outcome of the contract and a probable [highly probable] outcome

15. Some reason that the variable consideration should be constrained to $50,000 because the individual contract can never result in $65,000 of variable consideration. Therefore, they think the $15,000 in excess of $50,000 is probable [highly probable] of being reversed, unless it is probable that the entity will earn the $100,000 bonus. Those with that view observe that when applying the constraint on variable consideration in accordance with paragraph 606-10-32-11 [56], an entity would only include an amount in the transaction price that is not probable [highly probable] of a significant revenue reversal. Assuming that $15,000 is significant in relation to this contract, those with this view think the entity should only include the probable [highly probable] amount that can actually be received from the individual contract (that is, $50,000).

16. Those with this view also point to paragraph 606-10-10-4 [4] and note that the new revenue standard specifies the accounting for an individual contract; therefore, they reason that an entity cannot recognize revenue for an amount that is not a potential outcome of the individual contract even if that amount is probable [highly probably] of occurrence in the context of a large number of contracts. Those with that view reason that the transaction price should reflect the amount the entity expects to be entitled to in the individual contract without regard to the context of a large number of contracts.

17. Some opponents of this view note that application of the constraint in this manner could result in an entity negating the expected value approach for estimating the transaction price, which would result in a de facto application of the most likely amount approach. Further, opponents point to other fact patterns involving variable consideration, such as product returns, for which they think application of View A would be inconsistent with the core principle of the new revenue standard. For example, consider a fact pattern in which an entity grants a right of return for one year and has significant historical evidence to indicate that product returns are consistently 40% with returns occurring ratably over the return period. Under View A, because there is only a 60% probability that an individual product is not returned, all revenue would be constrained until the right of return period has expired. If an entity does not recognize any revenue for any sale until the return period has expired, opponents argue that the core principle of the revenue standard would be violated. That is, the entity would not be recognizing revenue that depicts “the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.”

View B: The transaction price is not automatically reduced by the constraint on variable consideration

18. Proponents of View B think that the transaction price should be $65,000 in this example. They think that if an entity appropriately concludes that the expected value method better predicts the consideration to which it expects to be entitled, application of the constraint should not

automatically

negate the result of that estimation technique. It is important to emphasize, however, that in this example, the entity has concluded that none of the factors in paragraph 606-10-32-12 [57] or any other factors indicate a likelihood of a significant revenue reversal. In different circumstances, the entity might have been required to constrain its estimate of variable consideration, even though it used an expected value method. That said, the staff observes that application of the expected value method, which requires an entity to consider probability-weighted amounts, is complementary in some ways to the objective underlying the constraint on variable consideration. In developing its estimate of the transaction price in accordance with the expected value method, the entity has reduced the probability of a revenue reversal and might not need to constrain its estimate of variable consideration. The interaction between first estimating variable consideration and then assessing whether the variable consideration should be constrained is discussed in the Basis for Conclusions as follows:

BC215. Although some respondents explained that they reasoned that this guidance would inappropriately require a two-step process, the Boards observed that an entity would not be required to strictly follow those two steps if the entity’s process for estimating variable consideration already incorporates the principles on which the guidance for constraining estimates of variable consideration is based. For example, an entity might estimate revenue from sales of goods with a right of return. In that case, the entity might not practically need to estimate the expected revenue and then apply the constraint guidance to that estimate, if the entity’s calculation of the estimated revenue incorporates the entity’s expectations of returns at a level at which it is probable that the cumulative amount of revenue recognized would not result in a significant revenue reversal.

19. Additionally, those in support of View B do not think that the transaction price has to be a potential outcome of the individual contract in circumstances in which the entity concludes that using the expected value approach is the best method for estimating the transaction price. Consistent with that view, proponents think it would be inconsistent to develop an estimate of the expected value on the basis of historical experience, but then ignore the historical evidence when applying the constraint. They note that this view is consistent with the staff analysis of the objective of the constraint as articulated in Board Memo 162A (IASB Agenda Ref 7A). That paper noted the following in paragraph 26:

....an entity should use the same inputs as those used in determining the transaction price when applying the constraint because the measurement objective for determining the transaction price and applying the constraint are the same, ie predicting the amount of consideration the entity will be entitled to for providing its goods or services. For example, if an entity used a most likely outcome approach on a single contract to determine the transaction price, the entity would use the same inputs and unit of account when determining the application of the constraint.

20. Those that support View B think that $50,000 would be an appropriate estimated transaction price if the entity concluded that it should apply the most likely amount method for estimating variable consideration because the facts and circumstances are different than the example above. To illustrate, assume that Entity A has no other contracts with a performance bonus. In that scenario, Entity A would likely conclude that the most likely amount method would better predict the amount of consideration to which it is entitled because it does not have a large number of contracts with similar characteristics. The most likely amount is $100,000 (it is the outcome with the highest probability of being achieved), but it is not probable [highly probable] the entity will earn $100,000 (the probability estimate for this outcome is 45%). Therefore, when applying the constraint, Entity T includes $50,000 in the transaction price because it is probable [highly probable] that a significant reversal in the amount of cumulative revenue recognized will not occur (there is an 85% probability of the entity earning at least $50,000).

Question for the TRG Members

What are your views about the implementation issues discussed in this paper?

Appendix A: Relevant Accounting Guidance and Example

1. The new revenue standard requires an entity to estimate the amount of variable consideration that the entity will be entitled in exchange for transferring goods and services as follows:

606-10-32-8 [53] An entity shall estimate an amount of variable consideration by using either of the following methods, depending on which method the entity expects to better predict the amount of consideration to which it will be entitled:

The expected value—The expected value is the sum of probability-weighted amounts in a range of possible consideration amounts. An expected value may be an appropriate estimate of the amount of variable consideration if an entity has a large number of contracts with similar characteristics.

The most likely amount-The most likely amount is the single most likely amount in a range of possible consideration amounts (that is, the single most likely outcome of the contract). The most likely amount may be an appropriate estimate of the amount of variable consideration if the contract has only two possible outcomes (for example, an entity either achieves a performance bonus or does not).

2. The Boards’ basis for the two methods for estimating variable consideration follows:

BC195. The Boards decided to specify that an entity should estimate variable consideration using either the expected value or the most likely amount, depending on which method the entity expects will better predict the amount of consideration to which the entity will be entitled (see paragraph 606-10-32-8). The Boards noted that this is not intended to be a “free choice”; an entity needs to consider which method it expects to better predict the amount of consideration to which it will be entitled and apply that method consistently for similar types of contracts.

BC 200 The Boards observed that in some cases, a probability-weighted estimate (that is, an expected value) predicts the amount of consideration to which an entity will be entitled. For example, that is likely to be the case if the entity has a large number of contracts with similar characteristics. However, the Boards agreed with respondents that an expected value may not always faithfully predict the consideration to which an entity will be entitled. For example, if the entity is certain to receive one of only two possible consideration amounts in a single contract, the expected value would not be a possible outcome in accordance with the contract and, therefore, might not be relevant in predicting the amount of consideration to which the entity will be entitled. The Boards decided that in those cases, another method-the most likely amount method—is necessary to estimate the transaction price. This is because the most likely amount method identifies the individual amount of consideration in the range of possible consideration amounts that is more likely to occur than any other individual outcome.

3. The estimate for variable consideration should be constrained as follows:

606-10-32-11 [56] An entity shall include in the transaction price some or all of an amount of variable consideration estimated in accordance with paragraph 606-10-32-8only to the extent that it is probable [highly probable] that a significant reversal in the amount of cumulative revenue recognized will not occur when the uncertainty associated with the variable consideration is subsequently resolved.

4. The new revenue standard specifies the unit of account as the individual contract, but allows for a practical expedient when considering a portfolio of contracts as follows:

606-10-10-4 [4] This guidance specifies the accounting for an individual contract with a customer. However, as a practical expedient, an entity may apply this guidance to a portfolio of contracts (or performance obligations) with similar characteristics if the entity reasonably expects that the effects on the financial statements of applying this guidance to the portfolio would not differ materially from applying this guidance to the individual contracts (or performance obligations) within that portfolio. When accounting for a portfolio, an entity shall use estimates and assumptions that reflect the size and composition of the portfolio.

Example 22-Right of Return

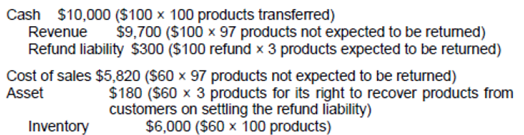

606-10-55-202 [IE110] An entity enters into 100 contracts with customers. Each contract includes the sale of 1 product for $100 (100 total products × $100 = $10,000 total consideration). Cash is received when control of a product transfers. The entity’s customary business practice is to allow a customer to return any unused product within 30 days and receive a full refund. The entity’s cost of each product is $60.

606-10-55-203 [IE111] The entity applies the guidance in this Topic to the portfolio of 100 contracts because it reasonably expects that, in accordance with paragraph 606-10-10-4, the effects on the financial statements from applying this guidance to the portfolio would not differ materially from applying the guidance to the individual contracts within the portfolio.

606-10-55-204 [IE112] Because the contract allows a customer to return the products, the consideration received from the customer is variable. To estimate the variable consideration to which the entity will be entitled, the entity decides to use the expected value method (see paragraph 606-10-32-8(a)) because it is the method that the entity expects to better predict the amount of consideration to which it will be entitled. Using the expected value method, the entity estimates that 97 products will not be returned.

606-10-55-205 [IE113] The entity also considers the guidance in paragraphs 606-10-32-11 through 32-13 on constraining estimates of variable consideration to determine whether the estimated amount of variable consideration of $9,700 ($100 x 97 products not expected to be returned) can be included in the transaction price. The entity considers the factors in paragraph 606-10-32-12 and determines that although the returns are outside the entity’s influence, it has significant experience in estimating returns for this product and customer class. In addition, the uncertainty will be resolved within a short time frame (that is, the 30-day return period). Thus, the entity concludes that it is probable that a significant reversal in the cumulative amount of revenue recognized (that is, $9,700) will not occur as the uncertainty is resolved (that is, over the return period).

606-10-55-206 [IE114] The entity estimates that the costs of recovering the products will be immaterial and expects that the returned products can be resold at a profit.

606-10-55-207 [IE115] Upon transfer of control of the 100 products, the entity does not recognize revenue for the 3 products that it expects to be returned. Consequently, in accordance with paragraphs 606-10-32-10 and 606-10-55-23, the entity recognizes the following:

___________ The IASB is the independent standard-setting body of the IFRS Foundation, a not-for-profit corporation promoting the adoption of IFRSs. For more information visit www.ifrs.org

The Financial Accounting Standards Board (FASB) is an independent standard-setting body of the Financial Accounting Foundation, a not-for-profit corporation. The FASB is responsible for establishing Generally Accepted Accounting Principles (GAAP), standards of financial accounting that govern the preparation of financial reports by public and private companies and not-for-profit organizations in the United States and other jurisdictions. For more information visit www.fasb.org

1 Paragraph 606-10-10-2 [2]

Copyright #year# by Financial Accounting Foundation, Norwalk, Connecticut.

View image

View image

View image

View image

View image

View image

View image

View image