The threshold for a reporting entity to adopt the liquidation basis of accounting is when liquidation is imminent, unless the entity follows a plan for liquidation which was specified at inception in its governing documents (e.g., its article of incorporation). When it is appropriate to apply the liquidation basis of accounting, it is not an election; a reporting entity should apply the guidance in

ASC 205-30 to determine when a liquidation is considered imminent and, consequently, when the liquidation basis of accounting is required.

ASC 205-30-25-2

Liquidation is imminent when either of the following occurs:

a. A plan for liquidation has been approved by the person or persons with the authority to make such a plan effective, and the likelihood is remote that any of the following will occur:

1. Execution of the plan will be blocked by other parties (for example, those with shareholder rights)

2. The entity will return from liquidation.

b. A plan for liquidation is imposed by other forces (for example, involuntary bankruptcy), and the likelihood is remote that the entity will return from liquidation.

Whether liquidation is imminent should be considered in light of the facts and circumstances and the actions of management regarding its plans for the reporting entity. Depending on a reporting entity’s bylaws or the laws of the state of incorporation, a voluntary plan of liquidation would ordinarily require approval by at least a simple majority of its shareholders. The liquidation basis of accounting should not be adopted in financial statements prior to such approval because until such approval, liquidation of the reporting entity is not “imminent.” If an involuntary plan of liquidation is imposed by other forces, the decision to liquidate is usually imposed by the Court and is outside the control of the reporting entity. In this case, it is remote that the reporting entity will return from liquidation and it should adopt liquidation basis accounting even if formal board approval is not obtained (because the decision to liquidate does not rest with the board). Management should consider seeking the guidance of legal counsel in determining when an involuntary liquidation is imminent.

ASC 205-30 does not consider the length of time the liquidation process could take as a factor in determining when the imminent threshold has been met. A reporting entity is required to adopt the liquidation basis of accounting as soon as its liquidation meets the definition of imminent, even if the actual liquidation event is 12 months or more in the future (or extends beyond the plan year in the case of employee benefit plans, as discussed further in

BLG 6.8.1). However, when the liquidation process is expected to occur over a lengthy period that includes significant operating decisions, the reporting entity should carefully consider whether it has met the requirements of

ASC 205-30-25-2.

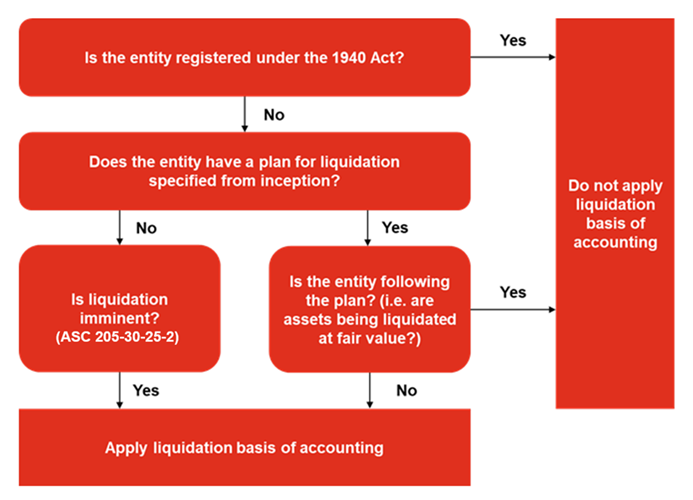

Figure BLG 6-2 illustrates the determination of when the liquidation basis of accounting should be adopted.

Figure BLG 6-2

Determination of when liquidation basis of accounting should be adopted

The liquidation basis is applied prospectively only from the day that liquidation becomes imminent, and so a reporting entity adopting the liquidation basis for the first time would not retrospectively adjust its historical financial statements. For practical reasons, opening account balances and adoption adjustments under the liquidation basis may be determined using a "convenience date." A convenience date is a date shortly before or after the date the criteria for adoption are met (such as the beginning or end of the month or quarter in which the criteria are met) and is used when the impact is not quantitatively and qualitatively material to the reporting entity's financial statements for all periods presented. Notwithstanding, the adoption date as presented on the financial statements and disclosed in the notes is usually the actual date the criteria were met. Generally, a convenience date should not cross a quarterly or annual reporting period. In instances when the imminent threshold is met after the balance sheet date but prior to the release of the financial statements, prior period financial statements should continue to be prepared on a going concern basis and appropriate subsequent event disclosures, which may include pro forma financial data for the liquidation basis of accounting, should be provided.

The liquidation basis of accounting does not apply to a planned wind-down of a reporting entity’s activities that occurs over time where the legal entity will be kept active and may continue or increase operations with an improvement in the business climate. In such circumstances, the resolution by the board of directors or other governing body is usually not clear that liquidation is imminent and it may be difficult for the reporting entity to assert that the likelihood it will return from liquidation is remote.

Example BLG 6-1, Example BLG 6-2, Example BLG 6-3, Example BLG 6-4, and Example BLG 6-5 demonstrate circumstances when it may or may not yet be appropriate to adopt the liquidation basis of accounting. Example BLG 6-5 and Example BLG 6-6 illustrate the timing of adoption of the liquidation basis of accounting.

EXAMPLE BLG 6-1

A reporting entity that keeps its operating license intact

A mortgage origination entity's management determines that the reporting entity will not process any new mortgages and will sell off its existing mortgage portfolio to third parties within the next six months. Following the distribution of the assets of the reporting entity, the business will not be dissolved as it holds a state mortgage license that the reporting entity's parent wants to keep intact because it may begin to originate mortgages once market conditions improve.

Should the reporting entity adopt the liquidation basis of accounting?

Analysis

No. The mortgage origination entity should not adopt the liquidation basis of accounting because its liquidation is not considered imminent. The reporting entity would not be able to assert that its return from liquidation is remote since it is keeping its mortgage license intact and may resume operations if market conditions improve.

EXAMPLE BLG 6-2

A reporting entity that retains its legal charter

The board of directors of a research entity decides that because of the loss of a patent, the long-term viability of the reporting entity is in doubt. The board authorizes management to sell the reporting entity's assets and settle all of its obligations, but there is no plan to make a final distribution of its assets or to dissolve its charter as the board explores other investment alternatives.

Should the reporting entity adopt the liquidation basis of accounting?

Analysis

No. The research entity should not adopt the liquidation basis of accounting because its liquidation is not considered imminent. While the reporting entity is disposing of its assets and settling its obligations, the entity's charter is neither being dissolved nor are the proceeds from the liquidation being distributed. As the board explores other investment alternatives, the reporting entity is a going concern since it is considering using the sale proceeds to enter a new business. The reporting entity would not qualify for the liquidation basis of accounting until its board of directors approves further actions, such as a full dissolution of the reporting entity's charter and distribution of any remaining proceeds to its shareholders.

EXAMPLE BLG 6-3

A reporting entity that files for Chapter 7 bankruptcy

Company A files a petition under Chapter 7 of the Bankruptcy Code, which involves an independent trustee taking over management of Company A for purposes of liquidating its assets.

Is liquidation imminent for purposes of adopting the liquidation basis of accounting?

Analysis

It depends. The filing of the petition under Chapter 7 is a significant event, and in most cases would necessitate the adoption of the liquidation basis of accounting. Generally, when the filing of a petition under Chapter 7 is voluntary, the plan would have been approved by the person or persons with the authority to make the plan for liquidation effective. When a reporting entity's filing under Chapter 7 is involuntary, by definition the plan for liquidation has been imposed by other forces. Whether voluntary or involuntary, it is generally unlikely that a reporting entity filing under Chapter 7 will return from liquidation. Of course, a reporting entity's facts and circumstances surrounding a Chapter 7 petition are unique, and so management should review the facts to ensure the criteria in

ASC 205-30-25-2 are met prior to adopting the liquidation basis of accounting.

EXAMPLE BLG 6-4

A reporting entity that is not legally dissolved

Fund A is not registered under the Investment Company Act of 1940 and its governing documents do not specify a contractual life. Management of Fund A intends to liquidate Fund A's investments whereby all investors will be fully redeemed and all expenses will be paid. Management does not intend to legally dissolve Fund A as the legal structure may be used in the future to start a new fund.

Should Fund A adopt the liquidation basis of accounting?

Analysis

It depends. Under

ASC 205, liquidation, whether compulsory or voluntary, is the process by which a reporting entity converts its assets to cash or other assets and settles its obligations with creditors in anticipation of the reporting entity ceasing all activities. Upon cessation of the reporting entity's activities, any remaining cash or other assets are distributed to the reporting entity's investors or other claimants. A fund's process to liquidate all assets, settle all debt, and distribute all net assets would most likely meet the definition of liquidation even if management does not legally dissolve the reporting entity after the liquidation process is completed.

However, in this scenario, an understanding of what the potential future use of the fund would be and the likelihood of such future use should be considered when determining whether adopting the liquidation basis of accounting is appropriate. A future likely use of the legal entity with similar or identical investment strategy to that of the recently liquidated fund should be considered as part of the analysis as to whether it is appropriate to adopt the liquidation basis of accounting.

EXAMPLE BLG 6-5

Timing of adoption of the liquidation basis of accounting

On June 30, 20X1, Company A was notified by its only customer that the customer will no longer order its product. Existing orders are expected to be completed by May 20X2. From July through December 20X1, Company A continued efforts to raise additional financing from venture capital groups and secure new customers. By December 15, 20X1, it was evident that these efforts would not be successful.

On March 1, 20X2, Company A obtains the required shareholder approval for a plan of liquidation that will be completed by May 20X2. Upon ceasing its operations, all employees will be terminated, and the reporting entity's assets will be liquidated to repay its creditors. Company A is preparing its December 31, 20X1, financial statements.

Should Company A adopt the liquidation basis of accounting in its December 31, 20X1, financial statements?

Analysis

No. In its December 31, 20X1 financial statements, Company A should apply the going concern basis of accounting as liquidation is not considered “imminent” at that date. Under

ASC 205-30, liquidation is considered “imminent” when either:

- the plan of liquidation has been approved by the person(s) with the authority to make such a plan effective, and the likelihood is remote that (1) execution of the plan will be blocked by other parties and (2) the reporting entity will return from liquidation, or

- when a plan of liquidation is imposed by other forces and the likelihood is remote that the reporting entity will return from liquidation.

Furthermore, the liquidation basis of accounting is applied prospectively only from the day that liquidation becomes imminent, and so a reporting entity adopting the liquidation basis of accounting for the first time would not retrospectively adjust its historical financial statements.

In this fact pattern, Company A’s liquidation does not meet the imminent threshold until the required shareholder approval is obtained. Although going concern accounting is utilized as of December 31, 20X1, given the significance of the subsequent event and the pending change in the basis of accounting, it may be necessary to provide a pro forma statement of net assets in liquidation giving effect to the change to the liquidation basis of accounting as if it had occurred on the date of the balance sheet. See

FSP 28.6.3.12.

EXAMPLE BLG 6-6

Use of convenience date

The criteria for liquidation being imminent are met under

ASC 205-30 on October 29, 20X1.

Can the liquidation basis of accounting be adopted by the reporting entity on October 31, 20X1?

Analysis

Assuming the reporting entity reports annually on December 31, 20X1, it would prepare its going concern financial statements for the January 1 through October 28, 20X1 period and its liquidation basis financial statements for the October 29 to December 31, 20X1 period. Alternatively, any activity between October 29 and 31 may be included in the October 28, 20X1 financial statements, if, after considering the impact of using a convenience date together with the effect of all other identified errors, the financial statements (all periods presented) are not considered to be materially misstated.