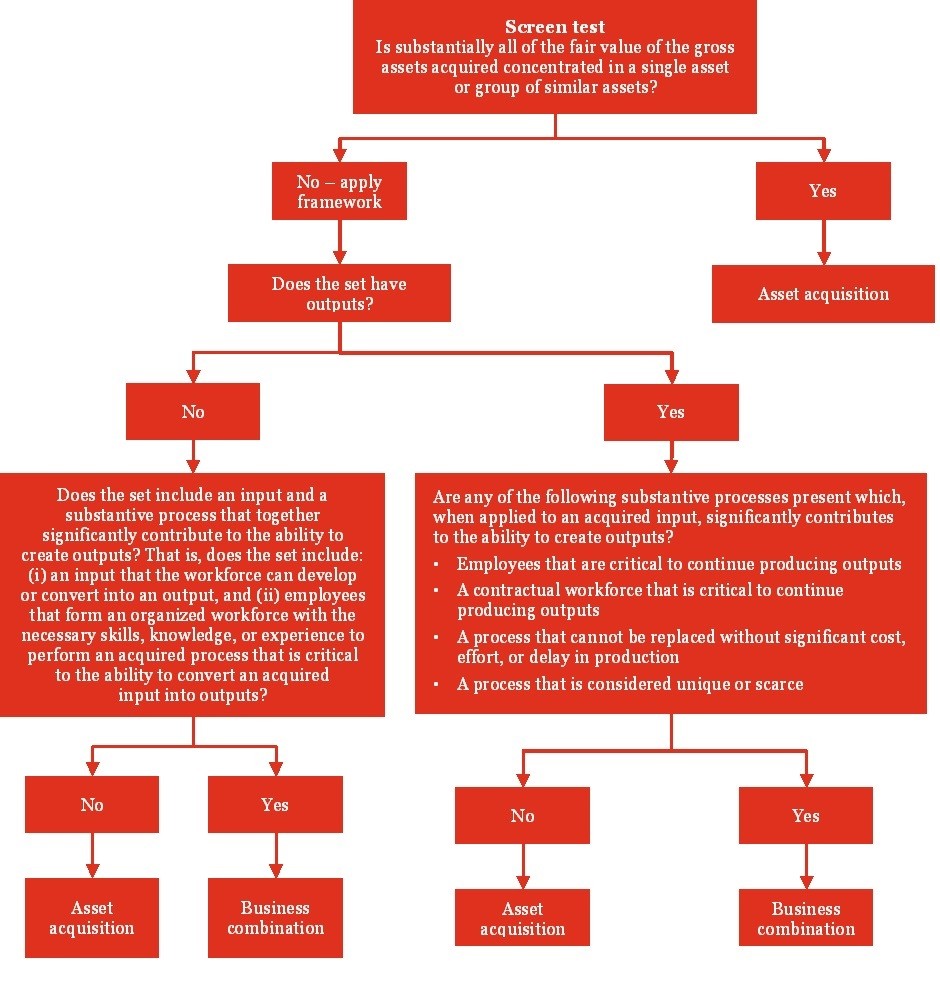

A set will have outputs when there is a continuation of revenue before and after the transaction. However, the continuation of revenues does not on its own indicate that both an input and a substantive process have been acquired. When determining whether a process has been acquired, the presence of contractual arrangements that provide for the continuation of revenues, such as customer contracts, customer lists, and leases, would not be indicative of an acquired process and should be excluded from the analysis.

ASC 805-10-55-5E includes four examples of substantive processes, which when applied to an acquired input, significantly contribute to the ability to create outputs.

ASC 805-10-55-5E

When the set has outputs (that is, there is a continuation of revenue before and after the transaction), the set will have both an input and a substantive process that together significantly contribute to the ability to create outputs when any of the following are present:

- Employees that form an organized workforce that has the necessary skills, knowledge, or experience to perform an acquired process (or group of processes) that when applied to an acquired input or inputs is critical to the ability to continue producing outputs. A process (or group of processes) is not critical if, for example, it is considered ancillary or minor in the context of all of the processes required to continue producing outputs.

- An acquired contract that provides access to an organized workforce that has the necessary skills, knowledge, or experience to perform an acquired process (or group of processes) that when applied to an acquired input or inputs is critical to the ability to continue producing outputs. An entity should assess the substance of an acquired contract and whether it has effectively acquired an organized workforce that performs a substantive process (for example, considering the duration and the renewal terms of the contract).

- The acquired process (or group of processes) when applied to an acquired input or inputs significantly contributes to the ability to continue producing outputs and cannot be replaced without significant cost, effort, or delay in the ability to continue producing outputs.

- The acquired process (or group of processes) when applied to an acquired input or inputs significantly contributes to the ability to continue producing outputs and is considered unique or scarce.

It is not uncommon for various processes to be performed by third parties through contractual arrangements (e.g., asset managers). However, just because the set includes access to a workforce does not necessarily mean that the workforce is substantive. Similar to the framework for when outputs are not present, an entity will need to consider if the workforce accessed through a contractual arrangement is critical to continue producing outputs. For instance, the duration and renewal terms of a contract may be an indication of how critical the functions performed are.

An organized workforce can be an indicator of a substantive process. However, when outputs are present, an organized workforce is not required for the set to be considered a business. A substantive process can exist without an organized workforce (e.g., if the set includes an automated process through acquired technology or infrastructure).

See Example BCG 1-3 for an example of an acquisition of brands, Example BCG 1-4 and Example BCG 1-5 for examples of an acquisition of a license agreement, and Example BCG 1-6 for an example of an acquisition of office buildings.

EXAMPLE BCG 1-3

Acquisition of brands

Company T is a global beverage manufacturer. Company T sells the worldwide rights of its oat milk brand, including all related intellectual property, to Company A. Company A also acquires (1) existing customer contracts, and (2) an at-market supply contract with the manufacturer of the oat milk, but it does not acquire any employees.

Has Company A acquired a business or a group of assets?

Analysis

The set is not a business. Since the set includes outputs through the continuation of revenues with customers, Company A would evaluate whether there is an acquired substantive process. Revenue contracts with customers are excluded from the analysis. The set does not include an organized workforce and the oat milk production process was not acquired by Company A; therefore, no substantive processes were acquired. Although it is likely that economic goodwill exists as a result of revenue derived from future customers, the goodwill will be reflected in the fair value of the assets acquired.

EXAMPLE BCG 1-4

Acquisition of a license agreement

Pharma Co. is a clinical-stage biopharmaceutical company that has an advanced drug in Phase 2 of clinical trials. Company A enters into a license agreement with Pharma Co. for the exclusive global license to the drug’s intellectual property, including R&D, manufacturing, and commercialization. No employees or other assets are acquired with the license agreement. The drug being licensed is not yet generating revenues. Company A also enters into two limited-time period arrangements at market rates, including a supply arrangement for product materials and an outsourced service arrangement (for development and clinical trials).

Is the arrangement the acquisition of a business?

Analysis

No. The acquired group is not a business.

Company A determined there is nominal fair value ascribed to the supply arrangement and outsourced service arrangement because the contracts are short-term and at market rates. Therefore, Company A would conclude that the license agreement is the only identifiable asset acquired with significant value. As a result, the set would meet the screen and would not be a business combination. Even if the set was assessed under the more detailed framework, since no employees were acquired and there is no continuation of revenue, the set does not contain outputs or a substantive process.

EXAMPLE BCG 1-5

Acquisition of a license agreement

Pharma Co. is a clinical-stage biopharmaceutical company that has an advanced drug in Phase 2 of clinical trials. Company A enters into a license agreement with Pharma Co. for the exclusive global license to the drug’s intellectual property, including R&D, manufacturing, and commercialization. The drug being licensed is not yet generating revenues. Concurrently, Company A acquires a subsidiary of Pharma Co. that includes experienced management and scientists as well as a corporate headquarters building, including a research lab with equipment necessary to develop the drug. Company A also enters into two limited-time period arrangements at market rates, including a supply arrangement for product materials and an outsourced service arrangement (for development and clinical trials).

Is the arrangement the acquisition of a business?

Analysis

Yes. The acquired group is a business. The identifiable assets in the set include the license agreement as well as the headquarters building, research lab, and equipment, which Company A determined have an aggregate fair value equal to 30% of the total consideration. As a result, the set does not meet the screen and the framework must be assessed.

Although the set does not have outputs, Company A would likely conclude that the workforce has the necessary skills, knowledge, and experience to continue or expand existing R&D activities. The experienced management and scientists represent an organized workforce that when applied to the acquired inputs (IPR&D) significantly contribute to the ability to create outputs.

EXAMPLE BCG 1-6

Acquisition of office buildings

Company T manages a portfolio of office buildings. Company T has a contract with a property management company. The executives of Company T are responsible for key strategic decisions, including identifying new properties to acquire. The property managers perform the primary duties related to tenant and lease management and property-level accounting. Company T has 25 domestic properties across five different states and each office building is diversified in terms of design construction.

Company A acquires Company T. At closing, the former executives of Company T become senior executives of Company A. None of the other employees of Company T join Company A. Additionally, Company A does not acquire the contract with the property management company.

Has Company A acquired a business?

Analysis

Yes. The acquired group is a business. The office buildings are not considered similar as the risks are significantly different (e.g., different geography, design) and may produce different cash flows throughout the period. As a result, the set does not meet the screen and the framework would need to be assessed.

Employees that form an organized workforce for property management services were not obtained since the property management contract was not acquired. However, the former executives are critical employees (due to the executive nature of their positions), which together with the continuation of revenue, indicates that the set includes a substantive process and is a business.