Search within this section

Select a section below and enter your search term, or to search all click Business combinations and noncontrolling interests, global edition

Favorited Content

Scenarios |

|||

Acquirer’s obligation |

Replacement of awards |

Expiration of acquiree awards |

Accounting |

1. The acquirer is obligated1 to issue replacement awards.

|

The acquirer issues replacement awards.

|

Not relevant.

|

The awards are considered in the determination of the amount of consideration transferred for the acquiree or for postcombination vesting.

|

2. The acquirer is not obligated1 to issue replacement awards to the acquiree.

|

The acquirer issues replacement awards.

|

The acquiree awards would otherwise expire.

|

The entire fair value of the replacement awards is recognized as compensation cost in the postcombination period.

|

3. The acquirer is not obligated1 to issue replacement awards to the acquiree.

|

The acquirer does not issue replacement awards. The acquiree awards remain outstanding postcombination as a noncontrolling interest.

|

The acquiree awards would not otherwise expire.

|

The acquirer could account for the continuation of the awards as if the acquirer was obligated to issue replacement awards (see Scenario 1 above).

Alternatively, the acquirer could account for the awards separate from the business combination as new grants and recognize the fair value of the awards as compensation cost in the postcombination period.

|

4. The acquirer is not obligated1 to issue replacement awards to the acquiree.

|

The acquirer issues replacement awards.

|

The acquiree awards would not otherwise expire.

|

Because the awards would not otherwise expire, if the acquirer had not issued replacement awards, the acquiree awards would have remained outstanding postcombination as a noncontrolling interest. The decision to issue replacement awards would then be viewed as an exchange of awards of the subsidiary (acquiree) for awards of the parent (acquirer), which is subject to modification accounting in accordance with ASC 718.

Therefore, similar to Scenario 3, the acquirer could account for the awards as if the acquirer was obligated to issue replacement awards. Alternatively, the acquirer could account for the awards separate from the business combination as new grants and recognize the fair value of the awards as compensation cost in the postcombination period.

|

Excerpt ASC 805-30-55-11

…if the fair-value-based measure of the portion of a replacement award attributed to precombination vesting is $100 and the acquirer expects that the service will be rendered for only 95 percent of the instruments awarded, the amount included in consideration transferred in the business combination is $95.

Total fair value |

% Vesting in year 1 |

Graded-vesting attributed in year 1 |

|

Tranche 1 |

$25 |

100% |

$25.00 |

Tranche 2 |

25 |

50% |

12.50 |

Tranche 3 |

25 |

33% |

8.33 |

Tranche 4 |

25 |

25% |

6.25 |

Total |

$100 |

$52.08 |

Replacement awards |

Total fair value |

% Vesting at acquisition date |

Graded-vesting attributed to precombination vesting |

Tranche 3 |

$200 |

83.3% 1 |

$167 |

Tranche 4 |

200 |

62.5% 2 |

125 |

Tranche 5 |

200 |

50.0% 3 |

100 |

Total |

$600 |

$392 |

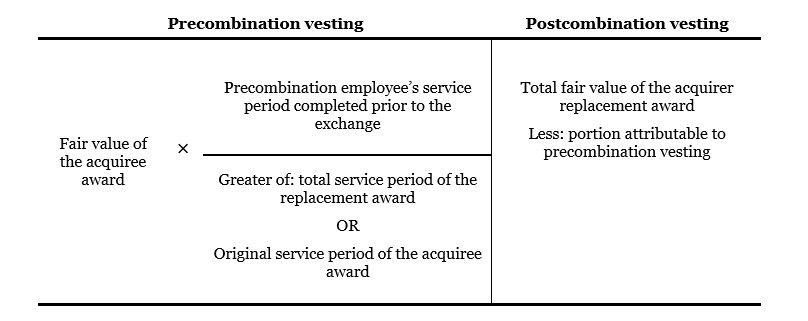

Acquiree’s awards |

Acquirer’s replacement awards |

Greater of total service period or original service period |

Fair value attributable to precombination vesting |

Fair value attributable to postcombination vesting |

Scenario 1:

|

||||

4 years of service required under original terms. All required services rendered prior to acquisition.

|

No service required after the acquisition date.

|

4 years. The original service period and the total vesting period are the same.

|

100% (4 years precombination service/4 years total service).

|

0%

|

Scenario 2:

|

||||

4 years of service required under original terms. 3 years of service rendered prior to acquisition.

|

1 year of service required after the acquisition date.

|

4 years (3 years prior to acquisition plus 1 year after acquisition). The original service period and the total service period are the same.

|

75% (3 years precombination service/4 years total service).

|

25% (total fair value of the replacement award less the 75% for precombination vesting). This amount is recognized in the postcombination financial statements over the remaining service period of 1 year.

|

Scenario 3:

|

||||

4 years of service required under original terms. 4 years of service rendered prior to acquisition.

|

1 year of service required after the acquisition date. The grantee has agreed to the additional year of service because the fair value of the replacement awards is greater than the fair value of the acquiree awards.

|

5 years (4 years completed prior to acquisition plus 1 year required after acquisition). The total service period of 5 years is greater than the original service period of 4 years.

|

80% of the acquiree award (4 years precombination service/5 years total service).

|

20% of the acquiree award and the excess fair value of the replacement award (total fair value of the replacement award less the 80% for precombination vesting). This amount is recognized in the postcombination financial statements over the remaining service period of 1 year.

|

Scenario 4:

|

||||

4 years of service required under original terms. 1 year of service rendered prior to acquisition.

|

2 years of service required after the acquisition date. Therefore, the replacement awards require one less year of service.

|

4 years (since only 2 years of service are required postcombination, the total service period for the replacement awards is 3 years, which is less than the original service period of 4 years). Therefore, the original service period is greater than the total service period.

|

25% (1 year precombination service/4 years original service period).

|

75% (total fair value of the replacement award less the 25% for precombination vesting). This amount is recognized in the postcombination financial statements over the remaining service period of 2 years.

|

Scenario 5:

|

||||

4 years of service required under original terms. 3 years of service rendered prior to acquisition. There was no change in control clause in the terms of the acquiree awards.

|

No service required after the acquisition date.

|

4 years (since no additional service is required, the total service period for the replacement awards is 3 years, which is less than the original service period of 4 years). Therefore, the original service period is greater than the total service period.

|

75% (3 years precombination service / 4 years original service period).

|

25% (total fair value of the replacement award less the 75% for precombination vesting). This amount is recognized in the postcombination financial statements immediately because no future service is required.

|

Scenario 6:

|

||||

4 years of service required under original terms. 3 years of service rendered prior to acquisition. There was a change in control clause in the original terms of the acquiree awards when granted that accelerated vesting upon a change in control.

|

No service required after the acquisition date.

|

Not applicable. Because the awards contain a pre-existing change in control clause, the total fair value of the acquiree awards is attributable to precombination vesting.

|

100%. For acquiree awards with a change in control clause that accelerates vesting, the total fair value of the acquiree awards is attributable to precombination vesting.

|

0%. For acquiree awards with a pre-existing change in control clause, no amount is attributable to postcombination vesting because there is no future service required.

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Business combinations and noncontrolling interests, global edition