Search within this section

Select a section below and enter your search term, or to search all click Consolidation and equity method of accounting

Favorited Content

Fees paid to a legal entity’s decision maker(s) or service provider(s) are not variable interests if all of the conditions below are met:

Fees or payments in connection with agreements that expose a reporting entity (the decision maker or the service provider) to risk of loss in the VIE would not be eligible for the evaluation in paragraph 810-10-55-37. Those fees include, but are not limited to, the following:

Excerpt from BC69 in ASU 2015-02

Current GAAP uses the term common control in multiple contexts, and the term is not defined in the Master Glossary. Therefore, for purposes of evaluating the criteria in paragraphs 810-10-25-42, 810-10-25-44A, and 810-10-55-37D, the Board’s intent was for the term to include subsidiaries controlled (directly or indirectly) by a common parent, or a subsidiary and its parent.

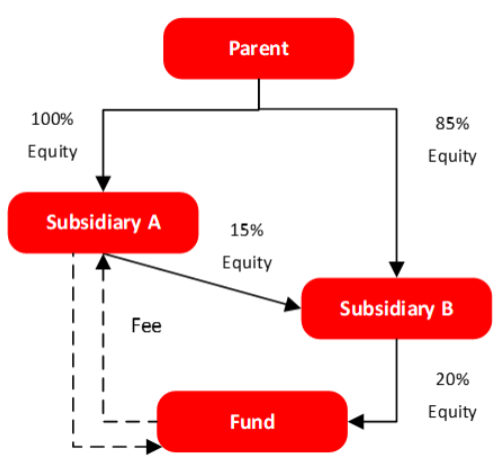

For purposes of evaluating the conditions in paragraph 810-10-55-37, any variable interest in an entity that is held by a related party of the decision maker or service provider should be considered in the analysis. Specifically, a decision maker or service provider should include its direct variable interests in the entity and its indirect variable interests in the entity held through related parties, considered on a proportionate basis. For example, if a decision maker or service provider owns a 20 percent interest in a related party and that related party owns a 40 percent interest in the entity being evaluated, the decision maker’s or service provider’s interest would be considered equivalent to an 8 percent direct interest in the entity for the purposes of evaluating whether the fees paid to the decision maker(s) or the service provider(s) are not variable interests (assuming that they have no other relationships with the entity). The term related parties in this paragraph refers to all parties as defined in paragraph 810-10-25-43, with the following exceptions:

Excerpt from ASC 810-10-55-37D

For purposes of evaluating the conditions in paragraph 810-10-55-37, the quantitative approach described in the definitions of the terms expected losses, expected residual returns, and expected variability is not required and should not be the sole determinant as to whether a reporting entity meets such conditions.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Consolidation and equity method of accounting