Search within this section

Select a section below and enter your search term, or to search all click Consolidation and equity method of accounting

Favorited Content

Area |

Voting interest entity model |

Variable interest entity model |

|---|---|---|

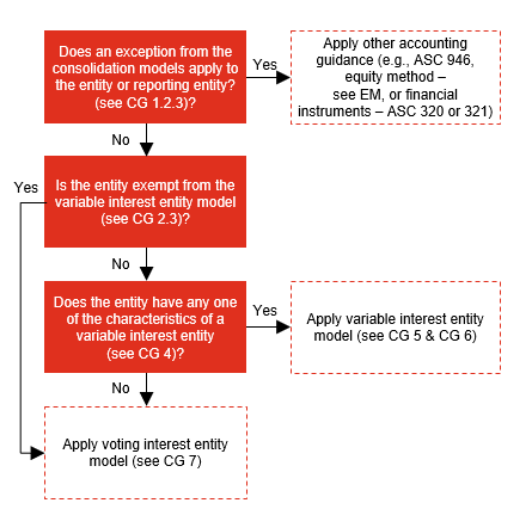

Definition of control (controlling financial interest)

|

For legal entities other than partnerships, the usual condition for control is ownership, directly or indirectly, of more than 50% of the outstanding voting shares over an entity.

For limited partnerships and similar entities, the usual condition for control is ownership, directly or indirectly, of more than 50% of a limited partnership’s kick-out rights (i.e., having the ability to replace the general partner or to liquidate the entity).

|

A party has control if it has both:

|

Related party considerations

|

No specific guidance

|

Interests held by related parties have the potential to impact a number of areas, including whether:

|

Participating rights

|

Defined as rights to block or participate in certain significant financial and operating decisions of the entity that are made in the ordinary course of business

Substantive participating rights over a significant activity (e.g., budgets) held by a noncontrolling investor preclude the majority shareholder from consolidating

The voting interest definition of participating rights is applied for determining if a limited partnership is a VIE

|

Defined as rights to block or participate in actions through which power to direct the activities that most significantly impact the entity’s performance are exercised

To be substantive and preclude the party with decision making power from consolidating, the participating rights must enable the holder to participate in all significant activities, and must be unilaterally exercisable by a single party

|

Disclosures

|

Limited required disclosures for consolidated subsidiaries that are voting entities; however, consideration is given to disclosures on key judgments (see FSP 18.5)

|

Incremental disclosures are required for reporting entities that are the primary beneficiary and also for other reporting entities that hold variable interests in a VIE. In addition, incremental disclosures about support arrangements and financial support provided to money market funds are required (see FSP 18.4 for further discussion on the disclosures)

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Consolidation and equity method of accounting