A fair value hedge is used to manage an exposure to changes in the fair value of a recognized asset or liability (e.g., fixed-rate debt) or an unrecognized firm commitment (e.g., the commitment to buy a fixed quantity of gold at a fixed price at a future date). A fair value hedge can be of either a financial or nonfinancial item, but fair value hedges of financial assets and liabilities are more common.

If a derivative qualifies as a fair value hedging instrument, the gain or loss on the portion of the derivative designated as a fair value hedge will still be recognized in earnings currently. However, a reporting entity would also recognize in earnings the changes in the value of the hedged asset, liability, or firm commitment due to the hedged risk through a basis adjustment to the hedged item. These two changes in fair value would offset one another in whole or in part and are reported in the same income statement line item as the hedged risk.

Example DH 5-2 illustrates a fair value hedge of a fixed-rate loan.

EXAMPLE DH 5-2

Fair value hedge of a fixed-rate loan

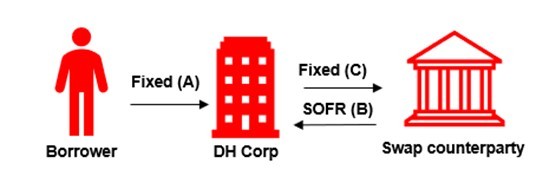

DH Corp invests in a fixed-rate loan that will be due in 10 years. It will be entitled to monthly interest payments at a fixed rate.

As market interest rates move over the term of the loan, the fair value of the loan will change. DH Corp is hedging SOFR as a benchmark interest rate (see

DH 6.4.5.1). All else being equal, as SOFR decreases, the value of its investment will increase because the contractual fixed interest payments will be above market. Similarly, all else being equal, if SOFR increases, the value of its investment will decrease. DH Corp is exposed to the risk of changes in the benchmark interest rate (SOFR Overnight Index Swap Rate).

To manage its exposure to changes in the fair value of its investment caused by changes in SOFR, DH Corp enters into a receive-SOFR and pay-fixed swap.

The fixed payments it receives from its investment (A) will be offset by the fixed payments it needs to make to the swap counterparty (C). Its net position will be the right to receive monthly SOFR payments (B).

How should DH Corp recognize the swap?

Analysis

DH Corp would recognize the changes in fair value of the derivative directly in earnings in the periods in which they occur. If DH Corp qualifies and elects to apply fair value hedge accounting, it would record a basis adjustment on the debt equal to the change in fair value of the debt that is attributable to the changes in the benchmark interest rate (SOFR Overnight Index Swap Rate). The changes in the value of the derivative and the changes in the value of the hedged item would be reported in interest income, offsetting each other to the extent the hedge is effective.

Had DH Corp not elected or qualified for hedge accounting, it would not record the basis adjustment on the investment, and there would be more volatility in earnings because the change in fair value of the derivative would not be offset.