Search within this section

Select a section below and enter your search term, or to search all click Derivatives and hedging

Favorited Content

Excerpt from 815-25-35-1

Excerpt from ASC 815-20-25-12(f)

Excerpt from ASC 815-20-25-12

Excerpt from ASC 815-20-25-43(c)

Excerpt from ASC 815-20-25-12(b)

Excerpt from ASC 815-20-55-14

If the change in fair value of a hedged portfolio attributable to the hedged risk was 10 percent during a reporting period, the change in the fair values attributable to the hedged risk for each item constituting the portfolio should be expected to be within a fairly narrow range, such as 9 percent to 11 percent. In contrast, an expectation that the change in fair value attributable to the hedged risk for individual items in the portfolio would range from 7 percent to 13 percent would be inconsistent with requirement in that paragraph [ASC 815-20-25-12(b)(1)].

In aggregating loans in a portfolio to be hedged, an entity may choose to consider some of the following characteristics, as appropriate:

Partial definition from the Master Glossary

Interest Rate Risk: For recognized fixed-rate financial instruments, interest rate risk is the risk of changes in the hedged item’s fair value attributable to changes in the designated benchmark interest rate. For forecasted issuances or purchases of fixed-rate financial instruments, interest rate risk is the risk of changes in the hedged item’s cash flows attributable to changes in the designated benchmark interest rate.

Definition from the ASC Master Glossary

Under this method, the change in a hedged item’s fair value attributable to changes in the benchmark interest rate for a specific period is determined as the difference between two present value calculations that use the remaining cash flows as of the end of the period and reflect in the discount rate the effect of the changes in the benchmark interest rate during the period.

Excerpt from ASC 815-25-55-56

Both present value calculations are computed using the estimated future cash flows for the hedged item, which would be either its remaining contractual coupon cash flows or the LIBOR benchmark rate component of the remaining contractual coupon cash flows determined at hedge inception as illustrated by the following Cases:

Year |

SOFR swap rate |

||

|---|---|---|---|

20X2

|

7%

|

||

20X3

|

6.5%

|

||

20X4

|

6.0%

|

||

20X5

|

5.5%

|

||

20X6

|

5.0%

|

||

20X7

|

4.5%

|

Dr. Interest expense

|

$1,713

|

||

Cr. Debt

|

$1,713

|

||

To record the change in fair value of debt for change in benchmark interest rates

($7,000×[(1-(1.065)-4)×(0.065)-1]+$100,000×(1.065)-4 = $101,713 minus $100,000) |

|||

Dr. Swap contract

|

$1,713

|

||

Cr. Interest expense

|

$1,713

|

||

To record the change in fair value of the swap

($7,000×[(1-(1.065)-4)×(0.065)-1]- $6,500×[(1-(1.065)-4)×(0.065)-1]) |

|||

Dr. Interest expense

|

$10,000

|

||

Cr. Cash

|

$10,000

|

||

To record payment of interest on the debt ($100,000 @ 10%)

|

|||

Note: No cash settlement on the swap to be recorded as the fixed and floating legs were both 7% for 20x3

|

|||

Dr. Interest expense

|

$960

|

||

Cr. Debt

|

$960

|

||

To record the change in fair value of debt for change in benchmark interest rates

($7,000×[(1-(1.06)-3)×(0.06)-1]+$100,000×(1.06)-3 = $102,673 less $101,713) |

|||

Dr. Swap contract

|

$960

|

||

Cr. Interest expense

|

$960

|

||

To record the change in fair value of the swap

($7,000×[(1-(1.06)-3)×(0.06)-1]-$6,000×[(1-(1.06)-3)×(0.06)-1] = $2,673 less $1,713) |

|||

Dr. Interest expense

|

$10,000

|

||

Cr. Cash

|

$10,000

|

||

To record payment of interest on the debt ($100,000 @ 10%)

|

|||

Dr. Cash

|

$500

|

||

Cr. Interest expense

|

$500

|

||

To record the settlement on the swap (receive fixed $7,000, pay float $6,500)

|

|||

Dr. Interest expense

|

$96

|

||

Cr. Debt

|

$96

|

||

To record the change in fair value of debt for change in benchmark interest rates

($7,000×[(1-(1.055)-2)×(0.055)-1]+$100,000×(1.055)-2 = $102,769 less $102,673) |

|||

Dr. Swap contract

|

$96

|

||

Cr. Interest expense

|

$96

|

||

To record the change in fair value of the swap

($7,000×[(1-(1.055)-2)×(0.055)-1]- $5,500×[(1-(1.055)-2)×(0.055)-1] = $2,769 less $2,673) |

|||

Dr. Interest expense

|

$10,000

|

||

Cr. Cash

|

$10,000

|

||

To record payment of interest on the debt ($100,000 @ 10%)

|

|||

Dr. Cash

|

$1,000

|

||

Cr. Interest expense

|

$1,000

|

||

To record the settlement on the swap (receive fixed $7,000, pay float $6,000)

|

|||

Dr. Debt

|

$865

|

||

Cr. Interest expense

|

$865

|

||

To record the change in fair value of debt for change in benchmark interest rates

($7,000×[(1-(1.05)-1)×(0.05)-1]+$100,000×(1.05)-1 = $101,904 less $102,769) |

|||

Dr. Interest expense

|

$865

|

||

Cr. Swap contract

|

$865

|

||

To record the change in fair value of the swap

($7,000×[(1-(1.05)-1)×(0.05)-1]- $5,000×[(1-(1.05)-1)×(0.05)-1] = $1,904 less $2,769) |

|||

Dr. Interest expense

|

$10,000

|

||

Cr. Cash

|

$10,000

|

||

To record payment of interest on the debt ($100,000 @ 10%)

|

|||

Dr. Cash

|

$1,500

|

||

Cr. Interest expense

|

$1,500

|

||

To record the settlement on the swap (receive fixed $7,000, pay float $5,500)

|

|||

Dr. Debt

|

$1,904

|

||

Cr. Interest expense

|

$1,904

|

||

To record the change in fair value of debt for change in benchmark interest rates

($7,000×[(1-(1.045)-0)×(0.045)-0]+$100,000×(1.045)-0 = $100,000 less $101,904) |

|||

Dr. Interest expense

|

$1,904

|

||

Cr. Swap contract

|

$1,904

|

||

To record the change in fair value of the swap

No future settlements as swap has matured so fair value is zero ($0-$1,904) |

|||

Dr. Interest expense

|

$10,000

|

||

Cr. Cash

|

$10,000

|

||

To record payment of interest on the debt ($100,000 @ 10%)

|

|||

Dr. Cash

|

$2,000

|

||

Cr. Interest expense

|

$2,000

|

||

To record the settlement on the swap (receive fixed $7,000, pay float $5,000)

|

|||

Year |

SOFR swap rate |

||

|---|---|---|---|

20X2

|

7%

|

||

20X3

|

6.5%

|

||

20X4

|

6.0%

|

||

20X5

|

5.5%

|

||

20X6

|

5.0%

|

||

20X7

|

4.5%

|

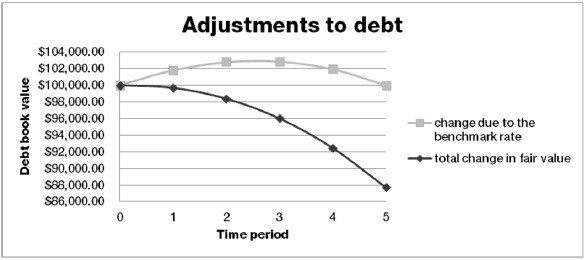

Change in present value of the cash flows due to both interest rates and time remaining until maturity |

|||||||

|---|---|---|---|---|---|---|---|

Date

|

12/31/X2

|

12/31/X3

|

12/31/X4

|

12/31/X5

|

12/31/X6

|

12/31/X7

|

Totals

|

Present value (PV)

|

$112,301

|

$111,990

|

$110,692

|

$108,308

|

$104,762

|

$100,000

|

|

Total change in present value (TC)

|

N/A

|

$310

|

$1,298

|

$2,384

|

$3,547

|

$4,762

|

$12,301

|

Isolate the change in time adjustment under Example 11 method while keeping rates constant at 7% |

|||||||

|---|---|---|---|---|---|---|---|

Date

|

12/31/X2

|

12/31/X3

|

12/31/X4

|

12/31/X5

|

12/31/X6

|

12/31/X7

|

|

Present value

|

$112,301

|

$110,162

|

$107,873

|

$105,424

|

$102,804

|

$100,000

|

|

Change in present value due to passage of time (∆ t)

|

N/A

|

$2,139

|

$2,289

|

$2,449

|

$2,620

|

$2,804

|

$12,301

|

Compute changes in fair value due to changes in the benchmark interest rate |

|||||||

|---|---|---|---|---|---|---|---|

Date

|

12/31/X2

|

12/31/X3

|

12/31/X4

|

12/31/X5

|

12/31/X6

|

12/311/X7

|

|

Total change in present value

|

$310

|

$1,298

|

$2,384

|

$3,547

|

$ 4,762

|

$12,301

|

|

Less impact of passage of time

|

–∆ t

|

$ 2,139

|

$2,289

|

$2,449

|

$2,620

|

$2,804

|

$12,301

|

Change in present value due to changes in benchmark interest rate

|

($1,829)

|

($991)

|

($65)

|

$927

|

$1,958

|

$0

|

|

a

|

c

|

e

|

g

|

i

|

|||

Change in fair value of the swap

|

$1,713

|

$960

|

$96

|

($865)

|

($1,905)

|

$0

|

|

b

|

d

|

f

|

h

|

j

|

|||

Earnings impact – difference in interest expense

|

($116)

|

($30)

|

$31

|

$62

|

$53

|

||

Dr. Interest expense

|

$1,829

|

||

Cr. Debt

|

$1,829

|

||

To record the change in fair value of debt for change in benchmark interest rates (a)

|

|||

Dr. Swap contract

|

$1,713

|

||

Cr. Interest expense

|

$1,713

|

||

To record the change in fair value of the swap (b)

|

|||

Dr. Interest expense

|

$10,000

|

||

Cr. Cash

|

$10,000

|

||

To record payment of interest on the debt ($100,000 @ 10%)

|

|||

Note: No cash settlement on the swap to be recorded, as the fixed and floating legs were both 7% for 20x3

|

|||

Dr. Interest expense

|

$991

|

||

Cr. Debt

|

$991

|

||

To record the change in fair value of debt for change in benchmark interest rates (c)

|

|||

Dr. Swap contract

|

$960

|

||

Cr. Interest expense

|

$960

|

||

To record the change in fair value of the swap (d)

|

|||

Dr. Interest expense

|

$10,000

|

||

Cr. Cash

|

$10,000

|

||

To record payment of interest on the debt ($100,000 @ 10%)

|

|||

Dr. Cash

|

$500

|

||

Cr. Interest expense

|

$500

|

||

To record the settlement on the swap (receive fixed $7,000, pay float $6,500)

|

|||

Dr. Interest expense

|

$65

|

||

Cr. Debt

|

$65

|

||

To record the change in fair value of debt for change in benchmark interest rates (e)

|

|||

Dr. Swap contract

|

$96

|

||

Cr. Interest expense

|

$96

|

||

To record the change in fair value of the swap (f)

|

|||

Dr. Interest expense

|

$10,000

|

||

Cr. Cash

|

$10,000

|

||

To record payment of interest on the debt ($100,000 @ 10%)

|

|||

Dr. Cash

|

$1,000

|

||

Cr. Interest expense

|

$1,000

|

||

To record the settlement on the swap (receive fixed $7,000, pay float $6,000)

|

|||

Dr. Debt

|

$927

|

||

Cr. Interest expense

|

$927

|

||

To record the change in fair value of debt for change in benchmark interest rates (g)

|

|||

Dr. Interest expense

|

$865

|

||

Cr. Swap contract

|

$865

|

||

To record the change in fair value of the swap (h)

|

|||

Dr. Interest expense

|

$10,000

|

||

Cr. Cash

|

$10,000

|

||

To record payment of interest on the debt ($100,000 @ 10%)

|

|||

Dr. Cash

|

$1,500

|

||

Cr. Interest expense

|

$1,500

|

||

To record the settlement on the swap (receive fixed $7,000, pay float $5,500)

|

|||

Dr. Debt

|

$1,958

|

||

Cr. Interest expense

|

$1,958

|

||

To record the change in fair value of debt for change in benchmark interest rates (i)

|

|||

Dr. Interest expense

|

$1,905

|

||

Cr. Swap contract

|

$1,905

|

||

To record the change in fair value of the swap (j)

|

|||

Dr. Interest expense

|

$10,000

|

||

Cr. Cash

|

$10,000

|

||

To record payment of interest on the debt ($100,000 @ 10%)

|

|||

Dr. Cash

|

$2,000

|

||

Cr. Interest expense

|

$2,000

|

||

To record the settlement on the swap (receive fixed $7,000, pay float $5,000)

|

|||

If the hedged item is a specific portion of an asset or liability (or of a portfolio of similar assets or a portfolio of similar liabilities), the hedged item is one of the following:

For a fair value hedge of interest rate risk in which the hedged item is for a partial term in accordance with paragraph 815-20-25-12(b)(2)(ii), an entity may measure the change in the fair value of the hedged item attributable to interest rate risk using an assumed term that begins when the first hedged cash flow begins to accrue and ends at the end of the designated hedge period. The assumed issuance of the hedged item occurs on the date that the first hedged cash flow begins to accrue. The assumed maturity of the hedged item occurs at the end of the designated hedge period. An entity may measure the change in fair value of the hedged item attributable to interest rate risk in accordance with this paragraph when the entity is designating the hedged item in a hedge of both interest rate risk and foreign exchange risk. In that hedging relationship, the change in carrying value of the hedged item attributable to foreign exchange risk shall be measured on the basis of changes in the foreign currency spot rate in accordance with paragraph 815-25-35-18. Additionally, an entity may have one or more separately designed partial-term hedging relationships outstanding at the same time for the same debt instrument (for example. 2 outstanding hedging relationships for consecutive interest cash flows in Years 1-3 and consecutive interest cash flows in Years 5-7 of a 10 year debt instrument.

Hedging relationship 1 |

Hedging relationship 2 |

|

Hedged item |

Bond A |

Bond B |

Stated maturity |

9/30/2025 |

9/30/2025 |

Optionality |

Callable starting 10/1/2024 |

Callable starting 10/1/2024 |

Designated hedged term end date |

9/30/2024 |

9/30/2025 |

Hedged item measurement include optionality? |

No |

Yes |

The adjustment of the carrying amount of a hedged asset or liability required by ASC 815-25-35-1(b) shall be accounted for in the same manner as other components of the carrying amount of that asset or liability. For example, an adjustment of the carrying amount of a hedged asset held for sale (such as inventory) would remain part of the carrying amount of that asset until the asset is sold, at which point the entire carrying amount of the hedged asset would be recognized as the cost of the item sold in determining earnings.

An adjustment of the carrying amount of a hedged interest-bearing financial instrument shall be amortized to earnings. Amortization shall begin no later than when the hedged item ceases to be adjusted for changes in its fair value attributable to the risk being hedged.

Amounts recorded in an entity’s income statement as interest costs shall be reflected in the capitalization rate under Subtopic 835-20. Those amounts could include amortization of the adjustments of the carrying amount of the hedged liability, under paragraphs 815-25-35-9 through 35-9A, if an entity elects to begin amortization of those adjustments during the period in which interest is eligible for capitalization.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Derivatives and hedging