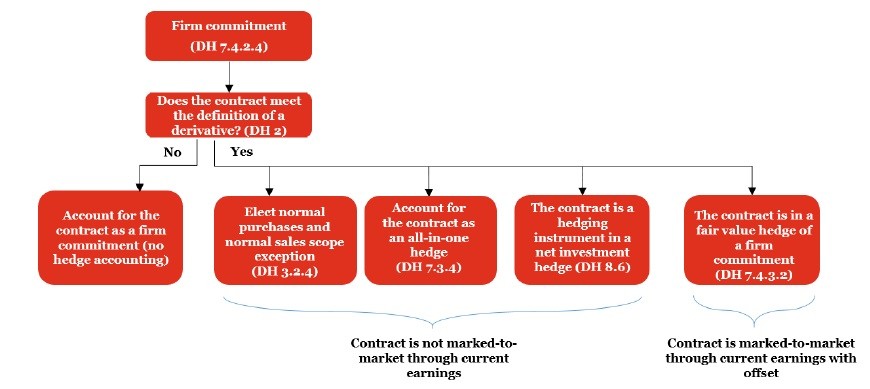

A recognized asset or liability, such as inventory, can be the hedged transaction in a fair value hedge if the specified criteria are met.

Fair value hedge of inventory

Production companies and users of commodities may need to manage exposure to the price of purchasing inputs and to changes in the value of their inventories during a holding period. A fair value hedge can be used to protect against the risk of a change in the value of physical inventory during the hedging period.

The risk identified as being hedged in a hedging transaction involving recognized nonfinancial assets, such as inventory, or a firm commitment may only be for overall changes in fair value (i.e., price risk) at the location of the inventory or the location at which the reporting entity intends to purchase or sell the inventory.

In contrast, the hedged risk identified in a cash flow hedge of a forecasted purchase or sale of inventory may also be the changes in a contractually specified component of the price or functional currency cash flows.

In practice, reporting entities often hedge the price risk associated with forecasted inventory purchases when changes in those prices cannot be passed onto their customers (i.e., through the subsequent sale of their product) because either the reporting entity has a fixed-price sales commitment or the marketplace is too competitive to allow for the pass-through of material cost increases. Reporting entities often hedge the price risk associated with forecasted inventory sales if their raw material or production costs are fixed and/or the pricing for their product in the marketplace is volatile. Because there is an opportunity to hedge the variability in either forecasted purchases or sales of inventory, many reporting entities do not find a need to enter into fair value hedges of their existing inventories. However, when a reporting entity has commodity inventories on hand, but cannot adequately forecast the timing of sales, it may be appropriate to consider entering into a fair value hedge.

Example DH 7-6 illustrates a fair value hedge of inventory using a collar.

EXAMPLE DH 7-6

Collar used to hedge inventory price risk

DH Corp uses a purchased collar (i.e., a combination of a purchased and written option) that does not constitute a written option to hedge the price risk in the inventory it holds. It structures a collar consisting of (1) a purchased put with a strike price of $80 and (2) a written call with a strike price of $120.

DH Corp documents that its hedge strategy is to protect the inventory from fair value changes outside the specified range; it does not hedge changes in the fair value from $80 to $120.

How would DH Corp account for such a hedge?

Analysis

DH Corp would adjust the inventory to reflect only the changes in value caused by a drop in the price below $80 or an increase in the price above $120 (i.e., the collar would be effective in offsetting only losses that occur when the price is below $80 or gains that occur when the price is above $120). The inventory would not be adjusted for price fluctuations that fall within the range of $80 to $120. Accordingly, changes in the fair value of the collar that reflect price fluctuations within the range of $80 to $120 would be recorded in earnings, with no offsetting adjustments made to the carrying amount of the inventory.

In this hedging relationship, DH Corp may elect to exclude the time value of the option from its assessment of effectiveness and recognize the time value of the option using an amortization approach, as discussed in

DH 7.2.1.3.

Example DH 7-7 illustrates a fair value hedge of commodity inventory using futures contracts.

EXAMPLE DH 7-7

Fair value hedge of commodity inventory using futures contracts

On October 1, 20X1, DH Mining Corp (DH Mining), located in Colorado, has 10 million pounds of copper inventory in its warehouse located near Dinosaur, Colorado, at an average cost of $3.065 per pound. DH Mining would like to protect the value of the inventory from a possible decline in copper prices until its planned sale in February 20X2. To hedge the value of the inventory, DH Mining sells 400 copper contracts (each for 25,000 pounds) through the Chicago Mercantile Exchange’s COMEX Division at $3.19 per pound for delivery in February 20X2 to coincide with its expected physical sale of its copper inventory. The spot price on October 1, 20X1 is $3.13.

How should DH Mining Corp account for the hedging relationship?

Analysis

DH Mining would designate the hedging relationship as a fair value hedge of inventory. Assuming the hedge relationship is highly effective, if prices fall during the period prior to settlement, the gain from the short position in COMEX futures contracts would be expected to substantially offset the decline in the fair value of the copper inventory. The hedge relationship may not be perfectly effective due to locational differences between the inventory and the specific warehouses designated for goods delivery by the COMEX exchange contract, none of which is near the inventory’s location. This difference creates basis risk. In addition, DH Mining would likely elect to assess effectiveness based on changes in spot prices and exclude the difference between the spot rate ($3.13) and forward rate ($3.19) from the hedging relationship. In this case, DH Mining may elect to recognize the excluded component using a mark-to-market approach or an amortization approach as discussed in

DH 7.2.1.3.

As a highly effective fair value hedge of the copper inventory, the futures contracts would be recognized on the balance sheet as assets or liabilities, and gains or losses on the futures contracts would be recognized currently in earnings, offset by the basis adjustment on the copper inventory.

View image

View image