Search within this section

Select a section below and enter your search term, or to search all click Derivatives and hedging

Favorited Content

Risk |

Hedged item |

Type of hedge |

Changes in fair value while holding inventory for consumption or sale

|

Recognized asset

Firm commitment to acquire inventory

|

Fair value hedge (DH 7.4)

|

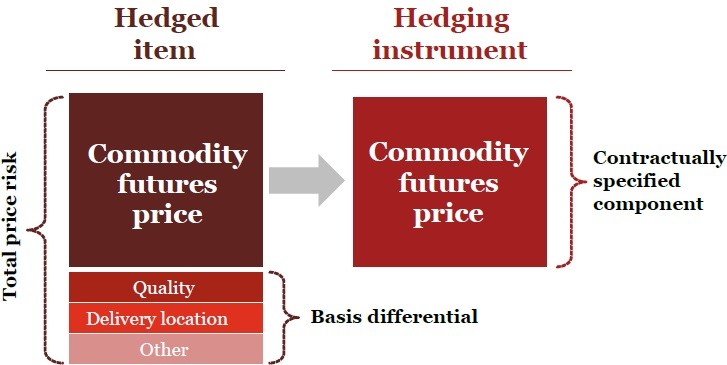

Risk associated with purchasing commodities with variable cash flows

|

Forecasted transaction (in its entirety)

Contractually specified component of a forecasted transaction |

Cash flow hedge (DH 7.3)

|

Foreign exchange risk - Risk associated with settling commodity purchases or sales in a currency other than the entity’s functional currency

|

Forecasted transaction denominated in a foreign currency

|

Foreign currency hedge (see DH 8)

|

Excerpt from ASC 815-20-25-83A

Excerpt from ASC 815-20-25-45

If a written option is designated as hedging a recognized asset or liability or an unrecognized firm commitment (if a fair value hedge) or the variability in cash flows for a recognized asset or liability or an unrecognized firm commitment (if a cash flow hedge), the combination of the hedged item and the written option provides either of the following:

For a combination of options in which the strike price and the notional amount in both the written component and the purchased option component remain constant over the life of the respective component, that combination of options would be considered a net purchased option or a zero cost collar (that is, the combination shall not be considered a net written option subject to the requirements of 815-20-25-94) provided all of the following conditions are met:

Excerpt from ASC 815-20-55-47

Date |

Henry Hub spot price |

SoCal spot price |

Henry Hub forward price— October |

SoCal forward price—October |

Difference in forward price |

January 1, 20X1 |

$7.50 |

$8.00 |

$0.50 |

||

March 31, 20X1 |

7.75 |

8.40 |

$0.65 |

||

June 30, 20X1 |

7.90 |

8.45 |

$0.55 |

||

September 30, 20X1 |

8.10 |

8.80 |

$0.70 |

||

October 1, 20X1 |

$8.10 |

$8.80 |

N/A |

N/A |

N/A |

Date |

Fair value of commodity forward* |

Change in fair value of commodity forward* |

Fair value of forward on SoCal basis* |

Change in fair value of forward on SoCal basis* |

January 1, 20X1 |

- |

- |

||

March 31, 20X1 |

$12,138 |

$12,138 |

$7,283 |

$7,283 |

June 30, 20X1 |

19,705 |

7,567 |

2,463 |

(4,820) |

September 30, 20X1 |

29,995 |

10,290 |

9,998 |

7,535 |

October 1, 20X1 |

30,000 |

5 |

10,000 |

2 |

* Amounts are discounted at 6% per year. |

March 31, 20X1 |

||

Dr. Commodity forward |

$12,138 |

|

Cr. Other comprehensive income |

$12,138 |

|

To record the change in fair value of the commodity forward |

||

Dr. Forward on SoCal basis |

$7,283 |

|

Cr. Other comprehensive income |

$7,283 |

|

To record the change in fair value of the forward on basis |

||

June 30, 20X1 |

||

Dr. Commodity forward |

$7,567 |

|

Cr. Other comprehensive income |

$7,567 |

|

To record the change in fair value of the commodity forward |

||

Dr. Other comprehensive income |

$4,820 |

|

Cr. Forward on SoCal basis |

$4,820 |

|

To record the change in fair value of the forward on basis |

||

September 30, 20X1 |

||

Dr. Commodity forward |

$10,290 |

|

Cr. Other comprehensive income |

$10,290 |

|

To record the change in fair value of the commodity forward |

||

Dr. Forward on SoCal basis |

$7,535 |

|

Cr. Other comprehensive income |

$7,535 |

|

To record the change in fair value of the forward on basis |

||

October 1, 20X1 |

||

Dr. Cash |

$40,000 |

|

Cr. Forward on SoCal basis |

$9,998 |

|

Cr. Commodity forward |

$29,995 |

|

Cr. Other comprehensive income |

$7 |

|

To record the change in fair value and settlement of the commodity and basis forwards (settlement period ignored for simplicity) |

||

October 31, 20X1 |

||

Dr. Natural gas expense |

$440,000 |

|

Cr. Accounts payable |

$440,000 |

|

To record the purchase and usage of the first 50,000 MMBtus of natural gas (50,000 MMBtus × SoCal Border spot price at first of month October 1, 20X1 price of $8.80/MMBtu) |

||

Dr. Accumulated other comprehensive income |

$40,000 |

|

Cr. Natural gas expense |

$40,000 |

|

To reclassify the gain on the swaps in AOCI to earnings |

||

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Derivatives and hedging