When determining significant influence, investors must consider both direct and indirect investments (i.e., those that may be held by its other investees) in an investee.

Example EM 2-1, Example EM 2-2, Example EM 2-3, Example EM 2-4, Example EM 2-5, and Example EM 2-6 illustrate the consideration of direct and indirect investments held by an investor.

EXAMPLE EM 2-1

Investment in each tier qualifies for equity method accounting

Company A owns a 20% voting common stock interest in Company B. Company B owns a 20% voting common stock interest in Company C. Therefore, Company A indirectly owns 4% of Company C. No contrary evidence exists to overcome the presumption that Company A has significant influence over Company B and that Company B has significant influence over Company C. All investors and investees are corporate entities.

How should Company A and Company B account for their investments?

Analysis

Company B should account for its investment in Company C pursuant to the equity method of accounting. Company A should account for its investment in Company B pursuant to the equity method of accounting. Company B would record its proportionate share of the earnings or losses of Company C in its financial statements before Company A records its proportionate share of the earnings or losses of Company B in its financial statements.

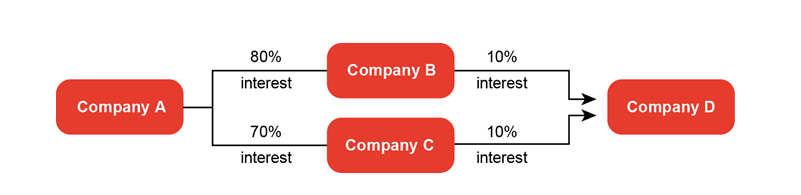

EXAMPLE EM 2-2

Investment qualifies for equity method accounting through ownership by commonly controlled investors

Company A owns an 80% voting common stock interest in Company B and a 70% voting common stock interest in Company C. Company B and Company C each own a 10% voting interest in Company D. Company A’s investments in Company B and Company C represent controlling financial interests. Therefore, Company A consolidates Company B and Company C. All investors and investees are corporate entities.

How should Company A account for its interest in Company D?

Analysis

Company A’s economic interest in Company D is 15%: an 8% interest through its controlling financial interest in Company B (80% * 10%) and a 7% interest through its controlling financial interest in Company C (70% * 10%). However, because Company A controls both Company B and Company C, Company A would not limit its indirect investment in Company D due to the partial ownership. Instead, it would be considered to have a 20% voting interest in Company D (10% through its control of Company B and 10% through its control of Company C).

Therefore, Company A’s indirect ownership interest in Company D, absent evidence to the contrary, is presumed to provide it with the ability to exercise significant influence over Company D. Therefore, if the presumption is not overcome, Company A should account for its investment in Company D under the equity method of accounting.

In their standalone financial statements, Company B and Company C would separately evaluate whether they have the ability to exercise significant influence over Company D. Given their parent (Company A) controls 20% of Company D’s voting stock, Company B and C would generally conclude in their separate financial statements that they have significant influence over Company D.

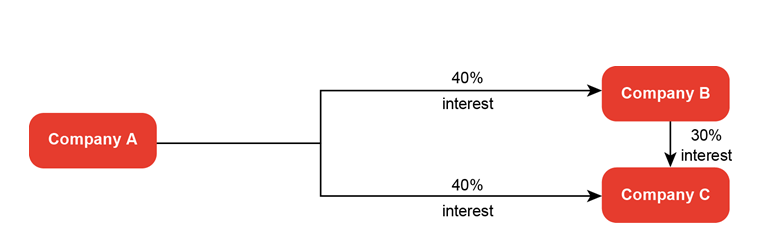

EXAMPLE EM 2-3

Equity method accounting despite majority interest through direct and indirect interests

Company A owns a 40% voting common stock interest in each of Company B and Company C. Company B also owns a 30% voting common stock interest in Company C. The remaining interests in Company B and Company C are widely held by other investors and there are no other agreements that affect the voting or management structures of Company B and Company C. All investors and investees are corporate entities. Company C is not a VIE.

How should Company A account for its direct and indirect interests in Company C?

Analysis

As there are no other agreements that affect the voting or management structures of Company B and Company C, Company A’s interest in Company B is not sufficient to direct the actions of Company B’s management. This includes how Company B should vote its 30% interest in Company C. Therefore, despite its 52% economic interest in Company C (40% direct interest, plus its 12% indirect interest through Company B (40% * 30%)), Company A would not consolidate Company C in its financial statements. Instead, Company A would account for its investment in Company C under the equity method of accounting.

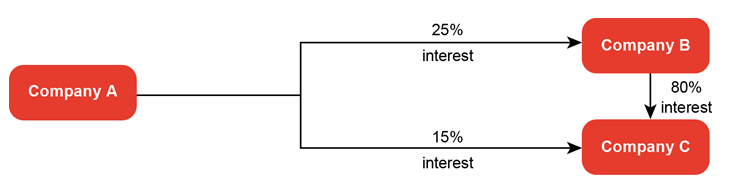

EXAMPLE EM 2-4

Investment in investee and direct investment in investee’s consolidated subsidiary

Company A owns a 25% voting common stock interest in Company B, which is accounted for under the equity method of accounting. Company A also owns a 15% voting common stock interest in Company C. Company B owns an 80% voting common stock interest in Company C, which provides Company B with a controlling financial interest; therefore, Company B consolidates Company C. All investors and investees are corporate entities.

How should Company A account for its direct interest in Company C?

Analysis

Company A has the ability to exercise significant influence over Company B. Company B has control over Company C; therefore, through its ability to exercise significant influence over Company B, Company A also has the ability to exercise significant influence over Company C, despite only having a 15% direct interest. As such, Company A should account for its direct investment in Company C under the equity method of accounting.

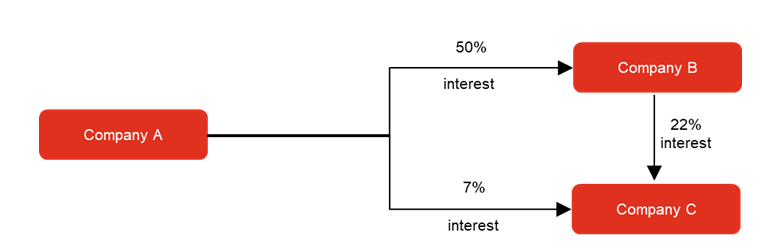

EXAMPLE EM 2-5

Equity method accounting through direct and indirect interests

Company A owns 50% of the voting common stock of Company B and applies the equity method of accounting since it has significant influence over Company B. Company B owns 22% of the voting common stock of Company C and applies the equity method of accounting since it has significant influence over Company C. Company A owns (directly) 7% of the voting common stock of Company C. All investors and investees are corporate entities.

How should Company A account for its direct investment in Company C?

Analysis

Company A’s economic interest in Company C is 18% (7% direct interest plus its 11% indirect interest (50% * 22%)). Given that Company A has the ability to exercise significant influence over the operating and financial policies of Company B (including Company B’s investment in Company C), Company A would apply the equity method of accounting to its 7% direct investment in Company C.

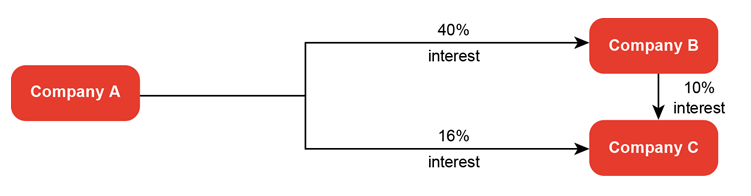

EXAMPLE EM 2-6

Investment may not qualify for equity method of accounting despite an economic interest of 20%

Company A owns a 40% voting common stock interest in Company B, which is accounted for under the equity method of accounting. Company A also owns a 16% voting common stock interest in Company C. Company B owns a 10% voting common stock interest in Company C. Individually, Company A and Company B are not able to exercise significant influence over the operating and financial policies of Company C. All investors and investees are corporate entities.

How should Company A account for its direct and indirect interests in Company C?

Analysis

Company A’s economic interest in Company C is 20% (16% direct interest, plus its 4% indirect interest (40% * 10%)). As neither Company A nor Company B have the ability to exercise significant influence over the operating and financial policies of Company C individually, Company A’s 20% economic interest in Company C is not, in and of itself, sufficient to indicate that it has the ability to exercise significant influence over Company C. Absent other factors that indicate that Company A has the ability to exercise significant influence over Company C (e.g., Company A having representation on Company C’s board), the equity method of accounting would not be appropriate for Company A’s investment in Company C.