Search within this section

Select a section below and enter your search term, or to search all click Equity method of accounting

Favorited Content

An investor shall record its proportionate share of the investee’s equity adjustments for other comprehensive income (unrealized gains and losses on available-for-sale securities; foreign currency items; and gains and losses, prior service costs or credits, and transition assets or obligations associated with pension and other postretirement benefits to the extent not yet recognized as components of net periodic benefit cost) as increases or decreases to the investment account with corresponding adjustments in equity. See paragraph 323-10-35-37 for related guidance to be applied upon discontinuation of the equity method.

For the purposes of applying the equity method of accounting to an investee subject to guidance in an industry-specific Topic, an entity shall retain the industry-specific guidance applied by that investee.

Paragraphs 323-10-25-4 through 25-6 provide guidance on accounting for share-based payment awards granted by an investor to employees or nonemployees of an equity method investee that provide goods or services to the investee that are used or consumed in the investee’s operations when no proportionate funding by the other investors occurs and the investor does not receive any increase in the investor's relative ownership percentage of the investee. That guidance assumes that the investor's grant of share-based payment awards to employees or nonemployees of the equity method investee was not agreed to in connection with the investor's acquisition of an interest in the investee. That guidance applies to share-based payment awards granted to employees or nonemployees of an investee by an investor based on that investor's stock (that is, stock of the investor or other equity instruments indexed to, and potentially settled in, stock of the investor).

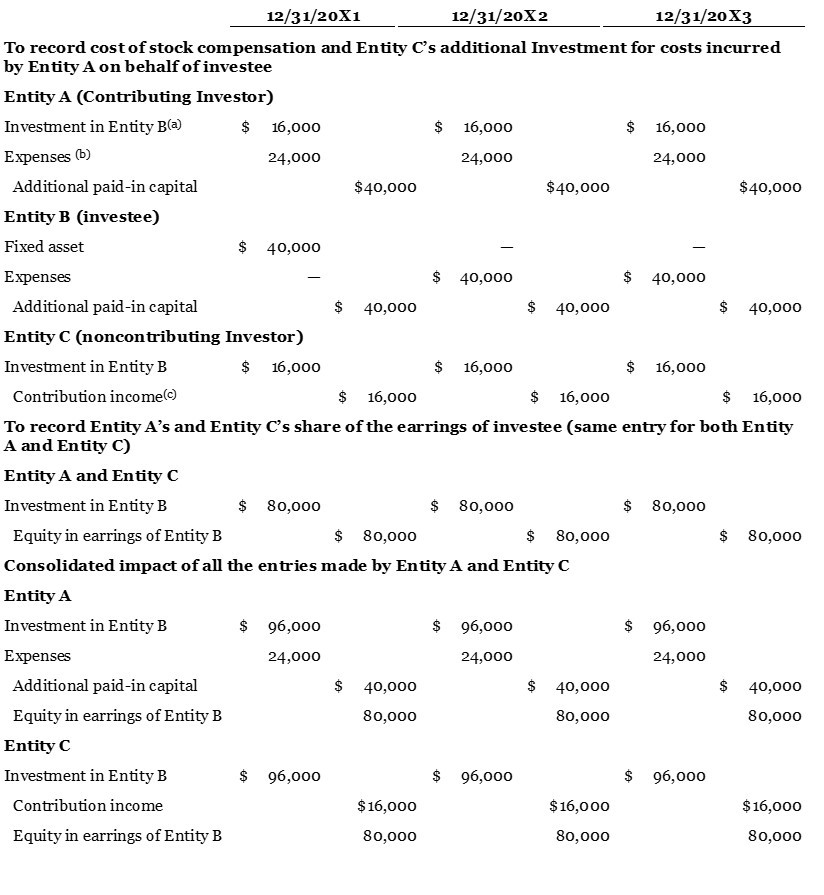

In the circumstances described in paragraph 323-10-25-3, a contributing investor shall expense the cost of share-based compensation granted to employees and nonemployees of an equity method investee as incurred (that is, in the same period the costs are recognized by the investee) to the extent that the investor’s claim on the investee’s book value has not been increased.

In the circumstances described in paragraph 323-10-25-3, other equity method investors in an investee (that is, noncontributing investors) shall recognize income equal to the amount that their interest in the investee’s net book value has increased (that is, their percentage share of the contributed capital recognized by the investee) as a result of the disproportionate funding of the compensation costs. Further, those other equity method investors shall recognize their percentage share of earnings or losses in the investee (inclusive of any expense recognized by the investee for the stock-based compensation funded on its behalf).

This Example illustrates the guidance in paragraphs 323-10-25-3 and 323-10-30-3 for share-based compensation by an investor granted to employees of an equity method investee. This Example is equally applicable to share-based awards granted by an investor to nonemployees that provide goods or services to an equity method investee that are used or consumed in the investee’s operations.

Entity A owns a 40 percent interest in Entity B and accounts for its investment under the equity method. On January 1, 20X1, Entity A grants 10,000 stock options (in the stock of Entity A) to employees of Entity B. The stock options cliff-vest in three years. If an employee of Entity B fails to vest in a stock option, the option is returned to Entity A (that is, Entity B does not retain the underlying stock). The owners of the remaining 60 percent interest in Entity B have not shared in the funding of the stock options granted to employees of Entity B on any basis and Entity A was not obligated to grant the stock options under any preexisting agreement with Entity B or the other investors. Entity B will capitalize the stock-based compensation costs recognized over the first year of the three-year vesting period as part of the cost of an internally constructed fixed asset (the internally constructed fixed asset will be completed on December 31, 20X1).

Before granting the stock options, Entity A’s investment balance is $800,000, and the book value of Entity B’s net assets equals $2,000,000. Entity B will not begin depreciating the internally constructed fixed asset until it is complete and ready for its intended use and, therefore, no related depreciation expense (or compensation expense relating to the stock options) will be recognized between January 1, 20X1, and December 31, 20X1. For the years ending December 31, 20X2, and December 31, 20X3, Entity B will recognize depreciation expense (on the internally constructed fixed asset) and compensation expense (for the cost of the stock options relating to Years 2 and 3 of the vesting period). After recognizing those expenses, Entity B has net income of $200,000 for the fiscal years ending December 31, 20X1, December 31, 20X2, and December 31, 20X3.

Entity C also owns a 40 percent interest in Entity B. On January 1, 20X1, before granting the stock options, Entity C’s investment balance is $800,000.

Assume that the fair value of the stock options granted by Entity A to employees of Entity B is $120,000 on January 1, 20X1. Under Topic 718, the fair value of share-based compensation should be measured at the grant date. This Example assumes that the stock options issued are classified as equity and ignores the effect of forfeitures.

Entity A would make the following journal entries.

View image

View image

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Equity method of accounting