In addition to joint control, there are other characteristics that must be met for an entity to meet the definition of a joint venture, as described in

ASC 323-10-20. That is, joint control alone is not sufficient to obtain joint venture accounting. At the 2014 AICPA National Conference on Current SEC and PCAOB Developments, the SEC staff stated that each of the characteristics in the definition of a joint venture should be met for an entity to be a joint venture, including that the purpose of the entity is consistent with that of a joint venture.

ASC 845-10-S99-2 states that the existence of joint control is not the only defining characteristic when determining whether an entity is a joint venture, rather, the other characteristics of a joint venture also need to be present. While the other characteristics might appear to be broad in nature and lacking specific guidance on how an entity would meet them (versus, for example, the joint control characteristic), an entity should exercise reasonable judgment in assessing whether it has met the additional characteristics. In making this assessment, the factors to consider include the purpose, nature, and operations of the entity.

For example, if the substance of a transaction is primarily to combine two or more existing operating businesses, which are either separate subsidiaries or divisions of a larger company, in an effort to generate synergies such as economies of scale or cost reductions and/or to generate future growth opportunities, such a transaction may be considered a merger that should be accounted for as a business combination under

ASC 805 rather than as a joint venture. In this fact pattern, determining whether the purpose of the transaction is consistent with the definition of a joint venture as described in

ASC 323 requires significant judgment.

Example EM 6-3, Example EM 6-4, Example EM 6-5, and Example EM 6-6 illustrate some of the accounting considerations when evaluating whether an entity meets the definition of a joint venture for accounting purposes.

EXAMPLE EM 6-3

Determining whether a joint venture is formed when each investor contributes its entire operations to a new entity

Company A, a holding company, owns Company B, which has a fair value of $500 million, and represents all of Company A’s operations. Company C, a holding company, owns Company D, which has a fair value of $400 million, and represents all of Company C’s operations. Company A and Company C agree to combine their operating businesses in a newly established entity, Newco. Company A contributes Company B in exchange for 55% equity and joint control of Newco. Company C contributes Company D in exchange for 45% equity and joint control of Newco. Company A and Company C each have two members on the four member board of directors and unanimous approval from all board members is required for all decisions related to Newco. Other than joint control, none of the other characteristics of a joint venture as described in

ASC 323 exist.

Does this arrangement meet the definition of a joint venture for accounting purposes?

Analysis

No. Newco does not meet the definition of a joint venture. Although the investors appear to have joint control, both investors have contributed their entire operations, and therefore would likely not meet the aspect of the definition that describes the purpose of a joint venture. This transaction was likely for the purpose of achieving economies of scale or cost reductions as opposed to the purpose of sharing risks and rewards in developing a new market, product, or technology; combining complementary technological knowledge; or pooling resources in developing production or other facilities.

EXAMPLE EM 6-4

Determining whether a joint venture is formed when one investor contributes a business and the other investor contributes cash to a new entity

Company A, a holding company, owns various businesses including Company B, which has a fair value of $500 million. Company A and Company C agree to form a joint venture, Newco, as they have plans for new product offerings and expansion into new markets. Company A contributes Company B in exchange for 50% equity and joint control of Newco. Company C contributes $500 million cash in exchange for 50% equity and joint control of Newco. The cash will remain in Newco to be used for ongoing operating expenses, developing new products, and developing new production facilities. Company A and Company C each have two members on the four member board of directors and unanimous approval from all board members is required for all decisions related to Newco.

Does this arrangement meet the definition of a joint venture for accounting purposes?

Analysis

Yes. Newco meets the definition of a joint venture for accounting purposes. Company A and Company C have each made contributions in exchange for joint control of the new entity. The purpose for the entity is consistent with that of a joint venture as the venture will use the cash invested by Company C to gain access to new markets and to develop new products.

EXAMPLE EM 6-5

Whether a joint venture is formed when one investor sells 50% of an existing operating subsidiary

Company A, a holding company, owns Company B, which has a fair value of $500 million, and represents all of Company A’s operations. Company A has decided to cash out a portion of its existing business. To facilitate the transaction, Company A and Company C agree to form a new company, Newco, which the two investors will jointly own and jointly control. Company A contributes Company B in exchange for 100% of the equity of Newco. Company C pays $250 million cash to Company A in exchange for 50% of its equity in Newco. Company A and Company C each have two members on the four member board of directors and unanimous approval from all board members is required for all decisions related to Newco.

Does this arrangement meet the definition of a joint venture for accounting purposes?

Analysis

No. While the investors have joint control over Newco, the substance of the transaction is that Company A has sold 50% of its business in exchange for cash. As the purpose of the transaction does not meet any of the other characteristics as described in ASC 323-10-20, this arrangement does not meet the definition of a joint venture for accounting purposes.

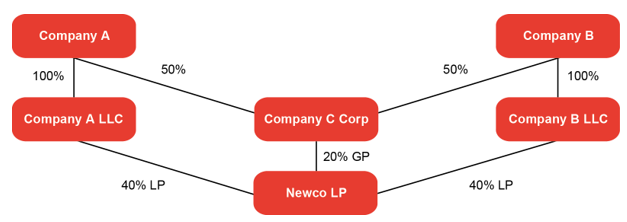

EXAMPLE EM 6-6

A joint venture structured in the form of a partnership

Company A and Company B form a new venture, Newco Partnership, a limited partnership. The general partner (GP) of Newco Partnership is Company C Corporation, a newly formed entity jointly owned and controlled by Company A and Company B. Company A owns 100% of Company A LLC, which has a 40% limited partnership interest in Newco Partnership. Company B owns 100% of Company B LLC, which has a 40% limited partnership interest in Newco Partnership. The GP owns the remaining 20% general partnership interest in Newco Partnership. The GP has the unilateral right to make all the decisions of Newco Partnership and the LPs do not have any participating rights or kick-out rights. Company A and Company B are not related parties.

Does Newco Partnership meet the definition of a joint venture?

Analysis

Yes. Assuming all of the other characteristics in ASC 323-10-20 are met, Newco Partnership would meet the definition of an accounting joint venture since Company A and Company B have joint control over the GP, which controls Newco Partnership. In this case, the substance of the arrangement is that the two companies have joint control over the joint venture.