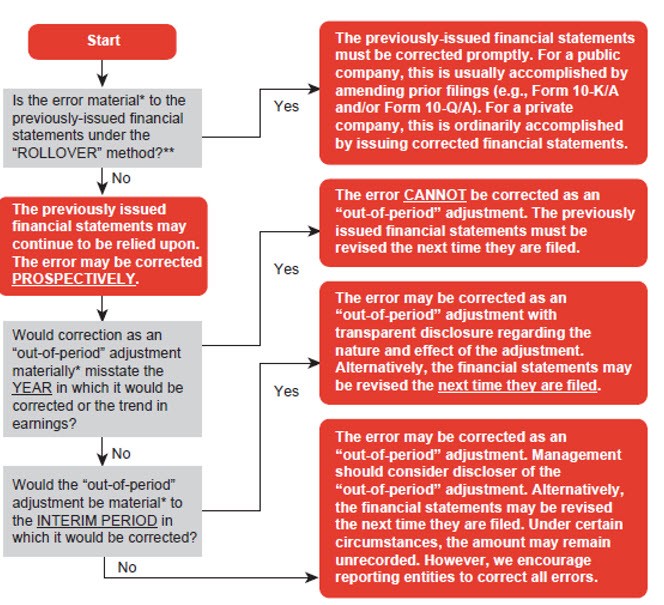

If the previously issued financial statements are not materially misstated, then the error may be corrected prospectively. While

ASC 250 only contemplates reporting the correction of an error by restating the previously issued financial statements, many identified errors do not result in a material misstatement to previously issued financial statements. In that case, the error may be corrected in one of two ways:

- Recording an out-of-period adjustment, with appropriate disclosure, in the current period, if such correction does not create a material misstatement in the current year

- Revising the prior period financial statements the next time they are presented

When the correcting amounts are material to current operations or trends, reporting entities should revise the previously issued financial statements the next time they are issued.

A revision disclosure is similar to a restatement disclosure. However, the financial statement columns should not be labeled “as restated.” Further, revising prior year financial statements would not require previously issued auditor reports to be corrected as users can continue to rely on those previously issued financial statements. The reporting entity should consult with its counsel to determine whether it should provide disclosure of prospective corrections that are expected to be made in future financial statements. It may not be necessary to file a

Form 8-K under Item 4.02 because the previously issued financial statements are not materially misstated (i.e., they can continue to be relied upon). However, there may be other situations in which separate disclosure would be appropriate. For example, if securities are to be offered based on the uncorrected financial statements, the prospectus/offering materials may need to include additional disclosure (including quantification) of the impending correction.

Example FSP 30-2 illustrates the evaluation of an identified error.

EXAMPLE FSP 30-2

Example of the error evaluation process

FSP Corp is a calendar year-end SEC registrant. In early April 20X5, FSP Corp identified a long-term incentive compensation obligation for one of its salespeople which it had inadvertently neglected to record since 20X1. If FSP Corp had properly accounted for the bonus, it would have recorded an additional $30 of compensation expense in each of the years 20X1 through 20X4.

- FSP Corp’s reported income in each of the years 20X1 through 20X4 was $1,000.

- FSP Corp projects its 20X5 income will be $1,000.

Note: Income tax effects are ignored for purposes of this example. Additionally, this example assumes that there are no other errors affecting any of the years. If there were additional errors (whether unadjusted or recorded as “out-of-period” adjustments), those errors would also need to be considered in the materiality analysis.

What analysis should FSP Corp perform to consider if the errors are material?

Analysis

Quantifying the errors in the previously issued financial statements

FSP Corp has quantified the errors under both the “rollover” and the “iron curtain” methods as follows:

Year |

Reported income |

Rollover method |

Iron curtain method |

|

|

|

|

20X5 |

$1,000 (Projected) |

N/A |

$120 (12%) |

Evaluating whether the affected financial statements are materially misstated

FSP Corp should consider whether the errors quantified under the “rollover” method (i.e., $30 or 3% of income per year) are material to the financial statements for any of the years 20X1 through 20X4. In making this analysis, FSP Corp should consider all relevant qualitative and quantitative factors.

Note: The above analysis focuses on the effects of the errors on the income statement. However, the analysis must also consider the impact of the error on the full financial statements, including disclosures (e.g., segment reporting).

Determining how to correct the errors

If FSP Corp determines that any of the years 20X1 through 20X4 are materially misstated when the errors are evaluated under the “rollover” method, then those years must be promptly corrected (as discussed in

FSP 30.7.1).

If FSP Corp determines that none of the years 20X1 through 20X4 (or quarters for 20X4) are materially misstated when the errors are quantified under the “rollover” method, then the errors can be corrected prospectively in current or future filings (as discussed in FSP 30.7.2). Depending on the circumstances, prospective correction may be accomplished in one of two ways:

- FSP Corp may correct the errors as an “out-of-period” adjustment in its first quarter 20X5 interim financial statements if the correction would not result in a material misstatement of the estimated fiscal year 20X5 earnings ($1,000) or to the trend in earnings. This is true even if the “out-of-period” adjustment is material to the first quarter 20X5 interim financial statements. If the “out-of-period” adjustment is material to the first quarter 20X5 interim financial statements (but not material with respect to the estimated income for the full fiscal year 20X5 or to the trend of earnings), then the correction may still be recorded in the first quarter, but should be separately disclosed (in accordance with ASC 250-10-45-27).

- If FSP Corp cannot correct the errors as an “out-of-period” adjustment without causing a material misstatement of the estimated fiscal year 20X5 earnings ($1,000) or to the trend in earnings, then the errors must be corrected by revising the previously issued financial statements the next time they are filed (e.g., for comparative purposes). For instance, the quarterly financial statements for the first quarter of 20X4 and the December 31, 20X4 balance sheet presented in FSP Corp’s March 31, 20X5 Form 10-Q should be revised to correct the error. The revised financial statements should include transparent disclosure regarding the nature and amount of each error being corrected. The disclosure should provide insight into how the errors affect all relevant periods (including those that will be revised in subsequent filings).

View image

View image