Search within this section

Select a section below and enter your search term, or to search all click Financial statement presentation

Favorited Content

Income available to parent company common stockholders (the “numerator”) |

Weighted average number of common shares outstanding (the “denominator”) |

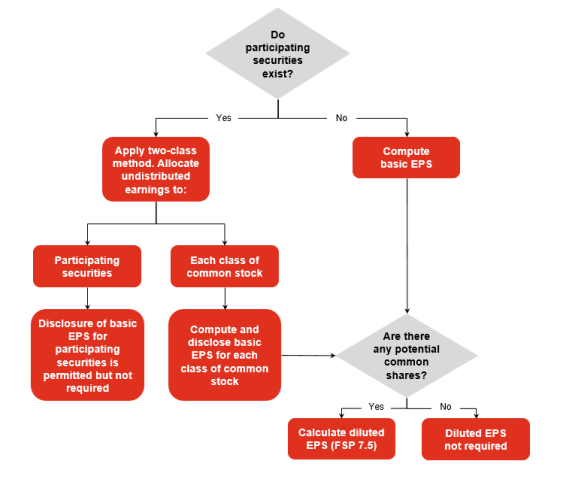

View image

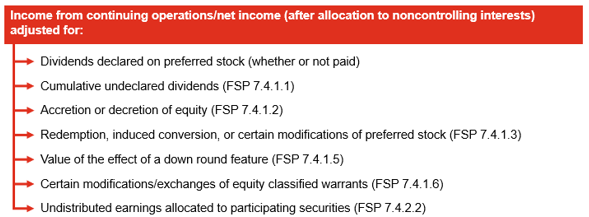

View image

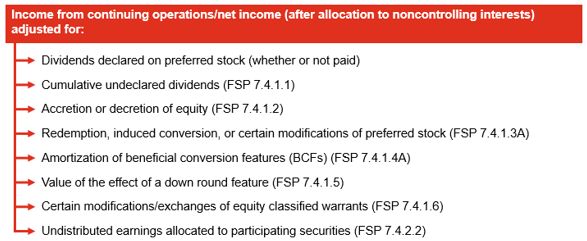

View image

View image

Fair value of consideration transferred

|

less

|

Carrying value, net of issuance costs

|

equals

|

Adjustment to numerator

|

Fair value of consideration transferred |

$1,200,000 |

|

Less: Carrying value of preferred stock |

(1,000,000) |

|

Reduction in numerator related to “deemed dividend” |

$200,000 |

|

Fair value of consideration transferred |

minus |

original BCF |

less |

Carrying value, net of issuance costs |

equals |

Adjustment to numerator |

Fair value of consideration transferred |

$1,200,000 |

Less: BCF (at original intrinsic value) |

(200,000) |

Less: Carrying value of preferred stock |

(900,000) 1 |

Reduction in numerator related to “deemed dividend” |

$100,000 |

Definition from ASC Master Glossary

Down round feature: A feature in a financial instrument that reduces the strike price of an issued financial instrument if the issuer sells shares of its stock for an amount less than the currently stated strike price of the issued financial instrument or issues an equity-linked financial instrument with a strike price below the currently stated strike price of the issued financial instrument.

Definition from ASC Master Glossary

Definition from ASC 260-10-20

Participating Security: A security that may participate in undistributed earnings with common stock, whether that participation is conditioned upon the occurrence of a specified event or not. The form of such participation does not have to be a dividend—that is, any form of participation in undistributed earnings would constitute participation by that security, regardless of whether the payment to the security holder was referred to as a dividend.

Excerpt from ASC 260-10-45-60

The two-class method is an earnings allocation formula that treats a participating security as having rights to earnings that otherwise would have been available to common shareholders…

Net income |

$50,000,000 |

|||

Less dividends declared: |

||||

Common stock |

($20,000,000) 1 |

|||

Participating preferred stock |

(12,000,000) 2 |

(32,000,000) |

||

Undistributed earnings

|

$18,000,000 |

|||

Net income |

$50,000,000 |

|

Less: Earnings attributable to preferred stockholders |

(18,750,000) 1 |

|

Income available to common stockholders |

$31,250,000 |

|

Divided by common shares outstanding |

10,000,000 |

|

Basic EPS |

$3.13 |

|

Common stock |

Restricted stock |

Total |

|||||

Distributed earnings |

$9,500,000 |

$1,000,000 |

$10,500,000 |

||||

Excess distributions |

(500,000) |

— |

(500,000) |

||||

Net income |

$9,000,000 |

$1,000,000 |

$10,000,000 |

||||

In a forward contract to issue an entity's own equity shares, a provision that reduces the contract price per share when dividends are declared on the issuing entity's common stock represents a participation right. Such a provision constitutes a participation right because it results in a noncontingent transfer of value to the holder of the forward contract for dividends declared during the forward contract period. That is, the forward contract holder has a right to participate in the undistributed earnings of the issuing entity because a dividend declaration by the issuing entity results in a transfer of value to the holder of the forward contract through a reduction in the forward purchase price per share. Because that value transfer is not contingent - as opposed to a similar reduction in the exercise price of an option or warrant - the forward contract is a participating security, regardless of whether, during the period the contract is outstanding, a dividend is declared.

Definition from ASC 260-10-20

Weighted-average number of common shares outstanding: The number of shares determined by relating the portion of time within a reporting period that common shares have been outstanding to the total time in that period. In computing diluted EPS, equivalent common shares are considered for all dilutive potential common shares.

Type of security |

Impact on denominator of basic EPS |

Section |

Contingent shares

|

Not included in the basic EPS denominator until the contingency has been resolved

|

|

Prepaid variable share forward sale contracts

|

Variable shares in excess of the minimum number to be issued under the arrangement are not included in the basic EPS denominator.

|

|

Restricted stock-based compensation awards

|

Not included in the basic EPS denominator until vested, unless vesting occurs upon retirement and the employee is retirement eligible

|

|

Mandatorily redeemable common stock

|

Not included in the basic EPS denominator if the stock is liability classified under ASC 480

|

|

Forward purchase contracts for a fixed number of shares

|

Shares subject to the forward purchase contract are not included in the basic EPS denominator if the forward purchase contract requires physical settlement of a fixed number of shares in exchange for cash.

|

|

Share lending arrangements

|

Not included in the basic EPS denominator unless default of the share lending arrangement occurs

|

|

Employee stock purchase plans

|

Typically not included in the basic EPS denominator until the shares are actually purchased

|

Excerpt from August 2008 proposed amendment to FAS 128

The Board agreed that including an instrument in basic EPS that does not give the holder the present ability to become a common shareholder provides an inaccurate depiction that, in all cases, the holder has the same claim to current-period earnings as a common shareholder even if the holder has stated participation rights that differ from common shareholders. Accordingly, the Board decided that the holder of (a) an instrument that is currently exercisable for little or no cost to the holder or (b) a share that is currently issuable for little or no cost to the holder has the present ability to become a common shareholder and, therefore, has the present right to share in current-period earnings with common shareholders.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Financial statement presentation