Generally, a put or call option is considered clearly and closely related to its debt host unless it is leveraged (i.e., it creates more interest rate and/or credit risk than is inherent in the host instrument). For example, debt issued at par value that is puttable at two times the par value upon the occurrence of a specified event may have an embedded component that is not clearly and closely related to its debt host instrument.

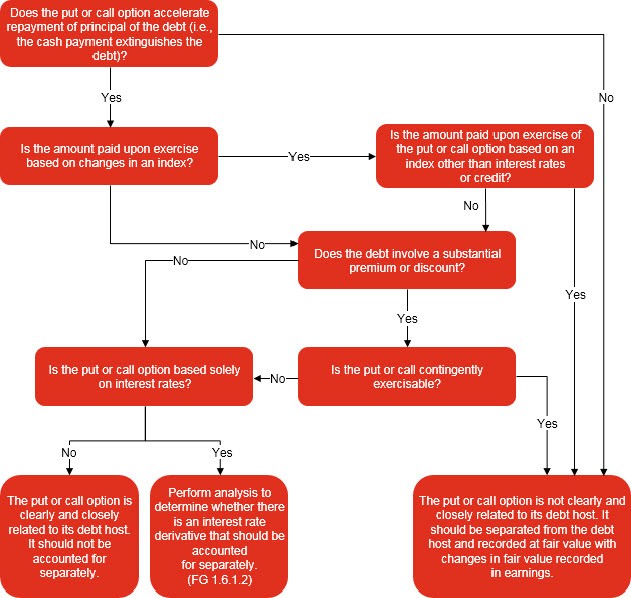

Figure FG 1-1 illustrates the analysis to determine whether a put or call option is clearly and closely related to its debt host instrument. If the put or call option is not considered clearly and closely related to its host debt instrument based on this analysis, it should be separately accounted for as a derivative under the guidance in

ASC 815.

Figure FG 1-1

Determining whether an embedded put or call option is clearly and closely related to its host debt instrument

See Example FG 1-1 for an illustration of the different analyses for a put option and a term extending option. The example is written from the perspective of an investor; however, an issuer would follow the same guidance.

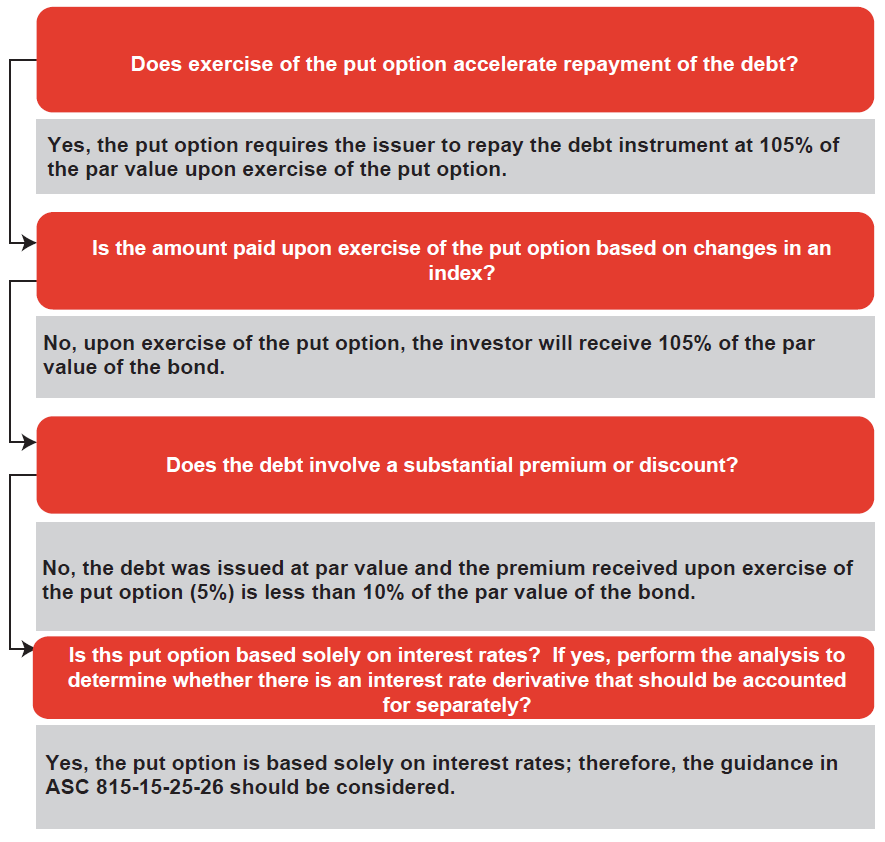

EXAMPLE FG 1-1

Analysis of put options and options to extend debt

Investor Corp purchases two bonds: Bond A and Bond B. Both bonds are issued by the same issuer at par and have a coupon rate of 6%.

Bond A has a stated maturity of ten years, but the investor can put it back to the issuer at par after three years.

Bond B has a stated maturity of three years, but after three years the investor can extend the maturity to ten years (i.e., seven more years) at the same initial interest rate (i.e., neither the interest rate, nor the credit spread, are reset to the then-current market interest rate).

Assume the following scenarios exist at the end of three years:

Scenario 1: The issuer’s interest rate for seven-year debt is 8%. The investor will put Bond A back to the issuer and reinvest the par amount of the bond at 8%. The investor will not extend the maturity of Bond B and instead will reinvest the principal at 8%.

Scenario 2: The issuer’s interest rate for seven-year debt is 4%. The investor will not put Bond A back to the issuer and instead will continue to receive 6% for the next seven years. The investor will extend the term of Bond B and continue to receive 6% for the next seven years.

How should the embedded derivatives in Bond A and Bond B be analyzed?

Analysis

Although in both scenarios the issuer and Investor Corp are in the same economic position with respect to Bond A and Bond B,

ASC 815 may require that they be treated differently.

The put option in Bond A would generally not have to be separated because calls and puts in debt hosts are generally clearly and closely related to the host contract, unless they meet the conditions in

ASC 815-15-25-42 or

ASC 815-15-25-26.

On the other hand,

ASC 815-15-25-44 indicates that the term-extending option in Bond B may not be clearly and closely related to its debt host because its interest rate and credit spread are not reset to the then-current market interest rate when the option is exercised. However, only term-extending options in debt hosts that cause an investor to potentially not recover substantially all of its recorded investment (i.e., lose principal) would be considered not clearly and closely related. Since the term extension option is within the control of the investors, they could not be forced into a term extension in which (on a present value basis) they would not be recovering substantially all of their initial net investment; therefore, the term-extending option embedded in Bond B is clearly and closely related.

If the issuer controls the term extension option, it is possible that the investor could be forced into a situation in which the investor does not recover substantially all of their initial net investment (on a present value basis), which would indicate that the term extension option is not clearly and closely related to the host contract. However, consideration should be given to whether the term extension option meets the definition of a derivative or if it would qualify for a scope exception in

ASC 815 to determine if it should be bifurcated from the host contract. For host contracts other than debt hosts,

ASC 815-15-25-45 requires an analysis to determine whether term extension options should be separated under

ASC 815-15-25-1(a).

Notwithstanding the guidance in

ASC 815-15-25-44 and

ASC 815-15-25-45, many term-extending options will not meet the definition of derivatives because they cannot be net settled. Additionally, from the perspective of the issuer of the loan agreement, a term-extending option when only the issuer/borrower has the right to extend the agreement would be considered a loan commitment and meet the scope exception for loan commitments, as described in

ASC 815-10-15-69 through

ASC 815-10-15-71. Therefore, many term-extending options will not have to be separated from the host instrument, even though they may not be clearly and closely related to their host contracts because a freestanding instrument with the same terms would not meet the definition of a derivative or would be eligible for a scope exception.

Determine whether the put or call option accelerates repayment of principal of the debt

The reporting entity should first determine whether exercise of the put or call option accelerates the repayment of principal of the debt.

ASC 815-15-25-41 provides guidance on put and call options that do not accelerate the repayment of the debt.

ASC 815-15-25-41

Call (put) options that do not accelerate the repayment of principal on a debt instrument but instead require a cash settlement that is equal to the price of the option at the date of exercise would not be considered to be clearly and closely related to the debt instrument in which it is embedded.

If exercise of a put or call option accelerates the repayment of the debt, further analysis is required to determine whether the put or call option is clearly and closely related to its debt host.

Determine the nature of the settlement amount paid upon exercise of put or call option

The reporting entity should determine if the amount paid upon exercise of a put or call option is based on changes in an index rather than simply being the repayment of principal at par or at a fixed premium or discount. For example, a put option that entitles the holder to receive an amount determined by the change in the S&P 500 index (i.e., par value of the debt multiplied by the change in the S&P 500 index over the period the debt is outstanding) is based on changes in an equity index. On the other hand, debt callable at a fixed price of 101% is not based on changes in an index. Debt callable at a price of 108% at the end of year 1, 106% at the end of year 2, and 104% at the end of year 3 is also not based on changes in an index because the call premium changes simply due to the passage of time.

If the amount paid upon exercise of a put or call option is based on changes in an index, then the reporting entity should determine whether the index is an interest rate index or credit risk (specifically, the issuer’s credit). If the index is

not an interest rate index or credit risk, the put or call option is not clearly and closely related to the debt host instrument and should be separately accounted for as a derivative under the guidance in

ASC 815.

If the amount paid upon exercise of the put or call option is (1) not based on changes in an index, or (2) based on changes in an interest rate or related to the issuer’s credit, further analysis is required to determine whether the put or call option is clearly and closely related.

Question FG 1-4

Is an embedded put or call option that if exercised, the borrower will pay the fair value of the debt upon exercise considered clearly and closely related to its host?

PwC response

Maybe. There are circumstances when a fair value put or call option may not be considered clearly and closely related to its debt host. For example, if a debt instrument is callable by the borrower at fair value, a lender may receive substantially less than their initial recorded investment. On the other hand, if the option is a lender-held put option, while the investor would never be forced to receive substantially less than their initial recorded investment, the put option would need to be further evaluated to determine if it is clearly and closely related to the host. However, the option generally would not have a material value because its strike price is equal to the underlying’s fair value.

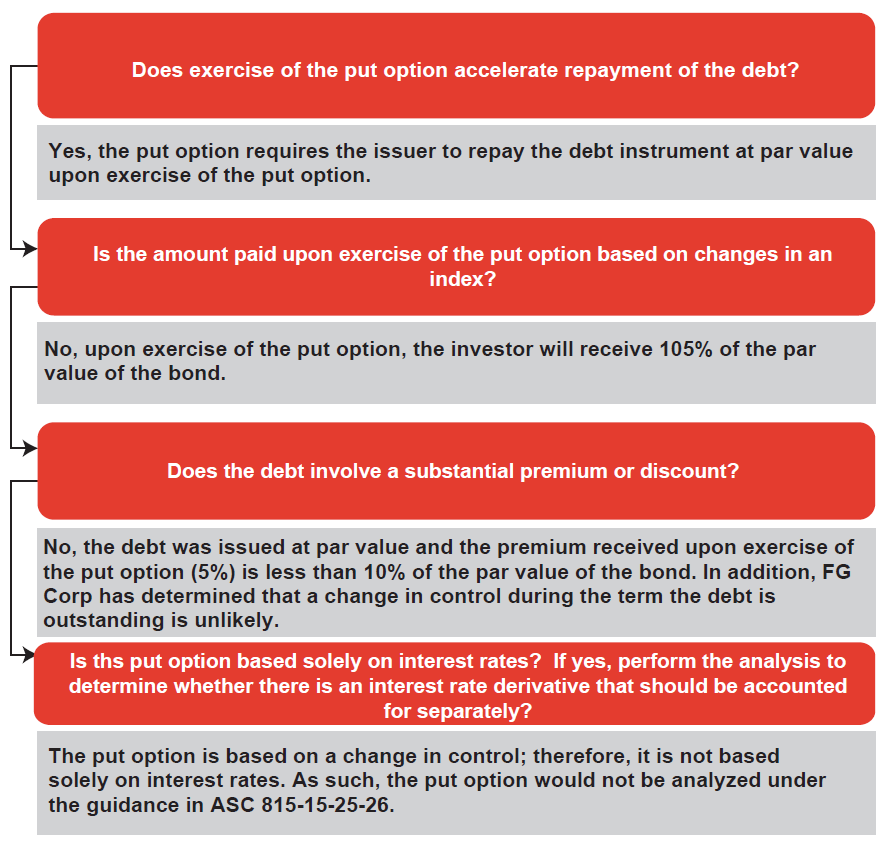

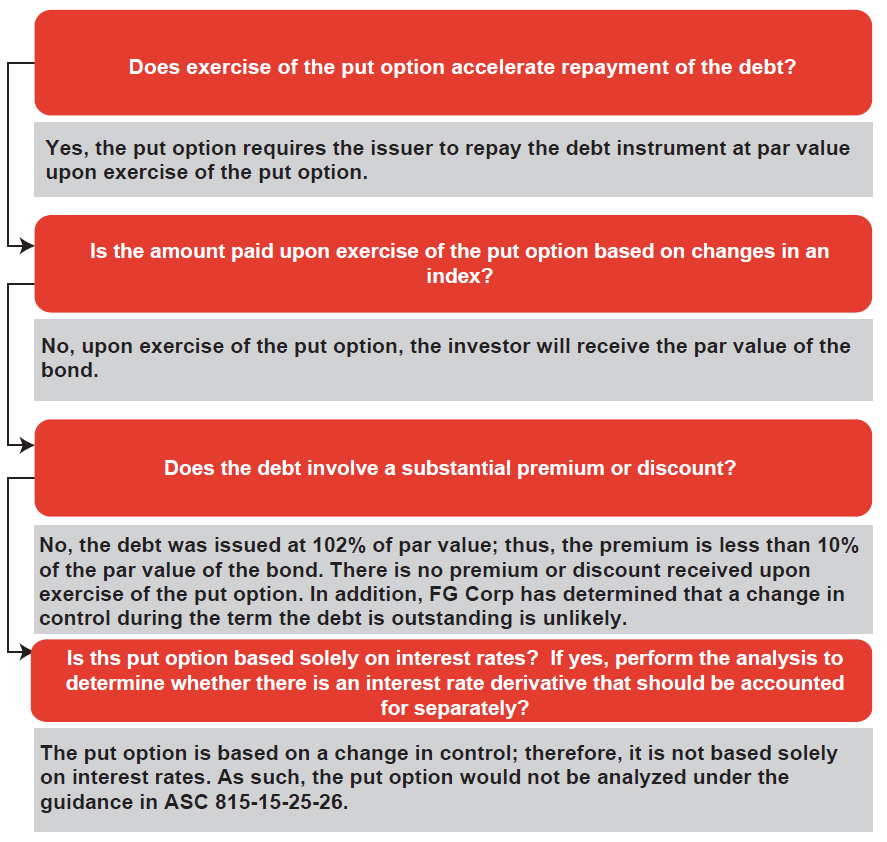

Determine whether the debt instrument involves a substantial discount or premium

Practice generally considers a discount or premium equal to or greater than 10% of the par value of the host debt instrument to be substantial. Similarly, a spread between the debt’s issuance price and the price at which the put or call option can be exercised that is equal to or greater than 10% is also generally considered substantial. However, a 10% discount or premium is not a bright-line; all relevant facts and circumstances should be considered to determine whether the discount or premium is substantial. For example, if a contingent put or call option is highly likely of becoming exercisable in a short period of time after issuance, a discount or premium of less than 10% could be considered substantial. A put or call option that requires a debt instrument to be repaid at its accreted value is generally not considered to involve a substantial discount or premium.

If the put or call involves a substantial premium or discount, it should be evaluated to determine whether it is contingently exercisable. If it does not involve a substantial premium or discount, it should be further evaluated to determine whether it contains an embedded interest rate derivative that should be separated. See

FG 1.6.1.2 for information on how to determine whether a debt host contract contains an embedded interest rate derivative.

Determine whether the put or call option is contingently exercisable

The reporting entity should then determine whether the put or call option is contingently exercisable. A debt instrument that an issuer can call upon a commodity price level reaching a specified price, bonds puttable if interest rates reach a specified level, and bonds puttable upon a change in control are examples of instruments with put and call options that are contingently exercisable.

If the put or call is contingently exercisable and meets the other requirements shown in Figure

DH 4-4, the put or call is not clearly and closely related to its host debt instrument. If it is not contingently exercisable or is not otherwise required to be bifurcated under

ASC 815-15-25-41 and

ASC 815-15-25-42, it should be further evaluated to determine whether it contains an embedded interest rate derivative that should be separated.