Search within this section

Select a section below and enter your search term, or to search all click Financing transactions

Favorited Content

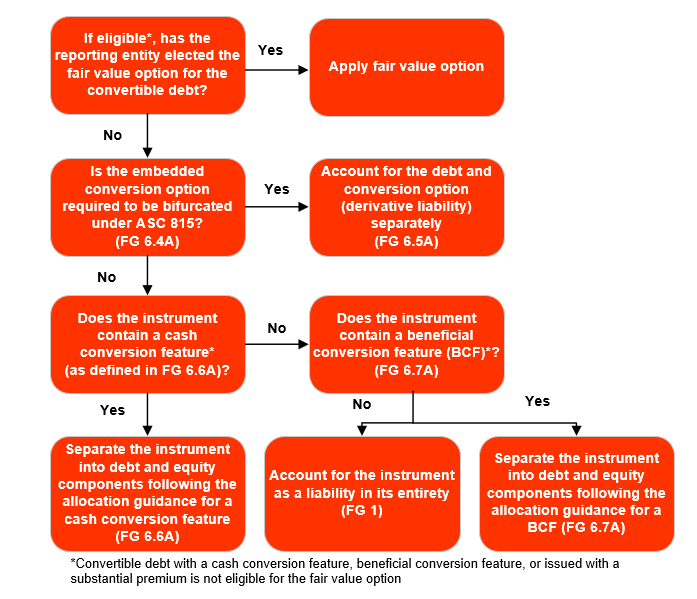

Method

| Description of methodology

|

Single instrument

(FG 1) | |

Derivative separation

(FG 6.5A) | • Determine the fair value of the embedded conversion option

• Record the conversion option at fair value and reduce the convertible debt liability by an equivalent amount

• Carry the conversion option as a liability at fair value with changes in fair value recorded in the income statement

• Amortize any discount or premium in the same manner as nonconvertible debt (see FG 1.2.3)

• Account for derecognition as discussed in FG 6.5.1A

|

Cash conversion option separation

(FG 6.6A) | • Determine the fair value of the debt liability by determining the fair value of an equivalent debt instrument without a conversion option

• The difference between the proceeds received and the debt liability is recorded in additional paid-in capital

• No subsequent remeasurement of the amount recorded in equity

• Amortize the discount on the debt liability to interest expense over the expected life of the debt instrument

• Account for derecognition as discussed in FG 6.6.5A

|

Beneficial conversion feature (BCF) separation

(FG 6.7A) | • Determine the BCF amount based on the in-the-money amount of the conversion option

• Record the BCF in additional paid-in capital and record a corresponding discount on the debt liability

• No subsequent remeasurement of the amount recorded in equity

• Amortize any discount or premium in the same manner as nonconvertible debt (see FG 1.2.3)

• Account for derecognition as discussed in FG 6.7.5A

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Financing transactions