Search within this section

Select a section below and enter your search term, or to search all click Health Care Guide

Favorited Content

The core principle of this Topic is that an entity recognizes revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

A contract is an agreement between two or more parties that creates enforceable rights and obligations. Enforceability of the rights and obligations in a contract is a matter of law. Contracts can be written, oral, or implied by an entity’s customary business practices.

An entity shall account for a contract with a customer … only when all of the following criteria are met:

Excerpt from ASC 606-10-25-3

An entity shall apply the guidance in this Topic to the duration of the contract (that is, the contractual period) in which the parties to the contract have present enforceable rights and obligations.

FASB Staff Q&A Revenue

Excerpt from Question 8: How do customer termination rights and penalties affect the identification of a contract duration?

A good or service that is promised to a customer is distinct if both of the following criteria are met:

In assessing whether an entity’s promises to transfer goods or services to the customer are separately identifiable in accordance with paragraph 606-10-25-19(b), the objective is to determine whether the nature of the promise, within the context of the contract, is to transfer each of those goods or services individually or, instead, to transfer a combined item or items to which the promised goods or services are inputs. Factors that indicate that two or more promises to transfer goods or services to a customer are not separately identifiable include, but are not limited to, the following:

At contract inception, an entity shall assess the goods or services promised in a contract with a customer and shall identify as a performance obligation each promise to transfer to the customer either:

Excerpt from ASC 606-10-25-15

A series of distinct goods or services has the same pattern of transfer to the customer if both of the following criteria are met:

Excerpt from ASC 606-10-25-3

An entity shall apply the guidance in this Topic to the duration of the contract (that is, the contractual period) in which the parties to the contract have present enforceable rights and obligations.

FASB Staff Q&A Revenue

Excerpt from Question 8: How do customer termination rights and penalties affect the identification of a contract duration?

Excerpt from ASU 2014-09 Basis for Conclusions

BC391. A renewal option gives a customer the right to acquire additional goods or services of the same type as those supplied under an existing contract…. A renewal option could be viewed similarly to other options to provide additional goods or services. In other words, the renewal option could be a performance obligation in the contract if it provides the customer with a material right that it otherwise could not obtain without entering into that contract.

Excerpt from ASC 606-10-55-43

If a customer has the option to acquire an additional good or service at a price that would reflect the standalone selling price for that good or service, that option does not provide the customer with a material right.

Excerpt from ASC 606-10-55-42

If, in a contract, an entity grants a customer the option to acquire additional goods or services, that option gives rise to a performance obligation in the contract only if the option provides a material right to the customer that it would not receive without entering into that contract…. If the option provides a material right to the customer, the customer in effect pays the entity in advance for future goods or services, and the entity recognizes revenue when those future goods or services are transferred or when the option expires.

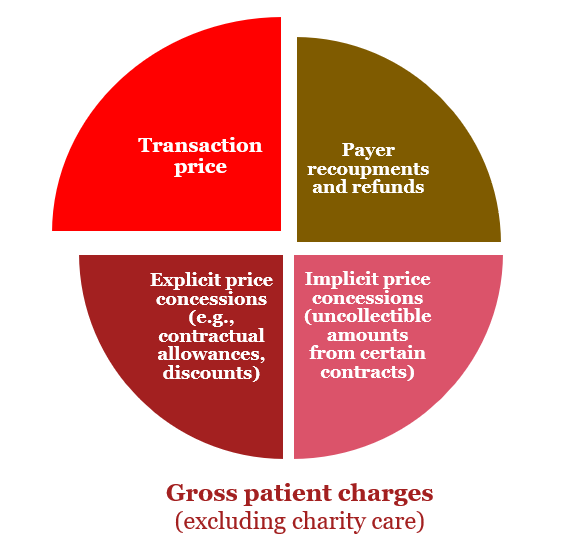

An entity shall consider the terms of the contract and its customary business practices to determine the transaction price. The transaction price is the amount of consideration to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer, excluding amounts collected on behalf of third parties (for example, some sales taxes). The consideration promised in a contract with a customer may include fixed amounts, variable amounts, or both.

An entity shall recognize revenue when (or as) the entity satisfies a performance obligation by transferring a promised good or service (that is, an asset) to a customer. An asset is transferred when (or as) the customer obtains control of that asset.

For each performance obligation identified…, an entity shall determine at contract inception whether it satisfies the performance obligation over time (in accordance with paragraphs 606-10-25-27 through 25-29) or satisfies the performance obligation at a point in time (in accordance with paragraph 606-10-25-30). If an entity does not satisfy a performance obligation over time, the performance obligation is satisfied at a point in time.

Excerpt from ASC 606-10-25-27

An entity transfers control of a good or service over time and, therefore, satisfies a performance obligation and recognizes revenue over time, if one of the following criteria is met:

For each performance obligation satisfied over time… an entity shall recognize revenue over time by measuring the progress toward complete satisfaction of that performance obligation. The objective when measuring progress is to depict an entity's performance in transferring control of goods or services promised to a customer (that is, satisfaction of an entity's performance obligation).

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Health Care Guide