In a typical acquisition of an asset in a transaction involving a monetary exchange, the book and tax bases of the asset are equal to the monetary purchase price (historical cost). Therefore, there is generally no temporary difference or related deferred tax to record at the acquisition date.

However, sometimes a group of assets may be purchased in a transaction that is not accounted for as a business combination under

ASC 805, usually because the group of assets does not meet the definition of a business. In those cases, a difference between the book and tax bases of the assets may arise.

ASC 740-10-25-51 prohibits any immediate income tax expense or benefit from the recognition of those deferred taxes, and, instead, requires the use of simultaneous equations to determine the assigned value of the asset and the related deferred tax asset or liability.

ASC 740-10-25-51 further provides that there may be instances when the simultaneous equation could, in theory, reduce the basis of an asset to less than zero. Under

ASC 740, this is not allowed and instead, a deferred credit is generated. The deferred credit is not a temporary difference under

ASC 740. The deferred credit is amortized to income tax expense in proportion to the utilization of the DTA arising from the realization of the tax benefits that gave rise to the deferred credit.

In the event that subsequent to the acquisition it becomes necessary to record a valuation allowance on the deferred tax asset,

ASC 740-10-45-22 requires that the effect of such adjustment be recognized in continuing operations as part of income tax expense.

ASC 740-10-45-22 further requires that a “proportionate share of any remaining unamortized deferred credit balance arising from the accounting shall be recognized as an offset to income tax expense. The deferred credit shall not be classified as part of deferred tax liabilities or as an offset to deferred tax assets.”

ASC 740-10-55-171 through

ASC 740-10-55-191 provides examples of the accounting for asset acquisitions that are not accounted for as business combinations in the following circumstance:

- The amount paid is less than the tax basis of the asset (Example 25 Case A)

- The amount paid is more than the tax basis of the asset (Example 25 Case B)

- The transaction results in a deferred credit (Example 25 Case C)

- A deferred credit is created by the acquisition of a financial asset (Example 25 Case D)

In addition to acquiring other assets, an entity may purchase future tax benefits from a third party other than a government acting in its capacity as a taxing authority, such as NOLs.

ASC 740-10-25-52 provides that the acquired tax benefits should be recorded with no immediate impact to income tax expense or benefit. This is illustrated in Example 25, Case F, in

ASC 740-10-55-199.

Conversely, according to

ASC 740-10-25-53, "[t]ransactions directly between a taxpayer and a government (in its capacity as a taxing authority) shall be recorded directly in income (in a manner similar to the way in which an entity accounts for changes in tax laws, rates, or other tax elections under this Subtopic)."

Asset acquisitions may result in the recognition of a DTA that is not expected to be realized (i.e., a full valuation allowance is required). Accounting for the recognition of the valuation allowance in these cases may not be straight forward. Example TX 10-27 illustrates accounting for deferred tax valuation allowances in a purchase of assets.

EXAMPLE TX 10-27

Accounting for deferred tax valuation allowances in a purchase of assets

Company A purchases two assets from an unrelated third party in a transaction considered to be an asset acquisition (not a business combination). Total consideration is $8 million in cash. The assets acquired consist of (1) a 20% equity interest in an entity that will be accounted for using the equity method and (2) a marketing-rights intangible allowing Company A to market the products and services of the investee entity in certain territories. The intangible asset has an estimated economic life of five years. The tax rate is 25%.

Under

ASC 805-50-30, the purchase price is allocated $6 million to the stock investment and $2 million to the intangible asset. For tax purposes, the $8 million purchase price is allocable in its entirety to the equity interest. The differences in purchase price allocation for book and tax creates two temporary differences: a deductible temporary difference of $2 million related to the equity method investment and a taxable temporary difference of $2 million related to the intangible asset.

Company A has determined that the ultimate manner of recovering its equity method investment is through disposal (i.e., dividends are not expected to be paid) and therefore the deductible temporary difference of $500,000 ($2,000,000 @25%) is expected to result in a capital loss. Company A has no other existing sources of capital gain income and, therefore, will need to recognize a valuation allowance against the DTA.

How should Company A account for the valuation allowance?

Analysis

The recognition of the valuation allowance would result in the immediate recognition of a deferred income tax expense, which appears to contradict the specific prohibition against immediate income statement recognition in

ASC 740-10-25-51.

We believe the prohibition in

ASC 740-10-25-51 extends to any valuation allowance related to deferred tax assets arising in the asset acquisition. As a result, the deferred tax asset of $500,000 would be recorded along with a valuation allowance, rather than using a simultaneous equation to calculate the deferred tax asset and a corresponding adjustment to the asset. As a result of recording the deferred tax asset and valuation allowance, there is no net impact on the provision.

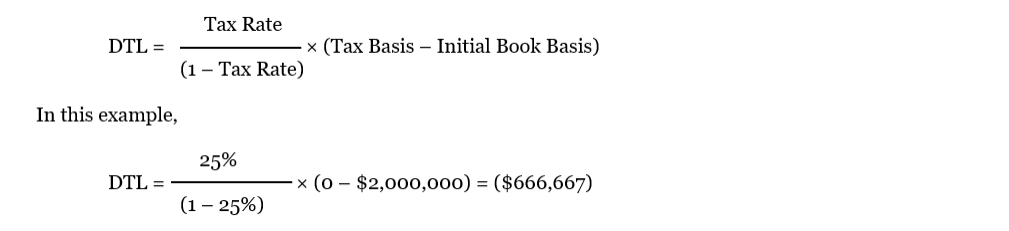

The remaining deferred tax effect is the recognition of the deferred tax liability related to the marketing intangible. The recognition of the deferred tax liability related to the marketing intangible would, in turn, increase the book basis of the asset. As such, the amount of the deferred tax liability and adjustment to the carrying amount of the asset is determined by using a simultaneous equation:

Thus, Company A would record the following journal entry:

Dr. Equity method investment |

$6,000,000 |

|

|

Dr. Intangible asset – marketing rights |

2,666,667 |

|

|

Dr. Deferred tax asset – equity method investment |

500,000 |

|

|

|

|

Cr. Deferred tax liability – marketing rights intangible |

|

666,667 |

|

|

Cr. Deferred tax asset – valuation allowance |

|

500,000 |

|

To record the asset acquisition and the related deferred taxes.

In-process research and development (IPR&D) acquired in an asset acquisition is expensed if it has no alternative future use. Such write-off occurs on the acquisition date prior to the measurement of deferred taxes. Accordingly, deferred taxes are not provided on the initial differences between the amounts assigned for financial reporting and tax purposes, and IPR&D is charged to expense on a gross basis.