Questions often arise regarding how single-member and multiple-member LLCs should account for income taxes in their separate financial statements.

ASC 272,

Limited Liability Entities, provides some guidance for accounting for LLCs.

ASC 272-10-05-4 indicates that LLCs are similar to partnerships in that members of an LLC are taxed on their respective shares of the LLC’s earnings (rather than the entity itself). Therefore, multiple-member LLCs generally do not reflect income taxes if they are taxed as partnerships (i.e., a partnership tax return is filed and the investors each receive a K-1) and are not otherwise subject to state or local income taxes. However, if a multiple-member LLC is subject to state or local income taxes (certain states impose income taxes on LLCs) the entity would be required to provide for such taxes in accordance with

ASC 740. This approach would apply irrespective of whether the members are part of the same consolidated group or not.

Single-member LLCs may be accounted for differently. The US federal tax law provides an election for single-member LLCs to be taxed as either associations (i.e., corporations) or “disregarded entities.” If the election is made to be taxed as an association, there is no difference between classification as a single-member LLC and a wholly owned C corporation for US federal income taxes. If a single-member LLC does not specifically “check the box” and elect to be taxed as an association, it is automatically treated as a disregarded entity. This means that for US federal income tax purposes, single-member LLCs are accounted for as divisions of the member and do not file separate tax returns.

ASC 740-10-30-27A provides an accounting policy election for allocating consolidated income tax provision to entities that are both not subject to tax and disregarded by the taxing authority (e.g., single-member LLCs that did not “check the box” to elect to be taxed as an association).

ASC 740-10-30-27A

An entity is not required to allocate the consolidated amount of current and deferred tax expense to legal entities that are not subject to tax. However, an entity may elect to allocate the consolidated amount of current and deferred tax expense to legal entities that are both not subject to tax and disregarded by the taxing authority (for example, disregarded entities such as single-member limited liability companies). The election is not required for all members of a group that files a consolidated tax return; that is, the election may be made for individual members of the group that files a consolidated tax return. An entity shall not make the election to allocate the consolidated amount of current and deferred tax expense for legal entities that are partnerships or are other pass-through entities that are not wholly owned.

The separate financials of a single-member LLC should disclose if it elects to record a tax provision. The accounting policy should be applied consistently from period to period. In addition, single-member LLCs that present a tax provision should also include disclosures consistent with those required by

ASC 740-10-50-17 (discussed in FSP

16.9.3).

Example TX 14-3 illustrates the assessment of whether a wholly-owned multi-member LLC is an in-substance single-member LLC.

EXAMPLE TX 14-3

Determining whether a wholly-owned, multi-member LLC is an in-substance single-member LLC

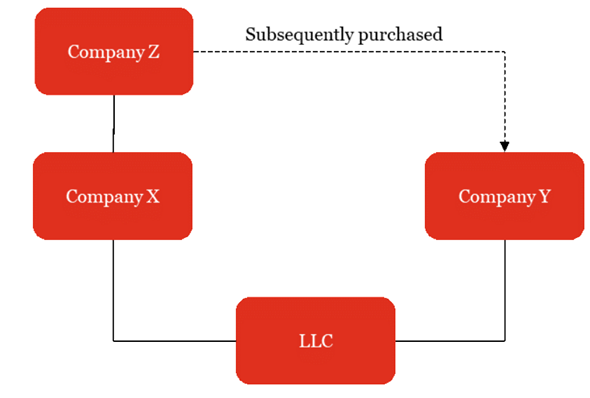

An LLC is 50% owned by two parties, Company X and Company Y (both C corporations). Company X is owned by another C corporation, Company Z. The LLC’s separate company financial statements appropriately do not provide for income taxes because it is a multi-member LLC and thus a flow-through entity for tax purposes. In a subsequent purchase transaction, Company Y was acquired by Company Z. After the acquisition of Company Y by Company Z, the LLC is ultimately wholly-owned by Company Z.

The following depicts the organizational structure.

After the purchase is completed, should the LLC reassess its determination as to whether to provide taxes in its separate company financial statements?

Analysis

No. We believe that the determination of whether taxes should be provided in the LLC’s separate financial statements should focus on whether the tax law considers the entity to be a flow-through entity. In this case, Company X and Company Y continue to retain their respective interests in the LLC. Therefore, the LLC is still considered a partnership for US federal income tax purposes, and the separate financial statements of the LLC should not include any provision for income taxes.