ASC 740-20-45-11(g) addresses the way an entity should account for the income tax effects of transactions among or with its shareholders. It provides that the tax effects of all changes in tax bases of assets and liabilities caused by transactions among or with shareholders should be included in equity. In addition, if a valuation allowance was initially required for deferred tax assets as a result of a transaction among or with shareholders, the effect of recording such a valuation allowance should also be recognized in equity. However, changes in the valuation allowance that occur in subsequent periods should be included in the income statement. Refer to

TX 12 for further discussion of intraperiod tax allocation.

For example,

ASC 740-20-45-11(g) would apply in the separate financial statements of an acquired entity that does not apply pushdown accounting to a transaction in which an investor entity acquires 100% of its stock (i.e., a nontaxable transaction). See

TX 10 and

BCG 10.1 for further discussion on pushdown accounting. If, for tax purposes, this transaction is accounted for as a purchase of assets (e.g., under IRC Section 338(h)(10)), there would be a change in the tax bases of the assets and liabilities. However, because the purchase accounting impacts are not pushed-down to the separate financial statements of the acquired entity for book purposes, there would be no change in the carrying value of the acquired entity’s assets and liabilities. In this situation, both the impacts of the change in tax basis and any changes in the valuation allowance that result from the transaction with shareholders would be recognized in equity. However, changes in the valuation allowance that occur in subsequent periods should be included in the income statement.

Example TX 14-4, Example TX 14-5, Example TX 14-6, Example TX 14-7, and Example TX 14-8 illustrate the accounting for the tax impacts of various transactions among or with shareholders on separate historical financial statements.

EXAMPLE TX 14-4

Interaction of pushdown accounting and deferred taxes on a subsidiary’s separate financial statements

Company A purchased Company B’s stock in a transaction accounted for as a taxable business combination (i.e., an asset purchase for tax purposes) as a result of an election under IRC Section 338(h)(10). The value of the assets acquired for book and tax are equal. Company B is required to issue separate company financial statements. Company B uses the separate return method to record taxes in its separate financial statements.

Company B has the choice of whether or not to apply pushdown accounting in accordance with

ASC 805-50-25-4. Regardless of whether or not pushdown accounting is applied, the tax basis in goodwill would be stepped up as a result of the asset purchase. Thus, Company B will enjoy the benefit of the amortization of the tax basis in goodwill.

Should Company B record deferred taxes related to goodwill (which is equal for book and tax purposes on a consolidated basis at the time of the business combination) in its separate financial statements if Company B (1) applies pushdown accounting, or (2) does not apply pushdown accounting?

Analysis

Scenario 1—Pushdown accounting

No. Deferred taxes related to goodwill would not be recognized at the date of acquisition. Company B would reflect book goodwill at the amount that is pushed down. In this example, the book pushdown amount would equal tax goodwill and, thus all goodwill would be classified as component 1 goodwill (as described in

ASC 805-740-25-8 through

ASC 805-740-25-9). Assuming no goodwill impairment is recognized for book purposes, goodwill would be amortized and deducted for tax purposes creating a book over tax difference on the component 1 goodwill over time, for which a deferred tax liability would be recorded.

Scenario 2—No pushdown accounting

Yes. Deferred taxes related to goodwill should be recognized at the date of acquisition. Company B would not record book goodwill in its separate financial statements. However, the tax basis created on the tax-deductible goodwill as a result of the election to treat the business combination as an asset purchase would be attributable to Company B and should be reflected in Company B’s separate financial statements.

ASC 740-20-45-11(g) indicates that the effects of “all changes in the tax bases of assets and liabilities caused by transactions among or with shareholders shall be included within equity.” Accordingly, Company B would report an increase to contributed capital by the amount of the DTA initially recorded relating to the excess of tax over book basis in goodwill. In subsequent periods, changes to the DTA resulting from amortization of the goodwill for tax purposes would be reported as a component of deferred tax expense in the income statement, which would offset the current tax benefit attributable to the amortization of goodwill, resulting in no impact on the effective tax rate.

EXAMPLE TX 14-5

Accounting for the income tax effect of a taxable distribution by a subsidiary to its parent on the subsidiary’s separate financial statements

Company A owns 100% of Company B. Company B makes a taxable distribution of appreciated property to Company A. In Company B’s separate financial statements, the distribution is recorded for GAAP purposes at book value and reflected as a distribution to Company A; as such, no gain is recognized for book purposes. However, Company B is taxed in its jurisdiction on the excess of the distributed property’s fair value over its tax basis.

How should the tax effect of this transaction be reflected in the separate financial statements of Company B?

Analysis

ASC 740-20-45-11(c) states that the tax effects of an increase or decrease in contributed capital should be charged or credited to shareholders’ equity. Accordingly, in the example above, Company B should reflect the tax effects of the transaction as a reduction of paid-in capital. The application of

ASC 740-20-45-11 should be made from the perspective of the reporting entity (Company B).

EXAMPLE TX 14-6

Accounting in separate company financial statements for the tax consequences of a transfer of shares that results in a gain for tax purposes

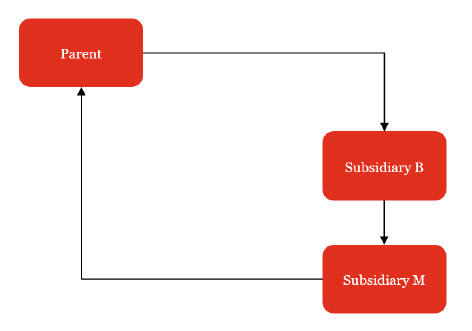

Parent owns 100% of the stock of Subsidiary B, which in turn owns 100% of Subsidiary M. Parent and subsidiaries B and M fall within the same tax jurisdiction (US). Subsidiary B prepares separate company financial statements using the separate return method. Parent files a US consolidated tax return that includes subsidiaries B and M.

Subsidiary B distributes the stock of Subsidiary M to Parent through a nonreciprocal transfer at book value. The book basis that Subsidiary B has in Subsidiary M’s stock exceeds the tax basis of its investment, but the book basis is less than the fair value of the shares. The transfer of Subsidiary M by Subsidiary B triggers an IRC Section 311(b) tax gain, which is deferred for tax return purposes because the transfer occurred within the consolidated tax group. On a consolidated basis, the gain will be recognized when Subsidiary B is no longer considered part of the consolidated group or upon the sale of Subsidiary M to a third party. A diagram of the organization and transfer follows:

Should Subsidiary B record the tax effects of this transaction in its separate company financial statements, even though the Section 311(b) gain is a deferred intercompany transaction on a consolidated tax basis?

Analysis

Yes. Under the separate return method, Subsidiary B must calculate the income tax effects of this transaction in accordance with

ASC 740-10-30-27 as if it were a stand-alone entity. The transfer of Subsidiary M to Parent should be characterized as a transfer that would trigger recognition of the 311(b) gain on a separate return basis. However, because the transaction involves a shareholder,

ASC 740-20-45-11 must also be considered.

The income tax consequence would be comprised of two components and would be accounted for as follows:

- Difference between Subsidiary B's book and tax basis in Subsidiary M (i.e., the outside basis difference)

In many cases, Subsidiary B would have historically asserted that Subsidiary M would be divested in a tax-free manner. This is because Subsidiary M is a domestic subsidiary, and therefore a deferred tax liability would not have been previously recorded for the outside basis difference when the tax law provides a means in which the investment can be recovered tax-free and the entity expects that it will ultimately use that means (ASC 740-30-25-7). Because Subsidiary M was divested in a manner that was not tax-free, Subsidiary B must record the tax effects of any previously unrecognized outside basis difference through the income statement, with a corresponding liability recorded in the balance sheet. The effect of this change should be recognized in the income statement in the period during which Subsidiary B is no longer expected to recover the outside basis difference in a tax-free manner.

If a deferred tax liability had been previously recorded for the difference between the book basis and the tax basis related to Subsidiary B’s investment in Subsidiary M, and if that deferred tax liability represented the actual tax consequence for the outside basis difference, no incremental tax consequence would need to be recognized in the income statement of Subsidiary B. Any differences between the deferred tax liability previously recorded on the outside basis difference and the actual tax rate applied to the outside basis difference would need to be recognized through the income statement in the period during which the expectation changed. - Difference between the fair value and book basis of the stock

To the extent that a tax liability is generated from Subsidiary B’s transfer of Subsidiary M’s shares to Parent, the portion of the tax liability related to the excess of fair value over book value should be accounted for as a direct charge to equity by analogy to ASC 740-20-45-11(g), which provides that “the tax effects of all changes in the tax bases of assets and liabilities caused by transactions among or with shareholders should be included in equity.” This portion of the tax liability is not related to a previously unrecognized outside basis difference, but rather is considered an incremental tax effect of an equity restructuring between the company (Subsidiary B) and its shareholder (Parent).

The cash settlement of this liability depends on the terms of the intercompany tax-sharing agreement. If Subsidiary B will not be responsible for the tax due either currently or at some future date, the extinguishment of that liability is considered a capital contribution by Parent to Subsidiary B and should be recorded as a credit to equity.

EXAMPLE TX 14-7

Alternatives for recording a valuation allowance in purchase accounting in separate company financial statements

Company A acquired 95% of Company B's outstanding shares in a transaction in which the tax bases of Company B's assets and liabilities are not affected (i.e., carryover basis). Company B elected to apply pushdown accounting. Subsequent to the acquisition, Company B will be included in Company A's consolidated US federal income tax return. However, because Company B will continue to issue separate financial statements, Company B will need to elect an accounting policy for the allocation of current and deferred income tax expense in accordance with

ASC 740-10-30-27. Company B elects the separate return method.

As part of acquisition accounting, Company A evaluated the need for a valuation allowance against the acquired US federal deferred tax assets related to Company B and has determined that, on a consolidated basis, the company will generate sufficient future taxable income to realize its DTAs and that no valuation allowance is necessary.

Company B has generated losses in the past and anticipates generating future losses. Accordingly, Company B has determined that, as a standalone taxpayer, it would require a full valuation allowance against its DTAs.

How should Company B account for the establishment of the valuation allowance against its DTAs in its separate financial statements?

Analysis

We believe that there are two acceptable alternatives that are consistent with a separate return method.

Alternative 1 – no adjustment to goodwill

Company B would record the valuation allowance as part of applying pushdown accounting (after considering, to the extent appropriate, any newly created deferred tax liabilities resulting from the acquisition), record the same amount of goodwill as the consolidated entity (with respect to the acquisition of Company B), and reflect the difference (essentially the effect of establishing the valuation allowance) in net equity. This methodology would result in an allocation of income taxes consistent with a separate return method and would also keep goodwill consistent between the entities. Supporters of this alternative believe that because pushdown accounting is generally considered a "top-down" concept, the purchase price allocation (including the resulting goodwill) should be the same for the subsidiary as it is for the consolidated entity.

Alternative 2 – adjustment to goodwill

Company B would record the valuation allowance as part of applying pushdown accounting with an offsetting increase in goodwill. This methodology would result in an allocation of income taxes consistent with a separate return method, but goodwill at Company B would be different than the goodwill related to Company B carried in the consolidated accounts. Proponents of this alternative believe that because the separate return method is intended to reflect the current and deferred tax consequences of the subsidiary’s activities as if it was a separate taxpayer, the tax effects arising from the pushdown of the new book bases of assets and liabilities (including the resulting implications on the determination of recorded goodwill) should reflect the implications to the entity as a separate taxpayer. Supporters of this view also note that goodwill impairment testing should be done on a separate company basis as described in

ASC 350-20-35-48, which, in some circumstances, could result in an impairment of goodwill at the subsidiary level, but not in consolidation or vice versa.

A similar question may arise when determining the appropriate tax rate for establishing deferred taxes in the separate financial statements of an acquired subsidiary. For example, when considering state deferred tax assets and liabilities in a separate company financial statement, there may be differences from the consolidated financial statement as a result of different state apportionment factors that would apply on a combined versus separate tax return basis. We believe the alternatives expressed above (adjustment to goodwill or no adjustment to goodwill) could also be applied to such a situation.

EXAMPLE TX 14-8

Deferred income tax effects of the acquisition of the noncontrolling interest in the consolidated and separate company financial statements of a pass-through entity

Company A consolidates a multi-member LLC in which Company A owns a 70% equity interest. The LLC holds public debt and is therefore required to file separate financial statements with the SEC. In prior periods, income taxes have not been reflected in the LLC's financial statements because the LLC was a partnership for US federal tax purposes. In the current year, Company A acquires the 30% noncontrolling interest (NCI) for fair value. As a result, the LLC ceases to be a partnership, becomes a single-member LLC, and effectively converts to a taxable division of Company A for US federal income tax purposes. The acquisition of the NCI is accounted for in equity with no change in the carrying amount of the assets and liabilities of the LLC.

For US federal income tax purposes, Company A is deemed to purchase the partnership assets proportionate to the acquired LLC interest (i.e., Company A is deemed to have acquired 30% of the partnership assets at fair value). Further, Company A is deemed to receive a distribution of partnership assets equal to its pre-existing equity interest (i.e., 70%). This creates a bifurcation of the partnership assets for tax purposes. The portion acquired through the purchase of the NCI is considered newly acquired, with tax basis equal to the price paid for the NCI. The assets deemed distributed would have carryover tax basis and lives.

a) How should Company A account for the additional tax basis in the consolidated financial statements?

b) How should the LLC account for the termination of its partnership tax status in the separate company financial statements?

Analysis

a) There can be direct and indirect tax effects stemming from transactions with noncontrolling shareholders (see

TX 10.9). All direct tax effects, net of valuation allowance, should be accounted for in equity in accordance with

ASC 740-20-45-11(c), which is applicable when total equity is increased or decreased. Any indirect tax effects, such as a change in indefinite reinvestment assertion or valuation allowance assessment, would be recorded in continuing operations in the current period. In this fact pattern, the benefit from the tax basis step-up was achieved through application of the relevant tax law resulting from a transaction recorded in equity. Therefore, it is a direct tax effect that should be recorded in equity.

b) The LLC was effectively converted from a pass-through entity to a single member LLC. Therefore, as discussed in

TX 14.5, we believe the LLC should present current and deferred income taxes in the separate company financial statements beginning in the period in which the tax status changed (

ASC 740-10-25-32). The company should follow its policy election for allocating consolidated income tax expense to single-member LLCs. The separate company financial statements should disclose the policy election and apply it consistently from period to period. If the reporting entity elects a policy to allocate tax to the LLC, all tax effects from the conversion, including the initial recognition of deferred taxes, would be recognized in continuing operations (i.e., income tax benefit or expense for the period) in accordance with

ASC 740-10-45-19.