In the event of a spin-off transaction, the parent (or spinnor) entity will need to evaluate whether the decision to spin-off the business into a separate entity results in a change to management’s ability and intent to indefinitely prevent the outside basis difference of a foreign subsidiary from reversing with a tax consequence. To the extent the decision to spin-off the business results in a change to the indefinite reinvestment assertion, the consolidated financial statements of the parent should reflect a charge to continuing operations at either the time of the decision to consummate the spin-off (i.e., prior to the spin), or at the time of the spin-off, even though such a charge would not have been required if the spin-off had not occurred.

If a charge is recognized in the consolidated financial statements prior to the spin-off, this charge should also be reflected in the standalone financial statements of the subsidiary if the outside basis difference relates to the subsidiary’s investment.

Example TX 14-10 discusses the alternatives related to the timing of recording the charge in the consolidated financial statements.

EXAMPLE TX 14-10

Accounting for a change in the indefinite reinvestment assertion as a result of a nontaxable spin-off transaction

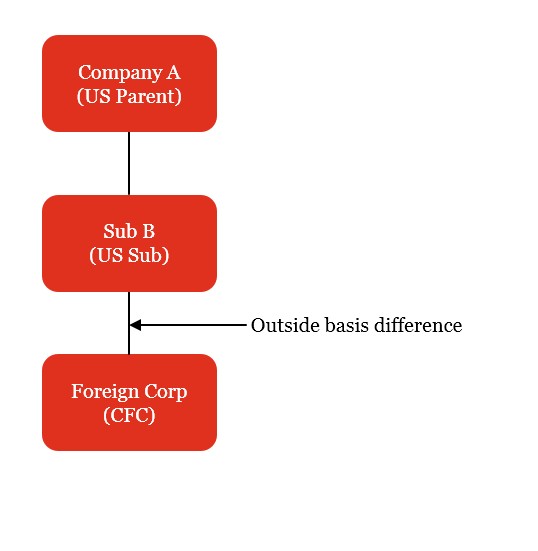

In 20X1, Company A decided to spin-off Subsidiary B and its controlled foreign corporation (CFC) in a nontaxable transaction. Company A’s management will prepare carve-out financial statements for Subsidiary B in connection with the anticipated transaction.

Historically, Company A asserted indefinite reinvestment under

ASC 740-30-25-17 regarding Subsidiary B’s outside basis difference in its investment in CFC (i.e., no deferred tax liability was recorded on the outside book-over-tax basis difference). After the spin-off, Subsidiary B will no longer be able to assert indefinite reinvestment. This is because after the spin-off, Subsidiary B will no longer receive funding from Company A and therefore will need to repatriate CFC’s cash in order to fund its US operations and repay separate company borrowings. Absent the spin-off transaction, Company A would expect to continue to assert indefinite reinvestment (i.e., no other factors exist that would cause Company A to change its indefinite reinvestment assertion).

At what point in time should the tax effect of a change in the indefinite reinvestment assertion (i.e., the recording of a DTL for the outside basis difference) as a result of the nontaxable spin-off be recorded?

Analysis

We believe that there are two acceptable accounting alternatives.

Alternative 1

Record the DTL on both the consolidated and separate financial statements when the decision to consummate the spin-off transaction is made (i.e., prior to the spin).

This view is supported by

ASC 740-30-25-19, which provides that “[i]f circumstances change and it becomes apparent that some or all of the undistributed earnings of a subsidiary will be remitted in the foreseeable future but income taxes have not been recognized by the parent company, it should accrue as an expense of the current period income taxes attributable to that remittance.” In addition, this view is consistent with

ASC 740-30-25-10, which indicates that a company should record a DTL for the outside basis difference when it is apparent that the temporary difference will reverse in the foreseeable future (i.e., no later than when the subsidiary qualifies to be reported as discontinued operations).

Proponents of this alternative point to the fact that the temporary difference related to Subsidiary B’s outside basis difference in its investment in the CFC existed prior to the change in assertion, but, by virtue of the indefinite reinvestment exception, Company A was not required to accrue income taxes on the undistributed earnings of the CFC. Consequently, the moment it becomes apparent that some or all of the undistributed earnings of the subsidiary will be remitted in the foreseeable future, Company A should record the DTL on the outside basis difference in its consolidated financial statements.

Alternative 2

Record the DTL on both the consolidated and separate financial statements at the time of the spin-off transaction.

Proponents of this alternative point to the fact that absent the spin-off transaction, Company A would continue to assert indefinite reinvestment under

ASC 740-30-25-17. Therefore, Company A’s expectations regarding the indefinite reversal of the temporary difference will not change until the consummation of the spin-off.

Refer to

TX 12.5.2.2 for discussion of intraperiod allocation of the related tax expense when recording the deferred tax liability.

Example TX 14-11 illustrates the recording of the tax effects of a taxable spin-off.

EXAMPLE TX 14-11

Measurement of the tax effects of a taxable spin-off of a majority-owned investment

Company A agrees to acquire Company B in a business combination. As a condition precedent to the purchase transaction stemming from its need for regulatory approval, Company A requires Company B to spin-off one of Company B's majority-owned subsidiaries ("Spinnee"). This transaction will be treated as a taxable transaction under the Internal Revenue Code. Prior to this transaction, Company B asserted that its outside basis difference in Spinnee (due to undistributed earnings) was indefinitely reinvested and therefore deferred taxes were not historically provided. At the date of the spin-off, Company B's investment in Spinnee was $500 and its tax basis was $400. As of the date of the spin-off, Spinnee's fair value was $800.

How should Company B account for the tax consequences of the taxable spin-off?

Analysis

The tax effects of this transaction can be separated into two distinct parts:

Part 1: The book/tax difference for which no deferred tax liability has previously been provided ($500 - $400 = $100)

Part 2: The additional taxable income resulting from the fair value of Spinnee over its current book basis ($800 - $500 = $300)

A tax liability should be provided on each, but the intraperiod allocation of the tax expense is different.

Consistent with the accounting for a change in assertion for Part 1, a deferred tax liability should be recognized for the outside basis difference of $100 multiplied by the applicable tax rate with a corresponding charge to tax expense in the income statement no later than the time of the spin-off.

ASC 740-20-45-11 states that "the tax effects of all changes in the tax bases of assets and liabilities caused by transactions among or with shareholders should be included within equity." Thus, for Part 2, the tax consequence of the $300 increase in the fair value of Spinnee would be a change in the tax basis caused by a transaction with shareholders (the spin-off). Therefore, upon spin-off, the tax expense arising from the increase in the value of Spinnee that will be borne by Company B should be charged to equity.